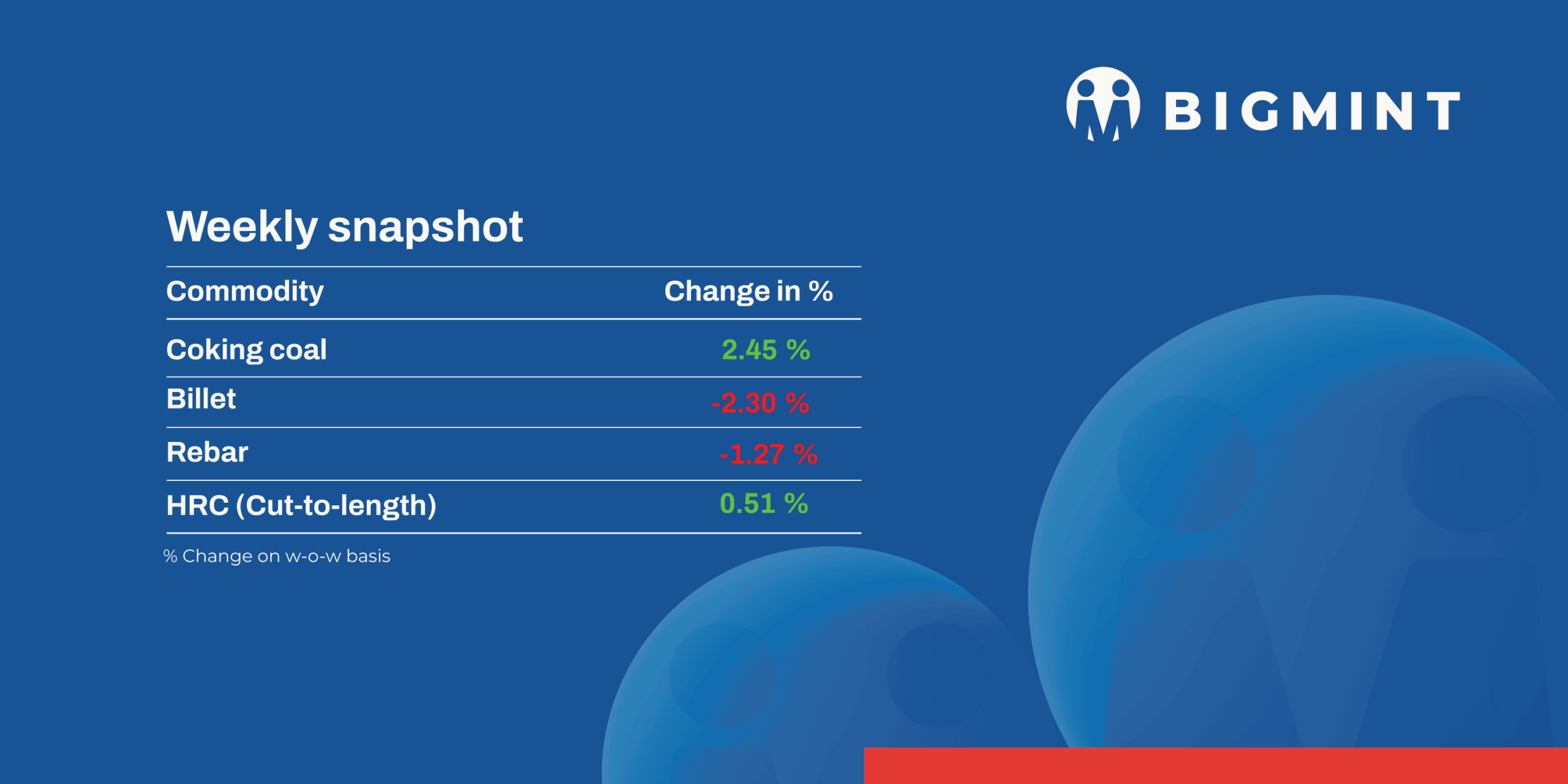

The domestic steel market weakened, with prices of semi-finished steel prices falling between INR 300-1,000/tonne (t) in the week ended 12 December.

Iron ore and pellet

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, fell by INR 200/t ($2/t) w-o-w to INR 9,450/t ($105/t) DAP on 12 December. Limited demand was recorded during the assessment period. Around 44,000 t of pellets (Fe 62.5-63%) were sold by local suppliers at INR 9,300-9,600/t exw Raipur at the revised offers. Raipur-based pellet producers reduced their offers for 62.5/63% (+/-0.5%) material by INR 300/t ($3.5/t) to INR 9,300-9,600/t ($103-106/t) exw recently.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices decreased by $2.5/tonne (t) w-o-w to $65.5/t FOB east coast on 11 December. BigMint heard approximately 575,000 t of export deals during this publishing period, were primarily concluded over the last weekend. The discount is now floating in the market at around 18-20% for the Fe 57% fines cargo, while exporters are still targeting 17-18%, which is not attracting buyers for fresh deals.

- NMDC Karnataka’s auctions on 9-10 Dec’25 recorded bookings of 112,000 t of iron ore. Lumps fetched premiums of up to INR 380/t From Kumaraswamy, 32,000-t lumps (10-40 mm, Fe 59.67%) booked at INR 4,085/t against base price of INR 3,705/t; 80,000-t fines (Fe 57.62-58.56%) booked at INR 2,984-2,755/t. However, from Donimalai, 48,000-t lumps (10-40 mm, Fe 55%) went unsold; base price was INR 2,850/t.

Coal

- South African RB2 (5,500 NAR) firmed w-o-w, with ex-Paradip and ex-Gangavaram rising to INR 8,900/t, while ex-Vizag increased to INR 8,850/t, up INR 100-200. RB3 (4,800 NAR) also strengthened, with ex-Paradip and ex-Gangavaram touching INR 7,500/t, and ex-Vizag at INR 7,400/t, also up INR 100-200. Despite higher offers, Indian acceptance remained negligible as sponge iron and rebar demand softened. Tightness deepened after crane damage halted operations at RBCT, delaying cargo availability owing to increased in demand from different destination until mid-February. Traders reported higher offers due to limited cargo availability and further currency depreciation. However, India mills demand for South African coal yet to pick up on slow domestic market.

- Domestic coal prices declined INR 150–250/t w-o-w, with 5,000 GCV falling to INR 5,800/t and 4,500 GCV to INR 4,900/t Exw-Bilaspur. The market remained under pressure following SECL’s 12 December auction, which offered 3.2 mnt of non-coking coal and saw full clearance. However, final bid prices were lower than previous levels, reinforcing bearish sentiment. Market participants expected further near-term softening as the impact of higher auction volumes continued to weigh on prices.

- India’s metallurgical coke market remained stable across regions during the week ended 10 December, as balanced supply met gradual demand. In eastern India, BF-grade (25–90 mm) met coke was assessed at INR 32,000/t ex-Jajpur, unchanged w-o-w, while western prices held at INR 30,200/t ex-Gandhidham. Foundry-grade material stayed firm at INR 36,000/t ex-Rajkot.

- BigMint’s premium hard coking coal (PHCC) index edged up on 12 December, reflecting firmer global cues, though bid–offer gaps persisted. The index was assessed at $227/t CNF Paradip, up $3/t from 6 December. Indian mills showed limited interest for Jan’26 cargoes, with only a few enquiries reported. Australian prime cargoes were quoted higher at $230–235/t CFR India, supported by weather-related disruptions and firmer China-linked trades. However, most Indian buyers stayed cautious, placing bids $5–10/t below offers, near $225/t CFR.

Ferrous scrap

- India’s imported scrap market stayed weak, with buying cautious and limited to selective bookings. Early winter restocking inquiries had little impact, as high inventories and weak finished steel demand restrained activity. Mills showed low interest across HMS, shredded, busheling, and PNS, with UK and Europe-origin shredded at $347-349/t CFR and HMS 80:20 near $317-319/t, keeping trade thin.

- Domestic scrap remained more attractive than imports, limiting overseas purchases. The rupee’s sharp fall to near-record lows against the US dollar raised import costs, forcing buyers to hold back unless urgently needed. As a result, sentiment stayed defensive by week’s end, with no immediate trigger for a near-term recovery.

- Approximately 3,000 t of imported scrap arrived in India, including around 1,500-2,000 t of HMS 80:20 from Africa at roughly $326/t CFR Mundra and about 1,000 t of tin-can bales from the UK and Australia at an average of around $263/t CFR Chennai.

Ferro alloys

- Indian silico manganese (60-14) prices edged up by around INR 100/t ($1/t) w-o-w to INR 69,300–69,900/t ($765–772/t) across Durgapur, Raipur, and Vizag. However, market activity remained subdued as mills cut production ahead of year-end maintenance shutdowns, leading to lower raw material offtake.Ferro Manganese:Indian ferro manganese (HC 70%) prices remained flat w-o-w at INR 72,000/t ($795/t) in both Durgapur and Raipur, as muted demand, cautious buying, and resistance to higher offers from consumers prevented sellers from pushing prices higher despite stable production levels.

- Ferro Silicon:Indian ferro silicon (Si 70%) prices declined by INR 1,400/t ($15/t) w-o-w to INR 97,600/t ($1,078/t) exw-Guwahati. Bhutan’s prices also fell slightly by INR 400/t ($4/t) to INR 98,600/t ($1,089/t).The market stabilised following Bhutan’s December price announcement, while prices eased as a few bulk orders were concluded at lower levels.

- Ferro Chrome:Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices dropped by INR 900/t ($10/t) to INR 109,100/t ($1,205/t) exw-Jajpur. The market remained quiet, as sellers held firm offers and buyers stayed cautious amid ample supply.

- Additionally, around 2,000 t were booked at Vedanta-FACOR’s ferro chrome auction on 10 December. The larger lot (Cr 57% min, 10–150 mm) achieved an H1 price of INR 107,500/t exw, in line with the base price, while the smaller lot settled at INR 108,800/t, up INR 800/t from the base price.

Semi Finished

- India’s semi-finished steel market witnessed a significant decline this week, as per BigMint’s assessment. Domestic billet prices across major markets dropped by INR 300-1,000/t ($3-11/t) w-o-w, due to weak buying interest and lower outstation enquiries. Key regions like Mandi Gobindgarh, Raigarh, Rourkela, and Raipur reported steeper corrections of INR 850-1,000/t ($9-11/t) w-o-w amid subdued market participation.

- The sponge iron market also saw a significant downturn, with prices across major producing regions plunging by INR 300-1,300/t ($3-14/t) w-o-w. Limited procurement, coupled with weakening finished steel demand, intensified downward pressure on spot prices, prompting a broad market correction.

- NMDC-Nagarnar Steel Plant conducted an auction on 9 Dec for 7,000 t of steel-grade pig iron, in which the entire quantity was booked at an average price of INR 31,200/t exw. This marks increased of INR 100/t compared to the previous auction on 28 Nov, in which the entire quantity of 5,000 t was sold at INR 31,100/t exw.

- Indian DRI (Direct Reduced Iron) offers declined by $2-6/t, assessed at $300/t CPT Raxaul for Nepal and $313/t CPT Benapole for Bangladesh. Despite this correction, export demand from both destinations remained weak.

Finished Long Steel

- IF-rebar:India’s Induction Furnace (IF) route rebar prices decreased w-o-w basis. Buying activity was limited, and fresh order bookings were lacking as buyers preferred need-based procurement and adopted a wait-and-watch approach. Manufacturers preferred either to lower their offers or to increase trade discounts, depending on their historical booking orders. Mill inventories are currently assessed at around 8–12 days across regions. As per current scenario, prices are likely to remain range-bound in the near term.

- On a weekly basis, prices in rebar steel witnessed decreased in the range of INR 100-1,000/t across the regions except in Mumbai market where price increased by INR 500/t as per BigMint assessment shows.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 38,800-39,200/t exw Raipur, INR 43,200-43,800/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 40,800-41,200/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 38,900-40,300/t ex Raipur.

- BF-rebar:In the BF rebar segment, prices have increased as mills raised their offers despite weak market demand. Buyers are reluctant to accept the higher levels resulting in slow trade activity. Trade-level BF rebar prices increased by INR 500/t ($6/t) w-o-w to INR 47,500/t ($525/t) exy-Mumbai, as per BigMint’s assessment on 12 December 2025. Prices are exclusive of GST at 18%.

In the projects segment, prices opened at INR 45,500-46,500/t ($506-517/t) FOR Mumbai.

Flat Steel

- Leading Indian steelmakers have rolled over hot-rolled coil (HRC) and cold-rolled coil (CRC) prices for December 2025 sales compared with late-November list levels.

- List prices of HRC (2.5-8 mm, IS2062, Gr E250 Br) ranged within INR 46,950-48,500/t ($522-539/t) ex-Mumbai. CRCs (0.9 mm, IS513 CR1) were at INR 53,200-55,750/t ($591-620/t).

- Trade-level prices of hot-rolled coils (HRCs) in India remained steady this week ended on 9 December 2025, reflecting consistent market conditions. HRC prices ranged between INR 45,500 and 47,600/t ($506-530/t) across regions, while cold-rolled coil (CRC) prices moved within INR 50,500 to 55,300/t ($562-616/t).

- The domestic HRC market continues with moderated activity, formed by steady demand and procurement aligned with current requirements, according to sources.

- India’s bulk imports of HRCs reached 64,035 t as of 5 December 2025. An additional 112,038 t of shipments are expected by mid-December.

- Bulk exports of HRCs from India totaled 134,507 t as of 5 December 2025.

- BigMint’s Indian hot-rolled coil (HRC, S275) export index for the European Union (EU) remained unchanged w-o-w at $520/t FOB main port, with mills refraining from issuing new offers after fully exhausting their October-December export quota. Uncertainty around the EU’s Carbon Border Adjustment Mechanism (CBAM) continues to weigh on HRC exports, with many mills holding back lower-margin offers and still waiting for official guidelines to be released.

- However, the Indian HRC (SAE 1006) export index for the Middle East slipped by $5/t w-o-w to $470/t, as trading activity remained subdued amid weak demand driven by the slowdown in construction activity and global oversupply.

Leave a Reply