- China restocking and firm freights boost weekly flows

- Higher exports from South Africa, Australia, Canada and Peru

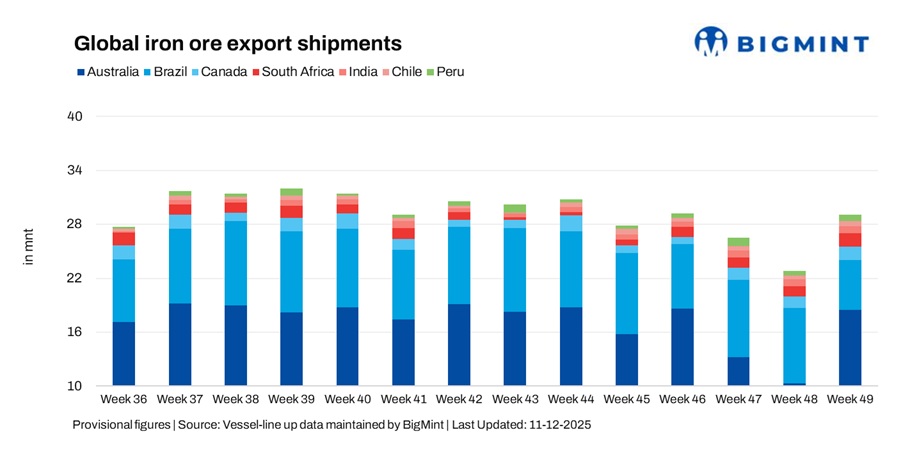

Global seaborne iron ore exports surged 27.9% w-o-w to 29.02 million tonnes (mnt) in the week ended 5 December 2025, up from 22.69 mnt the previous week, according to BigMint’s vessel line-up data. The rebound was led by strong shipments from Australia, South Africa, Peru, Canada, and Chile, while Brazil remained the only major supplier to see a notable decline.

Renewed restocking by Chinese mills, clearer visibility of winter demand, and a firmer freight market supported stronger w-o-w flows after the prior week’s slowdown.

Freight sentiment strengthened across key Capesize and Supramax routes, with tightening vessel supply, rising chartering interest, and firm Pacific and Atlantic activity boosting operator confidence.

While bunker costs and macro uncertainties kept some charterers cautious, overall improved freight conditions enabled steady vessel positioning and higher exports from Australia, South Africa, and Peru. In contrast, the firmer long-haul freight environment limited Brazil’s ability to scale up shipments, with some cargoes deferred amid cost considerations and muted fresh enquiries.

Country-wise trends

Australian iron ore rebounds on restocking demand

Australia’s iron ore exports rose a striking 79.4% w-o-w to 18.47 mnt in week 49 from 10.30 mnt in week 48, marking one of the sharpest recoveries of the season. Improved export momentum from Port Hedland (10.75 mnt), Walcott (4.21 mnt) and Dampier (2.92 mnt) supported the surge, aided by increased cargo nominations from major miners following the previous week’s pullback.

Supply was led by Rio Tinto (7.13 mnt), BHP (6.21 mnt) and FMG (3.91 mnt), as producers reinstated deferred stems and capitalised on improving Pacific market sentiment. Chinese mills lifted spot enquiries as restocking needs strengthened ahead of winter, restoring flow on key Western Australian routes. A firmer Pacific freight environment improved vessel availability for short-haul voyages to China, accelerating scheduling and boosting weekly shipments. Additionally, BHP has secured a $2 billion investment from GIP to upgrade its Pilbara power network, supporting cleaner and more reliable mine operations.

China was the largest importer of Australian iron ore at 14.46 mnt, followed by South Korea (1.99 mnt) and Japan (0.99 mnt), underscoring steady Northeast Asian demand.

Brazil iron ore slumps on long-haul weakness

Brazil’s iron ore exports fell sharply by 33.9% w-o-w to 5.53 mnt in week 49, down from 8.36 mnt in week 48, marking a notable pullback after two weeks of steady performance. Shipments from key terminals– Ponta da Madeira at 2.16 mnt and Tubarao at 1.51 mnt remained largely stable, but overall export momentum slowed as long-haul enquiries weakened and Chinese buyers became more cautious amid softer futures sentiment.

Major shippers included Vale (2.78 mnt) and CSN (2.06 mnt). Chinese mills, the top buyers at 3.28 mnt, focused more on inventory management ahead of winter, reducing prompt demand. Elevated freight costs on the Brazil-China route also limited fresh fixtures, contributing to the w-o-w drop despite adequate cargo availability. Early shipments from the Simandou project offered some support, though purchases from Northeast Asia declined.

Canada raises exports on healthy spot demand

Canada’s iron ore exports rose 16.8% w-o-w to 1.53 mnt in week 49, up from 1.31 mnt in week 48, supported by steady demand from both European and Asian buyers. Shipments were primarily led by Sept-Iles (0.92 mnt) and Port Cartier (0.61 mnt), where smooth vessel turnaround and efficient port operations helped maintain a consistent flow throughout the week.

Major shippers included AMNS (0.61 mnt) and Guinea & Nimba Mines (0.60 mnt). Healthy spot interest, along with stable North Atlantic freight conditions, allowed operators to secure fixtures early in the week, driving stronger export momentum. Among importers, The Netherlands (0.18 mnt) and Algeria (0.14 mnt) emerged as the largest buyers, reflecting ongoing demand for Canadian iron ore in both European and North African markets.

South Africa sees robust export growth

South Africa’s iron ore exports rose 32.4% w-o-w to 1.50 mnt in week 49, with all shipments moving through Saldanha Bay. The increase was driven by strong demand from Northeast Asian buyers and limited Capesize vessel availability on the South Africa-China route, which encouraged prompt fixing throughout the week.

Efficient vessel sequencing and improved coordination at the terminal further supported the smooth flow of cargoes, enabling South Africa to remain one of the strongest contributors to weekly global export growth. The major importers were The Netherlands (0.35 mnt) and Mauritius (0.35 mnt), reflecting consistent international demand for South African iron ore.

Indian exports rise w-o-w

India’s iron ore exports inched up by 1% w-o-w to 0.76 mnt in week 49, maintaining stable momentum following the slight dip in the previous week. Paradip (0.35 mnt) and Vizag (0.19 mnt) were the main contributors to shipments, supported by smooth port operations and efficient vessel turnaround.

However, limited fresh cargo nominations and seasonally subdued demand from Southeast Asia kept the overall increase modest. A steady Supramax freight market ensured timely vessel availability, allowing exports to continue without significant disruption. China remained the largest importer during the week, taking 0.23 mnt of Indian iron ore.

Chilean shipments record sharp recovery

Chile’s iron ore exports rose 44.2% w-o-w to 0.57 mnt in week 49, rebounding strongly from the subdued performance in week 48. Increased shipments from Huasco (0.20 mnt) and Totoralillo (0.20 mnt) supported the recovery, driven by steady Chinese spot enquiries and improved vessel availability across the Pacific.

The supply boost was further aided by a resurgence in short-haul fixtures, as manageable freight levels allowed miners to reinstate deferred stems and respond to renewed demand. A strengthening Pacific freight environment also helped streamline vessel allocation, enabling Chile to efficiently restore export momentum. China was the sole importer, taking the full 0.57 mnt shipped during the week.

Peruvian export flow normalises

Peru posted a strong recovery in iron ore exports, raising exports by 48.4% w-o-w to 0.67 mnt, reversing the decline seen in week 48. Shipments were entirely from San Nicolas (0.67 mnt), supported by fresh cargo nominations and improved vessel availability, which allowed operators to secure fixtures earlier in the week.

Shougang Hierro was the primary shipper, benefiting from a supportive mid-range Pacific freight market that enhanced scheduling and reinforced export consistency. China remained the largest importer, receiving 0.50 mnt, underlining Peru’s strengthened role in global iron ore flows during week 49.

Freight tightness boosts global iron ore flows

Freight markets strengthened across both basins this week, according to BigMint’s data, as strong Chinese restocking demand, tighter vessel supply, and heightened chartering activity lifted sentiment on major Capesize and Supramax routes. The strengthening momentum encouraged quicker vessel deployment from Western Australia, South Africa, and Peru, supporting higher w-o-w shipments from these regions.

While mixed bunker trends and winter-driven uncertainty kept some operators cautious, the overall improvement in freight fundamentals fostered better scheduling efficiency and steadier fixing. However, BigMint noted that the rise in long-haul freight economics limited Brazil’s ability to maintain higher export volumes, contributing to its sharp weekly decline despite stable port operations.

Outlook

Global iron ore exports are expected to remain supported in the coming weeks as China continues winter restocking and vessel supply across key basins remains moderately tight. Australia and South Africa are likely to maintain firm shipment levels, while Brazil’s recovery will depend on the stabilisation of long-haul freight to release deferred stems.

Short-haul Pacific and Indian Ocean routes are expected to benefit from healthy chartering interest, while mid-range suppliers such as Peru, Canada, and Chile may sustain steady flows, provided demand from Northeast Asia remains consistent. Overall, moderate tightness in shipping and ongoing regional demand are likely to keep global export momentum supported.

Leave a Reply