- Wide bid-offer gap stalls Indian pet coke trades

- Buyers shift to cheaper thermal coal amid high inventories

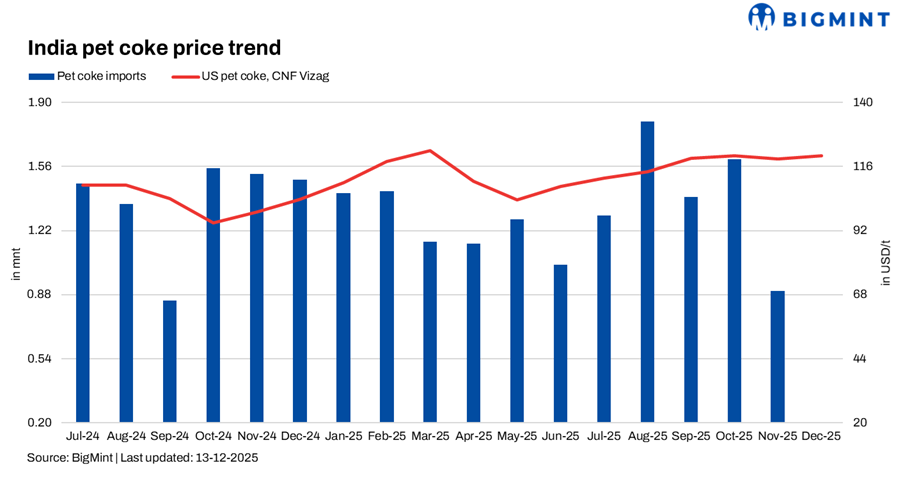

India’s petroleum coke (pet coke) market has reached a standstill in December 2025, with a persistent $4-8/t bid-offer gap preventing any meaningful trading activity. Sellers held firm at $118-121/t cost-and-freight (CFR) Kandla for US-origin 6.5% sulfur material, while buyers continued bidding $111-114/t, resulting in complete trade paralysis. This domestic stalemate unfolded against a backdrop of synchronized global weakness-declining US Gulf Coast (USGC) values, collapsing imports in Turkiye, and emerging geopolitical risks that now threaten Venezuelan export flows.

India: The core stalemate

Price dynamics & trading impasse

- Offer Range: $118-121/ton CFR Kandla (U.S. origin, 6.5% sulfur)

- Bid Range: $111-114/ton CFR Kandla

- Market Result: No recorded transactions in early December

Market sentiment: “No deals are happening at this high,” a major market participant observed-capturing the entrenched resistance across Indian buyers.

Headwinds crushing Indian demand

1. Thermal coal substitution accelerates

Indian buyers intensified the shift toward US Northern Appalachian (NAPP) thermal coal during December, supported by:

- Mozambique and South African coal available at a $5-10/ton advantage to pet coke

- Removal of additional Goods and Services Tax (GST) cess on thermal coal

- FOB Baltimore 6,900 kcal/kg NAR coal offered near $110/ton CFR India

2. Inventory overhang

- Cement plants remain well-stocked from October purchases

- Minimal urgency for new December spot buying

3. Economic unviability

- “U.S. and Saudi pet coke are not economical at these levels,” noted one industrial consumer

- Abundant domestic coal reinforced downward pressure on import demand

Outcome: A classic standoff-sellers hold firm, buyers wait for prices to crack.

United States: Export weakness emerges

- USGC 6.5% sulfur pet coke values slipped to $67-71.25/ton free-on-board (FOB)

- Seaborne exports down 13% week-over-week

- Chinese buying interest faded after a brief November peak

Turkiye: Import collapse

- October imports plunged 37% year-on-year

- Buyers swapped pet coke for Russian 6,000 kcal/kg NAR thermal coal, priced $15-18/ton cheaper

Cross-market convergence

Across India, Turkiye, and much of the Atlantic Basin:

- Alternatives became cheaper

- Buyers sat on comfortable inventories

- Sellers faced resistance across all grades

New geopolitical factor: The US seizure of a tanker off Venezuela-with more enforcement actions expected-has raised the risk of disruption to Venezuelan pet coke loadings. Higher vessel-insurance risk, reduced shipowner willingness to call Venezuelan ports, and potential slowdowns at upgrading complexes could cut export availability to India, Turkiye, and Mediterranean markets. This introduces a new geopolitical risk premium that may tighten mid-sulfur supply and partially offset the current global oversupply.

What to watch out for

1. Thermal coal prices

Particularly US NAPP, South African, and Mozambique coal.

2. Freight rate stability

USGC to India sits near $45.50/t-any spike could undermine coal economics.

3. Chinese market rebound

Any recovery in China may firm US pet coke values globally.

4. Venezuelan geopolitical escalation

If US. enforcement expands:

- Venezuelan-origin supply tightens

- Atlantic Basin balances shift

- Price floors strengthen for U.S. high-sulfur pet coke

India’s waiting game amid global downturn

India’s pet coke market sits in a holding pattern, mirroring global weakness but shaped by its own unique substitution pathways. The bid-offer standoff reflects a broader recalibration across the world’s pet coke markets, now complicated by a new geopolitical risk emanating from Venezuela.

As 2026 approaches, the key question becomes whether suppliers will soften pricing or whether India’s pivot toward cheaper thermal coal will solidify into a long-term structural shift. For now, the balance of power lies firmly with Indian buyers-armed with alternatives, abundant inventories, and little urgency.

Leave a Reply