- Exports dipped with broad declines across key suppliers

- Pacific freight firmed on tight tonnage, while Atlantic rates softened

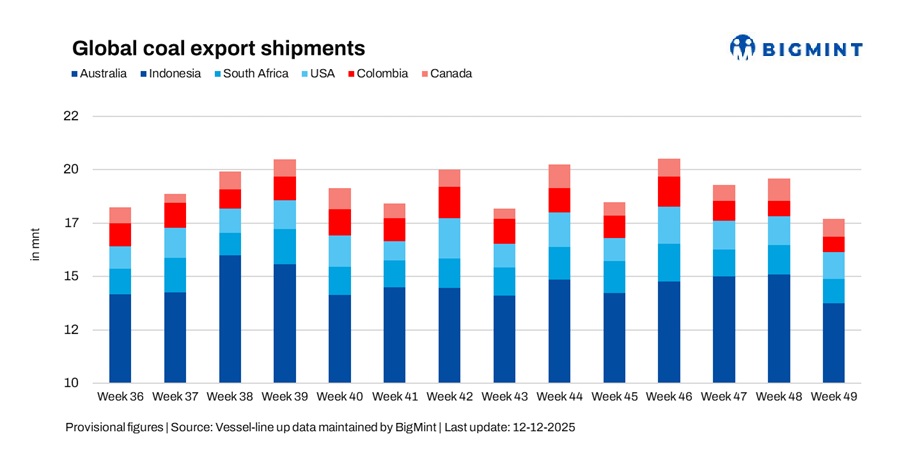

Global seaborne coal exports fell 10.2% w-o-w to 17.38 million tonnes (mnt) in the week ended 5 December from 19.36 mnt in the previous week, according to BigMint’s vessel line-up data. The decline was driven primarily by lower shipments from Australia, South Africa, and the USA, partially offset by Indonesia’s steady exports. Overall, uneven regional demand and contrasting Pacific-Atlantic freight trends influenced the weekly movement.

The w-o-w fall reflected weaker cargo nominations from Australia and South Africa, while Indonesia maintained export momentum due to operational efficiency and prompt cargo flow. Softer Pacific activity and mixed Atlantic sentiment kept growth constrained, despite smooth port operations across key regions.

Country-wise trends

Australia’s coal exports dip

Australia’s coal exports dropped 18.5% w-o-w to 5.91 mnt in the week ended 5 December from 7.25 mnt the previous week. Loadings at key ports — Newcastle (2.61 mnt), Gladstone (1.23 mnt), and DBCT (1.21 mnt) — remained steady, supported by smooth port operations and operational efficiency.

However, weaker interest from Indian and Northeast Asian buyers restrained shipment momentum. Pacific freight rates firmed slightly, but thin activity and few fixtures prevented a rebound in exports despite sound fundamentals.

On the demand side, Japan (2.03 mnt) and China (1.13 mnt) continued as major importers, with Yancoal (0.48) mnt and Glencore (0.46 mnt) emerging as leading shippers. Australia’s coal exports are expected to remain broadly stable in the near term, supported by operational efficiency and steady regional demand.

Indonesian shipments stay resilient

Indonesia exported 7.7 mnt of coal in the week ended 5 December, slightly down from 7.73 mnt the previous week. Strong loadings from East and South Kalimantan — led by Taboneo (1.72 mnt), Samarinda (1.18 mnt), and Bunati (1.07 mnt) — supported overall performance. Rising demand from China (2.72 mnt) and steady Indian interest (0.86 mnt) helped sustain flows.

However, muted Pacific freight sentiment limited sharper gains, and Indonesia faced constraints in replacing China’s reduced coal demand with buyers from Southeast Asia. Nevertheless, operational efficiency and prompt cargo nominations ensured exports remained resilient, highlighting the country’s ability to maintain steady shipments despite regional market challenges.

Looking ahead, Indonesia plans to impose a coal export tax of 1-5% next year to boost government revenue, potentially raising $1.2 billion. The move aims to balance state income while keeping the coal industry profitable, amid slower demand from China.

South Africa coal exports under pressure

South Africa’s coal exports fell 12.2% w-o-w to 1.14 mnt, with all shipments handled through Richards Bay. The decline was primarily driven by weaker demand from India (0.42 mnt) and other destinations, as buyers remained cautious amid softer spot prices and ample regional supply.

At the same time, the number of open vessels available for charter increased, giving buyers more options and adding pressure on export volumes. Despite this, Atlantic freight sentiment remained firm, supported by steady European demand and tighter tonnage in key Atlantic routes. Overall, while shipping conditions were favorable, subdued regional demand and growing vessel availability tempered South Africa’s export growth this week.

Adding to the short-term challenges, strong winds recently damaged equipment at Berth 801 of Richards Bay Coal Terminal, forcing a temporary halt in coal loading and a force majeure declaration. Repairs are expected to take about 14 days, pausing a key route for South Africa’s coal exports.

US coal shipments slip amid muted global buying

US coal exports fell to 1.17 mnt from 1.33 mnt, down by 12% reflecting subdued activity in European markets and cautious buying from India. European demand remained soft due to ample regional stockpiles and competitive pricing from alternative suppliers, while Indian buyers adopted a selective approach amid fluctuating domestic coal prices and freight costs.

Steady operations at key ports — Mobile (0.35 mnt), Baltimore (0.34 mnt), and Norfolk (0.33 mnt) — helped sustain shipments, but these could not fully offset the decline in overall volumes. The moderation in exports highlights how external demand conditions, rather than domestic operational constraints, are currently shaping US coal trade flows.

According to market sources, unless European and Indian buying picks up, short-term US export volumes are likely to remain under pressure despite robust port throughput.

Colombia loadings soften slightly

Colombia’s coal exports declined slightly to 0.71 mnt from 0.72 mnt last week, down by 2% primarily due to constrained cargo availability and subdued demand from European buyers. Lower shipments from key ports — Puerto Nuevo (0.40 mnt) and Puerto Bolivar (0.24 mnt) — contributed to the marginal drop. The limited cargo availability is attributed to ongoing operational adjustments by mining companies and fewer ready-to-ship inventories.

South Korea (0.16 mnt) remained the largest single destination, reflecting steady Asian demand, while Prodeco Group (0.40 mnt) and Cerrejon Mines (0.24 mnt) continued to dominate export volumes. The overall decline highlights a short-term softening in European appetite amid seasonal inventory management, even as Asian markets maintain moderate interest.

Canada loadings dip on softer asian demand

Canada’s coal exports declined to 0.81 mnt from 1.03 mnt by 21.5%, primarily due to a combination of limited cargo availability and selective buying from Northeast Asian markets. Japanese and South Korean buyers remained cautious amid ample regional supply and fluctuating coal prices, leading to fewer prompt shipments.

Despite the slowdown, port operations remained smooth, supporting steady loadings across major terminals: Roberts Bank (0.42 mnt), Prince Rupert (0.23 mnt), and Vancouver (0.16 mnt).

Although South Korea was the largest importer at 0.30 mnt, followed by Japan at 0.24 mnt. The decline reflects external demand conditions rather than operational constraints, and exports could rebound if Northeast Asian procurement activity strengthens in the coming weeks.

India coal freight firms on limited tonnage

Dry bulk coal freight rates to India firmed across major Pacific routes, driven by tighter vessel availability despite a slowdown in fixture activity. Australian and Indonesian routes benefited from limited tonnage, supporting higher charter levels, though muted enquiries and fewer active fixtures constrained shipment momentum.

In contrast, Atlantic freight softened amid subdued demand and balanced tonnage, even as rising bunker costs exerted upward pressure on shipping economics. These dynamics collectively influenced cargo deployment and pacing of exports across regions, resulting in a market that remained stable yet cautious.

While Pacific tightness is supporting rates in the short term, overall freight activity remains sensitive to regional demand fluctuations and vessel positioning, keeping charterers and owners alert to changing market conditions.

Outlook

Global coal exports are expected to remain broadly unchanged through December. Indonesia is likely to maintain export volumes, supported by operational efficiency and prompt cargo readiness. In contrast, Australian shipments may face headwinds from softer Pacific freight rates and cautious procurement by Indian buyers, which could temper export growth.

Atlantic exports from South Africa and the USA are expected to remain relatively stable, aided by firm freight sentiment and selective demand from key markets. Market watchers note that near-term export momentum will hinge on shifts in vessel availability, changes in regional buying patterns, and evolving freight dynamics.

Overall, while supply remains robust, cautious demand and freight considerations are likely to keep global trade flows balanced but sensitive to short-term fluctuations.

Leave a Reply