- Weak domestic demand exerts downward pressure on prices

- Mills maintain cautious output amid subdued consumption

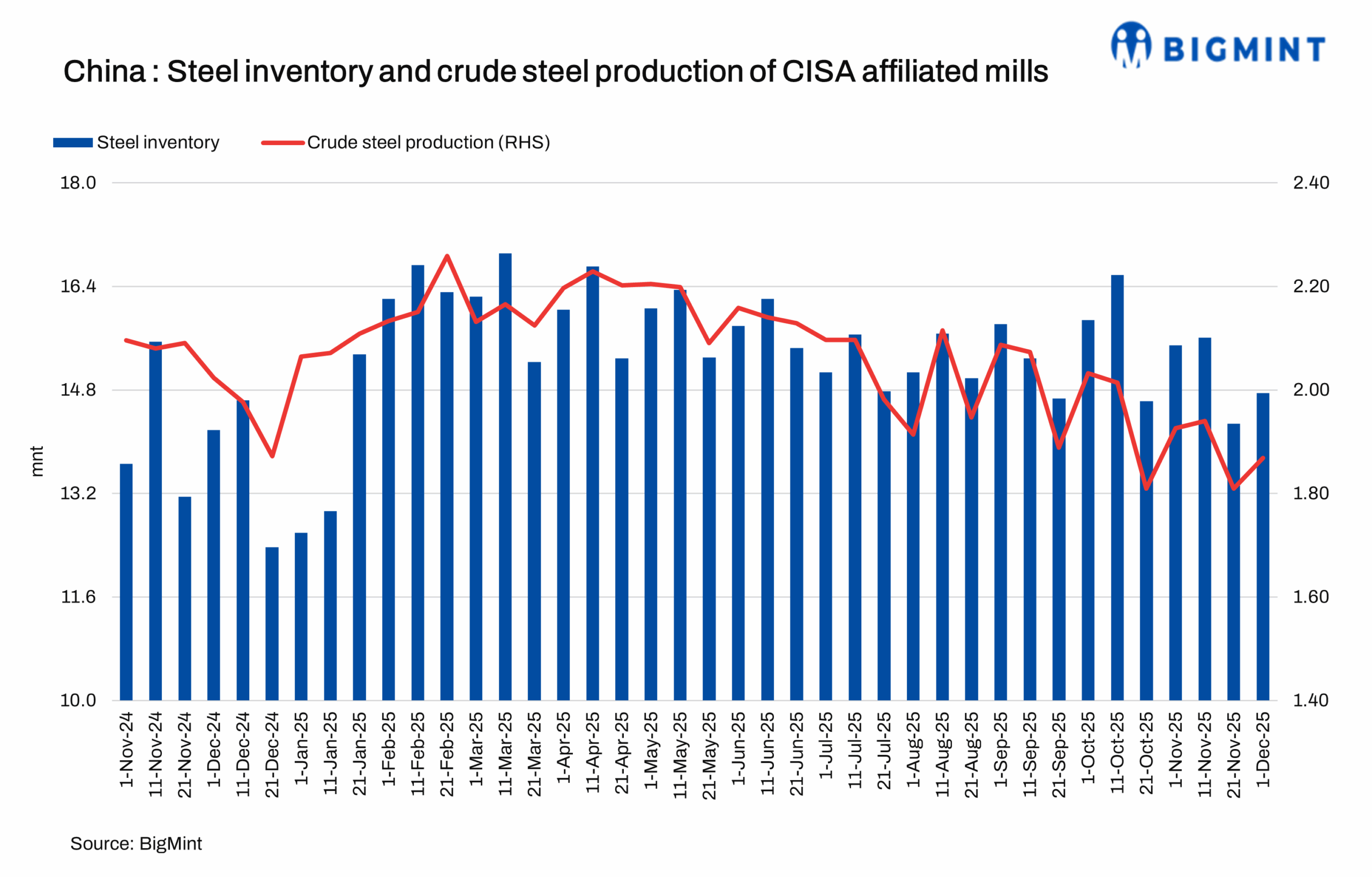

The China Iron and Steel Association (CISA) reported that total steel inventory at key Chinese enterprises reached 14.75 million tonnes (mnt) in early-December 2025 (1-10 Dec’25), up by 470,000 tonnes (t) or 3.3% from 14.28 mnt in late November. However, inventories were down by 740,000 t or 4.8% m-o-m from 15.49 mnt in early November. On a y-o-y basis, inventories rose by 570,000 t or 4% compared with 14.18 mnt in early-December 2024.

Production volume

The average daily crude steel output of CISA-affiliated enterprises stood at 1.869 million tonnes (mnt) in early December, up by 2.8% from 1.818 mnt in late November. However, on a y-o-y basis, output declined by 7.7% from 2.024 mnt in early December 2024.

Average daily finished steel output stood at 1.829 mnt in early December, down by 12.1% from 2.08 mnt in late November. This level was also 5.1% lower than that recorded in early December last year.

Average daily pig iron output stood at 1.714 mnt in early December, down by 3.4% from 1.774 mnt in late November, and 7% lower y-o-y.

Outlook

China’s steel market is likely to stay under pressure in the coming weeks, with prices lacking clear upward momentum amid persistently weak demand. Despite some monthly fluctuations, y-o-y declines in crude steel, finished steel, and pig iron output underscore sluggish consumption, while inventories, though lower on a sequential basis, remain higher than last year, tempering price support. Mills are therefore likely to maintain cautious production, suggesting steel prices will continue to fluctuate within a narrow range as market participants await clearer demand signals.

Leave a Reply