- Chennai scrap steady as steel demand stays weak

- Billet prices increased by INR 500/t w-o-w

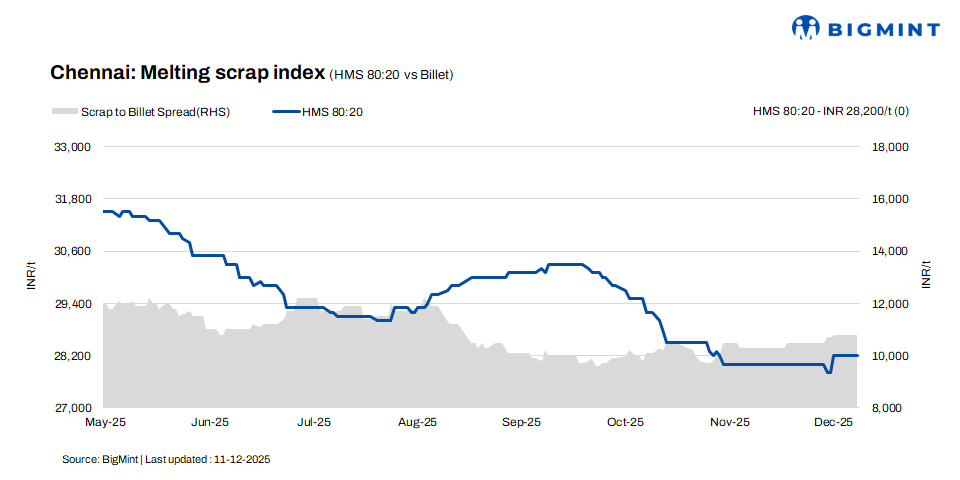

According to BigMint’s latest assessment, HMS (80:20) scrap prices in Chennai remained stable at INR 28,200/t on 11 December, with no changes recorded on either a d-o-d or w-o-w basis. Rebar prices also held steady at INR 43,000/t across both timeframes. In contrast, billet prices strengthened by INR 500/t w-o-w to INR 39,000/t, while remaining unchanged d-o-d. Overall, the market reflected a mixed sentiment, marked by stable trading activity and limited price fluctuations.

Imported, domestic market trends

Imported shredded scrap offers were reported at $340-345/t CFR Chennai, while buyers remained conservative with bids in the range of $330-335/t. HMS (80:20) scrap was quoted at $320-322/t, against bid levels of $315-320/t. Overall sentiment stayed weak, pressured by muted finished steel demand and limited procurement interest.

In the Chennai market, domestic HMS (80:20) scrap is trading at INR 27,500-28,500/t for spot deals with immediate payment. Transactions involving extended credit terms are commanding slightly higher prices of INR 28,500-29,000/t. According to market participants, most offers and concluded trades are concentrated within the INR 28,000-29,000/t range, reflecting tight liquidity and the increasing reliance on credit-driven pricing in scrap trade.

Buyer-supplier sentiments

According to a mill representative, major sponge iron producers are currently prioritising captive consumption rather than supplying material to the merchant market. In the billet segment, a notable bid-offer disparity has emerged, with buyers submitting lower bids amid weak finished steel demand, while sellers are holding higher offers to protect their conversion margins. Additionally, several key re-rollers in the region are either undergoing maintenance shutdowns or operating at reduced production levels.

According to market sources, with the rainy season still ongoing, demand for finished steel remains subdued. Major bulk buyers are refraining from placing large orders, and only small-volume deals are being concluded. Market participants anticipate that finished steel prices may soften further in the coming days.

According to a leading scrap supplier, HMS (80:20) scrap traded at INR 28,000-29,000/t, with variations driven mainly by payment terms. Persistent liquidity constraints have kept trade volumes moderate, while the ongoing monsoon season is prompting buyers to adopt a cautious approach, especially in the finished steel segment. Market sentiment remains subdued as major mills continue to hold elevated finished steel inventories of around 15-20 days.

Regional comparison

In the western India-based Jalna market, billet and HMS (80:20) scrap prices remained steady at INR 38,500/t and INR 29,300/t, respectively. Rebar prices, however, increased by INR 200/t to INR 43,500/t. Trade activity has softened slightly in recent sessions, although scrap availability at mills continues to be sufficient. According to market sources, the near-term outlook appears stable, with limited volatility expected as supply-demand conditions point toward continued range-bound pricing.

Outlook

Market participants anticipate domestic scrap prices to remain broadly stable in December, as suppliers continue to resist lower offers amid consistent procurement requirements. Any price movement is expected to be limited to INR 200-500/t, keeping overall market sentiment cautious.

Leave a Reply