- Southeast Asia buyers wait for deeper price corrections

- Iran billet exports paused amid currency uncertainty

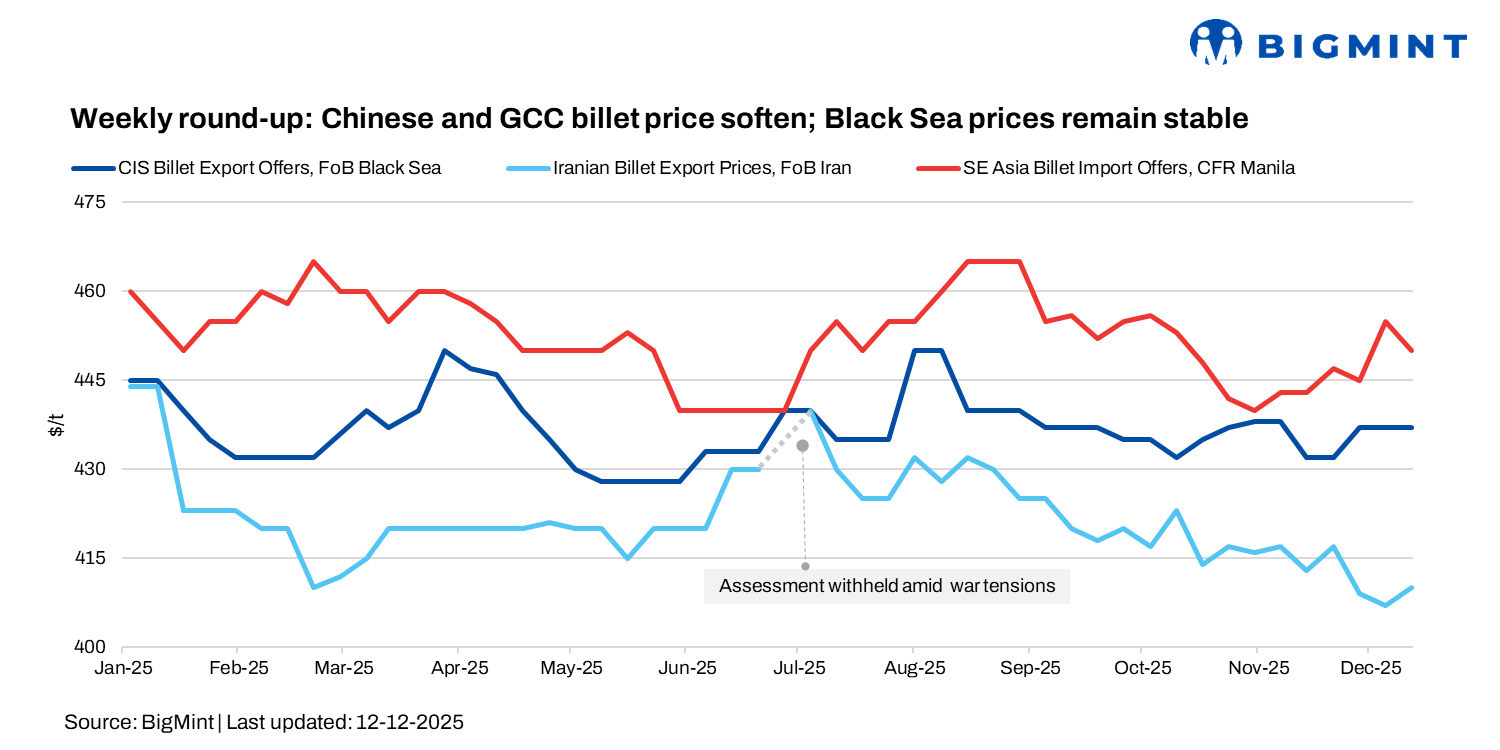

Global billet and scrap markets softened in the week ended 12 December as buying interest remained muted across Asia and the GCC. Chinese billet export offers eased w-o-w, pressured by weakening domestic sentiment and persistently slow demand from Southeast Asia, where buyers continued to hold back amid uncertain downstream conditions.

In contrast, imported deep-sea scrap prices into Turkiye held largely steady despite thin deal activity. US-origin HMS (80:20) inched up by $1/t to around $368-370/t CFR, touching an eight-month high last seen in April, while EU- and UK-origin scrap prices showed only marginal movement.

Black Sea billet market

CIS billet export prices stayed largely unchanged this week, though most levels were considered nominal amid thin buying interest. Russian square billet was quoted around $440-450/t FOB Black Sea, unchanged since early December. A few mills tested slightly higher levels near $452-455/t FOB, supported by a stronger rouble and firm scrap prices, but these offers attracted little response. Most cargoes were positioned for February shipment, with limited late-January availability.

In Turkiye, Russian billet was heard at $460-465/t CFR, while Donbas-origin material was offered at $450-460/t CFR. Market participants noted fewer Russian offers overall, as the strong rouble reduced export competitiveness, leaving Donbas suppliers more active. With no confirmed trades reported, the CIS export billet assessment remained unchanged at $435-437/t FOB.

Asian export billet market

Asian billet export prices softened through mid-December, weighed down by weakening sentiment in China and persistently slow buying interest across Southeast Asia. Chinese mills cut February-shipment offers for 3sp billet to $430-435/t FOB, down from $438-445/t FOB late last week, tracking a RMB 60/t fall in Tangshan billet prices amid weak seasonal demand.

Export activity from China remained subdued, with Southeast Asian buyers largely staying on the sidelines in anticipation of further corrections. Bid-offer gaps stayed wide. Buyers were generally willing to pay $440-445/t CFR for imported 3sp billet, while sellers held closer to $455/t CFR. Open-origin 5sp offers eased by $5-10/t w-o-w to $455-460/t CFR, though workable buying levels were heard at $445-450/t CFR.

In Indonesia, Dexin Steel trimmed base-grade billet offers to $435-438/t FOB for March shipment, down $2-3/t, but interest remained limited due to long lead times and relatively high prices. A rare deal was reported for 10,000–15,000 t of Chinese 3sp billet at $445-450/t CFR Thailand. However, overall demand in Thailand stayed weak as rebar sales slowed and buyers avoided holding inventory ahead of year-end.

In the Philippines, China-origin 3sp and 5sp billet offers softened to $450-455/t CFR. Re-rollers described the market as very slow, with poor long steel demand continuing to cap purchases. Overall, the Asian billet export market remains under pressure from soft Chinese fundamentals, cautious year-end buying, and weak downstream demand across Southeast Asia.

UAE billet market

The UAE billet market has entered a quieter phase as most re-rollers have already covered near-term requirements and both regional and overseas suppliers have largely met December sales targets. With little urgency on either side, trading volumes have thinned and are expected to remain muted in the coming weeks.

Chinese mills lowered offers to $455-458/t CFR, down $4-6/t w-o-w, reflecting efforts to secure cargoes in a competitive market. This continues to pressure GCC semis producers. Although Qatari and Omani integrated mills have sold out December allocations, achieved deal levels remain below expectations, with recent regional billet trades reported around $480-490/t CFR/CPT.

With buyers sufficiently stocked and suppliers reluctant to cut further, the market is likely to maintain a low-activity pattern until procurement cycles reopen.

Iranian billet export market

Iran’s billet export market slowed further as suppliers reassessed pricing strategies following recent changes to the currency exchange mechanism. Most mills refrained from issuing fresh offers, with nominal billet indications holding at $410-415/t FOB for December-January shipments. Traders remained cautious, noting that prices now need to stay closer to mill levels, while some buyers continued to push for significantly lower targets near $390-395/t FOB, keeping the market unbalanced.

Larger export volumes are expected to surface in the coming week. In the DRI segment, weak domestic demand and winter gas constraints are encouraging producers to seek export relief, with industry participants lobbying for easier export regulations to support outbound flows in the near term.

Leave a Reply