- Domestic copper prices surge to three-year highs

- High-grade scrap buying slows on elevated offers

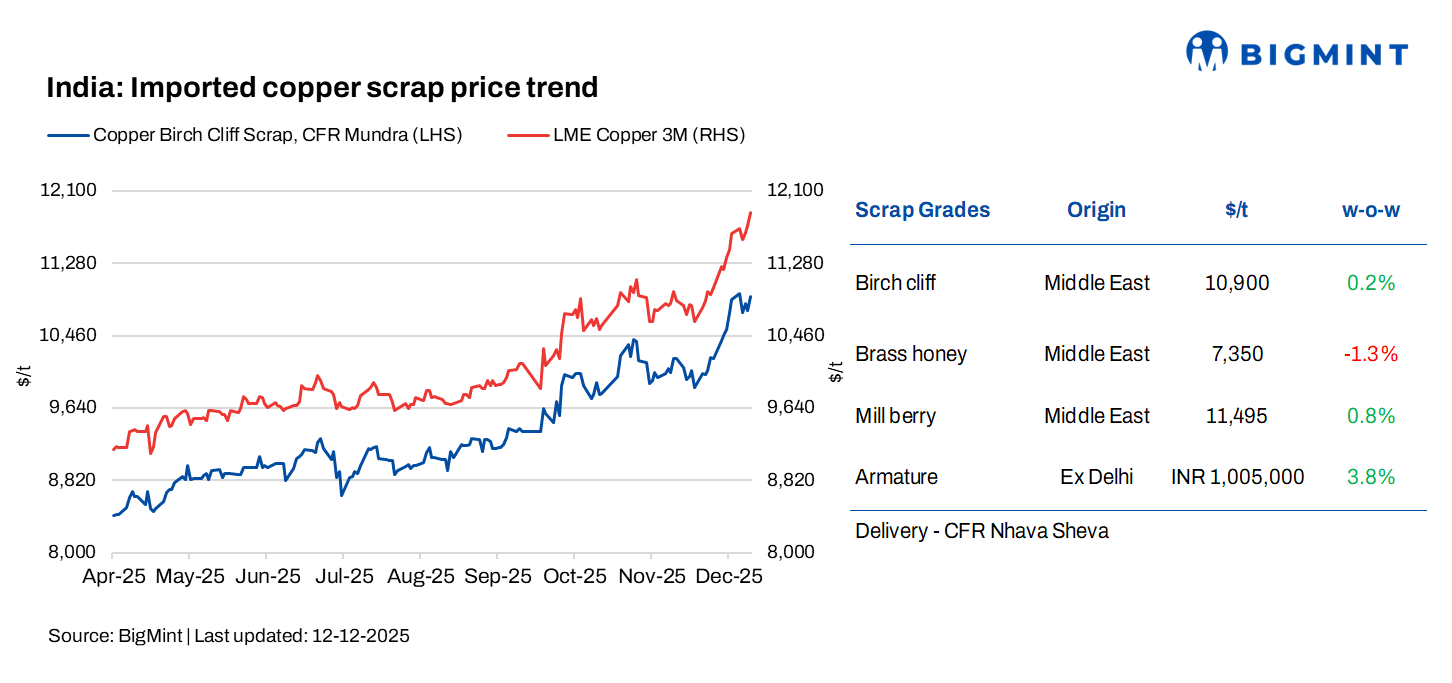

Imported copper scrap prices in India edged higher w-o-w on 12 December, supported by positive momentum in LME futures. Overall market momentum was capped by the seasonal slowdown in global scrap flows. Domestic sentiment also remained soft as buyers refrained from absorbing the recent LME highs, keeping restocking cautious despite stabilising demand indicators.

According to BigMint’s assessment, Birch/Cliff was assessed at $10,900/t, up 0.23% w-o-w, while US motors mix stood at $1,355/t (both CFR Mundra), up 7.11% w-o-w.

LME copper prices strengthen

LME copper prices climbed to $11,710/t on 11 December, up 2.61% from $11,411/t on 4 December, indicating sustained bullish momentum in the copper market as broader base metals sentiment remains firm. Copper inventories in LME-registered warehouses also increased to 165,850 t, rising 1.86% from 162,825 t a week earlier, signalling a moderate build in visible stocks even as prices strengthened.

Copper’s rally is being fuelled by tightening refined supply, stronger fund inflows, and a supportive macro backdrop. Prices have touched fresh highs across major exchanges as physical premiums jump, and smelters struggle with limited concentrate availability. Ongoing mine disruptions reduced upstream supply, and uneconomic smelting margins — especially in China — continue to restrict output and keep the market firmly undersupplied.

On the macro front, a softer US dollar and signs of stabilising global manufacturing have added to the bullish tone. LME on-warrant inventories saw a slight uptick, but stocks remain structurally low and insufficient to ease concerns over refined availability. With demand in key consuming regions still outpacing incoming material, the physical market remains tight, sustaining backwardation and supporting strong near-term pricing.

Market insight

Imported copper scrap trading activity remains extremely subdued as exporters across Australia, the US, and Europe report minimal inquiries, with most buyers shut for the year-end holidays. Indian buyers, too, are only lifting limited quantities, prompting many sellers to divert cargoes to Thailand, China, and South Korea, where price realisations are comparatively better. With global holidays reducing physical demand, both the aluminium and copper scrap markets are largely quiet, and meaningful trading is expected to resume only after mid-January.

Seasonal closures have further slowed copper scrap movement, with yards operating at reduced capacity and exporters avoiding fresh commitments until holiday schedules ease. Limited staffing, logistical constraints, and weak inquiry levels have sharply curtailed activity, and exporters anticipate normal flows restarting only in the second week of January once operations stabilise.

Price levels (CIF China)

Brass Honey (EU, 6-7% impurity): 58% of LME

Birch/Cliff (EU): 92% of LME

Birch/Cliff (UAE): 92% of LME

Imported copper scrap offers remained steady across major origins, with LME cash levels continuing to anchor price benchmarks. Australian-origin material saw Brass Honey (2% attachment) offered at 62% of LME, Birch/Cliff at 94% of LME (CIF China), Candy/Berry at 97% of LME, while Millberry continued to trade flat to LME.

UAE-origin indications reflected Brass Honey (4% attachment) at 62% of LME, Millberry at 99% of LME, and high-grade Druid quoted around 91% of LME on an indicative basis.

In the Indian market, the recent rise in LME prices has not been fully absorbed, keeping copper scrap demand muted. Importers are resisting higher offer levels from overseas suppliers, widening the bid-offer gap. High-grade categories such as Birch/Cliff and Millberry continue to see slow offtake despite tight availability. Market participants expect clearer pricing and improved buying interest only after LME stabilises and domestic demand strengthens in early January.

BigMint’s latest assessment indicates that copper prices across key categories in India have climbed to their highest levels in nearly three years. Copper Armature Scrap (Ex-Delhi) increased from INR 968,000 on 5 December to INR 1,005,000 on 12 December, a w-o-w rise of around 3.8%. Copper Secondary CC Wire Rods (Ex-Delhi) strengthened from INR 1,030,000 to INR 1,070,000, up roughly 3.9% w-o-w, while Copper Primary CC Wire Rods (Ex-Delhi) moved higher from INR 1,090,000 to INR 1,130,000, marking a gain of about 3.7% w-o-w. These consistent increases underscore strong domestic pricing momentum and reflect supportive market conditions heading into mid-December.

Outlook

Copper scrap activity is likely to stay quiet until mid-January as global holidays limit supply and dampen buying. While LME strength and tight refined availability support a bullish tone, domestic demand in India should recover only once prices stabilise and restocking resumes. A clearer pickup is expected early next month as market flows normalise.

Leave a Reply