- India: Rupee slump curbs imported scrap buying activity

- Bangladesh: Downstream weakness keeps containerised scrap market slow

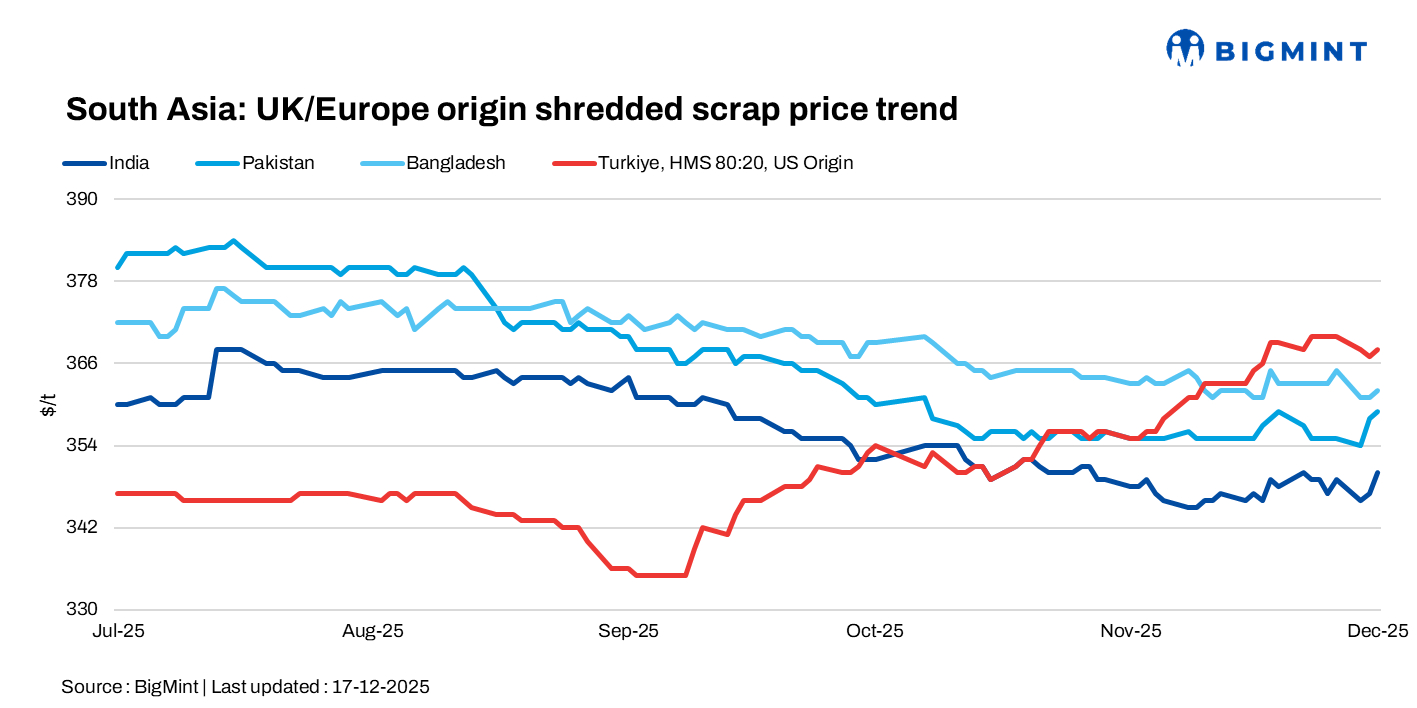

South Asian imported scrap markets remained subdued, with weak downstream demand and cautious buying across India, Bangladesh, and Pakistan on 17 December. Activity stayed limited, and market sentiment remained quiet, with only slight movement in offers amid year-end uncertainty.

India: Imported scrap demand in India remained subdued amid persistently weak buying interest, as the rupee slid to record lows near 91 against the US dollar, sharply inflating import costs. Market sentiment stayed quiet, with western suppliers largely absent and buyers avoiding fresh bookings.

EU-origin shredded scrap was last heard at $345-350/t CFR west coast India, while EU-origin HMS 80:20 stood at $315-318/t CFR. With no improvement in downstream demand, no major price movement is expected this week.

Pakistan: Imported scrap offers edged higher amid fewer cargoes available, prompting slightly improved buyer activity ahead of the holiday period, though overall interest remained limited due to high freight and LC costs. Recent Europe/UK shredded deals were heard at $354-359/t CFR Qasim, but trading stayed thin.

Bangladesh: Imported scrap market stayed subdued day on day, as weak downstream steel demand and cautious buyer sentiment continued to limit activity. Containerised scrap prices held largely steady, with HMS 80:20 at $335-336/t CFR, shredded at $360-366/t CFR, and PNS at $365-368/t CFR, while bulk US HMS was quoted at $355-360/t CFR, with limited interest above $365/t amid poor market confidence.

Turkiye: Deep-sea scrap prices remined stable on December 17, as market activity slowed and a stalemate emerged between buyers and sellers amid tightening margins. Mills continued to need cargoes for late January shipment but stayed hesitant due to weak downstream rebar demand and softer finished steel prices.

Offer levels remained firm, supported by high collection costs and slowing scrap inflows ahead of year-end, making lower prices difficult to sustain. Bids for US-origin HMS 80:20 were heard around $365/t CFR, against offers near $370/t CFR, limiting deal closures.

Leave a Reply