- Turkish imported scrap priced $20/t higher than Indian shipments in mid-Dec

- Indian imports generally command premium of $20-25/t over Turkish cargoes

- Aggressive restocking pushes up Turkish prices, South Asian prices remain weak

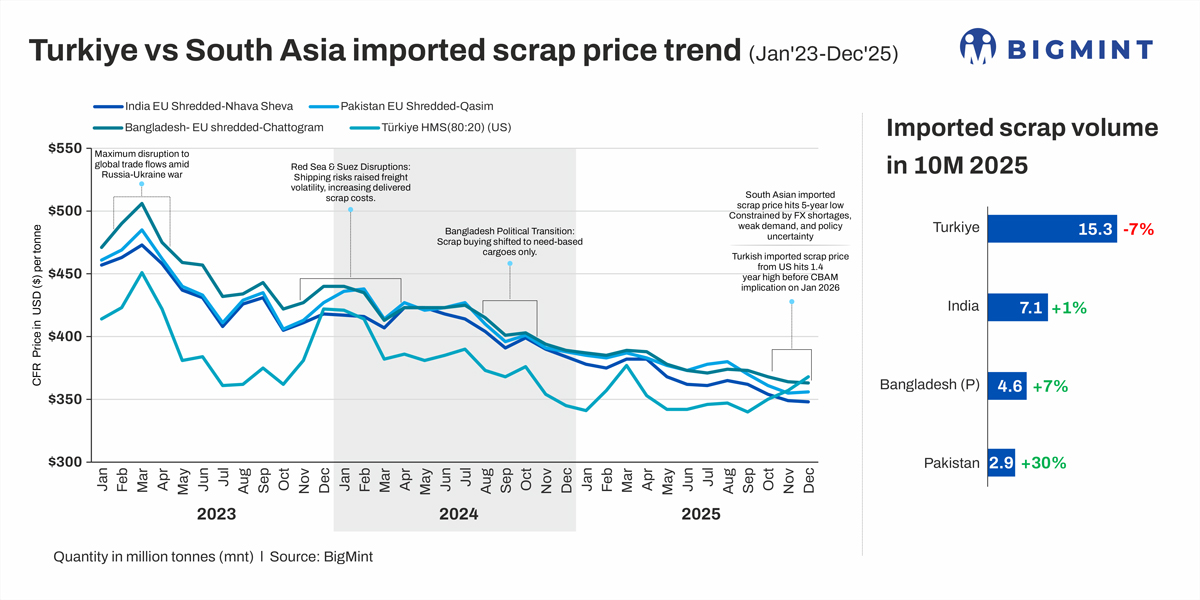

Morning Brief: In a notable shift from historical trends, Turkish imported scrap prices have surpassed South Asian prices since early November 2025, leading to a reversal of the price spread between the two.

Traditionally, containerised scrap imported into India and Pakistan commands a premium of $20-25/t over Turkish bulk prices, while the gap with Bangladeshi containerised scrap prices stands at $25-30/t.

Price spread analysis

On 16 December 2025, prices of US-origin HMS 80:20 (bulk) imported into Turkiye stood at $367/tonne (t) CFR Iskenderun, which was $20/t higher than India’s prices of European shredded (containerised) at $347/t CFR Nhava Sheva. The same price gap for Pakistan stood at $9/t, with European shredded (containerised) at $358/t CFR Qasim, while Bangladesh’s prices were lower by $6/t, with containerised UK-origin shredded at $361/t CFR Chattogram.

In terms of monthly averages, Turkish prices were higher by $8/t than Indian ones in November, with the spread widening to $20/t in the first half of December.

On 3 November, Indian and Turkish prices converged, with both at $351/t CFR. Turkish prices intersected with Pakistani levels from around 10 November, at the $356/t CFR mark. Meanwhile, Turkish prices began to surpass Bangladeshi ones from around 26 November, when both hovered near $362-363/t CFR.

Following this, Turkish prices have steadily increased, lifted by short burst of restocking, firmer rebar sales momentum, and pockets of speculative buying, while South Asian prices largely followed a downward trajectory, weighed down by weak demand, tight liquidity, and increased reliance on cheaper domestic scrap and sponge iron. However, in the first half of December, South Asian prices recovered slightly due to a slight improvement in demand.

BigMint’s data reveals that Turkish imported HMS 80:20 prices on 16 December were higher by 4.5% against 3 November, while Indian and Bangladeshi imported shredded fell by 1.1%. Imported shredded prices into Pakistan were marginally higher by 0.6%.

Similar trend last seen 2 years back

Notably, a similar reversal was last seen nearly two years ago, in December 2023-January 2024, when Turkish prices were higher by an average $4/t. At that time, the reversal was rooted in geopolitics.

Following the Red Sea crisis, which began on 19 October 2023, freights surged, insurers added security premiums, and vessel availability tightened. These disruptions pushed up logistics costs in South Asia more sharply than in Turkiye, creating a temporary premium for Turkish deep-sea scrap.

However, market participants believe that the present divergence is temporary and does not reflect a structural shift.

What factors pushed Turkiye’s scrap prices higher?

Short, intense restocking cycle driven by govt projects: The rise in Turkish scrap prices was triggered by mills entering late November with unusually low inventories. This created a brief but aggressive restocking push, tightening availability and lifting deep-sea offers. Rebar demand improved at the time because of the announcement of government-backed housing projects targeting 500,000 units by 2027. Traders added a speculative layer, supporting both scrap and rebar offers to stretch the momentum.

Winter scrap collection constraints tighten supply: Due to the onset of winter, European scrap supply tightened, and collection costs rose to EUR 255-260/t delivered to docks in the first week of December compared to EUR 245-250/t a month ago. Freight rates moved up, and a firmer euro (TRY 49.7/EUR 1 in December versus TRY 48.9/EUR 1 in November) inflated dollar-denominated offers. Sellers kept offers firm as Turkish mills filled January production slots, reinforcing the upward trend.

Demand from EU strengthens ahead of CBAM implementation: The 2026 CBAM framework, with stricter emission accounting, has increased the cost of higher-emission EU blast furnace output. This widened the competitiveness gap with Turkish EAF-based steel. Early signs of this shift are visible: mid-sized EU buyers have increased forward inquiries for Turkish longs and flats, indirectly pulling Turkish mills into a more active scrap-consumption cycle and supporting procurement through Q4.

South Asian prices move in opposite direction, hit 5-year low

During the same period, South Asian scrap prices remained under pressure due to weak downstream steel demand, persistent liquidity constraints, and tighter furnace operations across India, Pakistan, and Bangladesh.

India’s import appetite weakens as steel market sentiment remains soft: Indian buyers increasingly avoided new bookings and shifted to cheaper domestic scrap and sponge iron, leading to muted import activity. Landed costs of imports were higher by around INR 2,500-3,000/t in September-December.

Weak finished steel prices, with rebar hitting a five-year low in November 2025, also pushed mills to reduce bookings. Meanwhile, the rupee weakening past 90/USD also sharply lifted import costs, while a $10-15/t bid-offer gap hindered deal closures.India’s total scrap imports rose just 1% y-o-y to 7.1 million tonnes (mnt) in 10MCY’25.

Bangladesh struggles under political, financial stress: Bangladesh’s scrap market remained highly cautious, with buyers persistently pushing for discounts amid prolonged election-related uncertainty.

Purchasing was largely restricted to need-based bookings, while liquidity stayed tight due to delayed re-tendering of government projects and an extended foreign exchange squeeze. Mill utilisation has collapsed to 35-40%, sharply reducing steel demand and eroding producers’ ability to absorb overheads.

Consequently, prices of EU shredded in December 2025 fell to levels last seen in November 2020. Bangladesh’s scrap imports, however, rose by 7% y-o-y to 4.6 mnt in 10MCY’25, though it should be noted that last year, the July Revolution had led to limited mill operations.

Pakistani prices hit 5-year low in Nov’25: Imported scrap prices in Pakistan in November 2025 also slipped to levels last seen in November 2020. Mills continued to operate with limited raw material requirements, and payment constraints limited their ability to procure material even at lower levels. However, scrap imports rose sharply by 30% y-o-y to 2.9 mnt in 10MCY’25, likely driven by opportunistic purchases and relaxations on customs duties.

Outlook

The first quarter of 2026 is likely to open on a quieter, more measured footing for the global scrap market, with each major region carrying very different momentum into the new year. The current reversal in price spreads may not sustain, as Turkish prices are likely to soften modestly from December peaks. Deep-sea buying is expected to slow, with most January needs of Turkish mills secured. Competitive Chinese billet offers may also draw buyers, leading to lower demand for scrap. However, China’s export quota and licensing regulations and trade remedial measures instituted by over 80 countries to counter Chinese steel exports will shape scrap and steel dynamics in 2026.

That said, a sharp correction looks unlikely. The tighter 2026 CBAM framework keeps Turkish EAF steel cost-advantaged for European buyers, acting as a stabilising floor for scrap demand. Mills may only return to the market more actively by mid-February as they prepare for spring production cycles.

The real swing factor is likely to be Europe’s quota reshuffle for 2026. Turkish mills exhausted their 2025 quotas early, for the entirety of 402,733 t of hot-rolled coils (HRCs) and nearly all 94,993 t of rebar. Market sources expect cuts of up to 50% in the new quota period, which would push HRC quotas down toward 200,000 t and rebar toward 45,000-48,000 t.

With US access already lost due to tariffs, tighter EU quotas increase mills’ dependence on regional and domestic markets, making scrap procurement more sensitive to inventory cycles and sentiment swings.

South Asia is set to begin the new year on a weaker note. India’s import appetite is likely to remain subdued, as domestic scrap and sponge iron remain cheaper and a weak rupee continues to inflate import costs. Buyers will stay cautious unless global shredded prices correct further. However, supply shortages may push mills towards sourcing imports, which could support imported scrap prices.

Pakistan could see a brief firming in late January if current weak inflows create inventory tightness. However, Bangladesh may emerge as the most active buyer in the first quarter of 2026, supported by improving letter of credit (LC) conditions and gradually recovering confidence after months of political and financial uncertainty.

Leave a Reply