- Billet market softness limits scrap price support

- Trading remains quiet despite firmer assessed levels

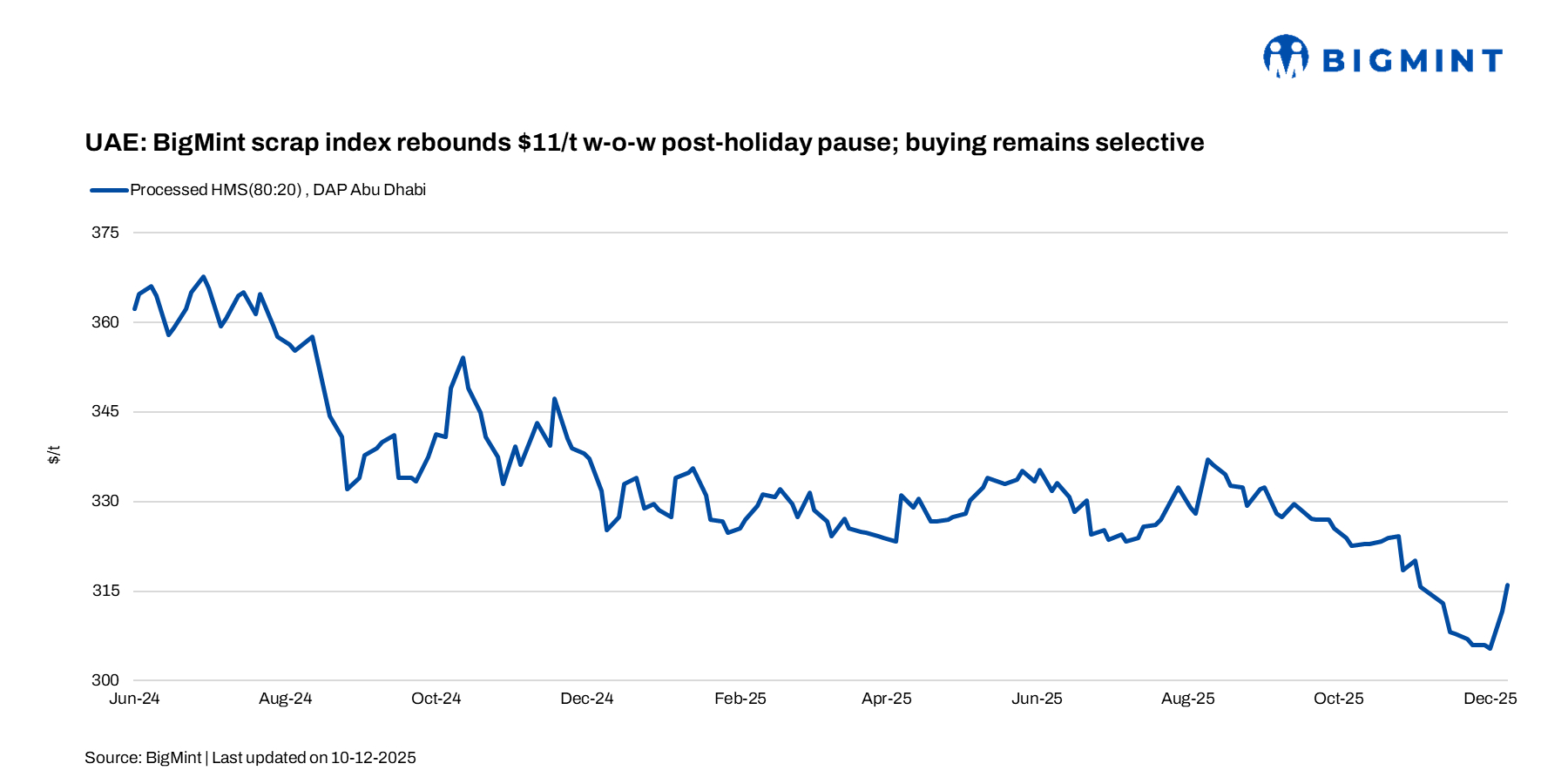

The UAE’s domestic scrap index posted a sharper rebound of AED 39/t ($11/t) from 3 December to the week ended 12 December, with processed heavy melting scrap (HMS) climbing to AED 1,161/t ($316/t) as of 10 December. Despite the price uptick, trading activity remained relatively quiet.

Market participants report processed HMS trading at about AED 1,160/t ($316/t), unprocessed HMS and PNS in the AED 1,120-1,150/t range ($305-313/t), and shredded scrap at AED 1,190-1,200/t ($324-327/t). Prices have stabilised after the holidays with an uptick, but overall demand is steady rather than strong. Some of the smaller local mills’ bids for unprocessed HMS were assessed lower at AED 1,075-1,100/t ($293-300/t).

A major trading house representative noted that local mills have not announced any fresh prices this month, leaving the market to follow previous levels in the current week: AED 1,160-1,170/t ($316-319/t) for processed HMS, AED 1,120-1,130/t ($305-308/t) for HMS, and AED 1,180-1,190/t ($321-324/t) for shredded scrap. He added that sentiment is steady, but mills appear in no rush to revise offers, keeping overall activity moderate.

UAE steel market

The UAE billet market has shifted into a quiet phase as most re-rollers have already covered near-term requirements and both regional and overseas suppliers have largely met their December sales targets. With little urgency on either side, trading volumes have thinned and are expected to stay muted in the coming weeks.

Chinese mills lowered offers to $455-458/t CFR, down $4-6/t w-o-w, reflecting their need to secure cargoes in a competitive market. This continues to pressure GCC semis producers. Although Qatari and Omani integrated mills have sold out December allocations, deal levels remain below expectations, with recent regional billet trades reported at $480-490/t CFR/CPT.

Given that buyers are sufficiently stocked and suppliers are reluctant to cut further, the market is likely to maintain a low-activity pattern until procurement cycles reopen. A meaningful rebound in prices will require either tighter Asian supply or a stronger pickup in regional rebar demand, neither of which appears likely in the immediate term.

Outlook

The UAE scrap market is expected to remain muted over the course of December. The recent firm rebound can hold only if buying interest improves; otherwise, a price correction looks likely as mills prepare to announce their next procurement levels. Without stronger demand from re-rollers, the market risks slipping back into a lower price band once fresh mill indications emerge.

Leave a Reply