- Global scrap consumption down 4% y-o-y in 9MCY’25

- South Asia, Southeast Asia show positive growth

- Rising global DRI, HBI production may impact scrap demand

Morning Brief: Global ferrous scrap trade volumes, excluding intra-European trade, increased by over 2% y-o-y in January-September 2025 (9MCY’25), as per data maintained with BigMint.

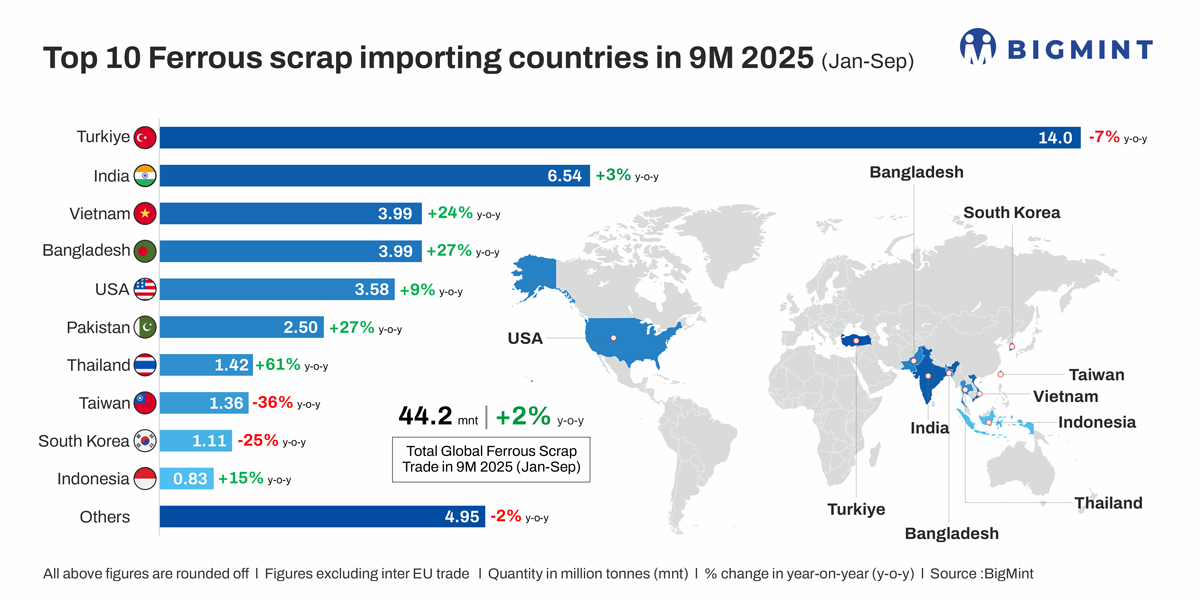

Data show that total imports by the leading scrap-buying countries inched up to around 44.2 million tonnes (mnt) compared to 43.2 mnt in 9MCY’24, showing some improvement despite a 2% decline in global crude steel production during the review period amid overall economic slowdown.

Ferrous scrap consumption also declined by 4% y-o-y to 447 mnt.

Steel & scrap dynamics in key geographies

Asia: The Asian seaborne scrap market remains subdued as strong Chinese steel exports continue to pressure regional pricing. As Chinese oversupply persists, steel exports continue to absorb output, delaying meaningful market tightening.

South Korea faces prolonged weakness as US tariffs escalate and domestic demand remains soft. Despite a $290 million export guarantee scheme, crude steel production fell 4% y-o-y in to 46 mnt in 9MCY’25. Oversupply and low consumption have pushed scrap suppliers to accelerate overseas sales.

Taiwan’s scrap imports dropped 36% y-o-y to 1.36 mnt on sluggish demand, cheaper billet inflows, and seasonal rainfall disruptions. Ferrous scrap demand across Thailand, Vietnam, Indonesi,a and Malaysia shows positive trends as import volumes improved as compared to 2024 levels, with activity concentrated in containerised cargoes.

Bangladesh has seen stable demand, with Japanese shipments up 250% y-o-y during January-September due to shorter lead times and flexible cargo sizes. Bangladesh has secured most of Japan’s last nine Kanto export tenders, witnessing a major shift in sourcing patterns.

India’s steel sector remains resilient despite monsoon disruptions and liquidity constraints. Crude steel production rose by 10% y-o-y in 9MCY’25 while imports declined by 15% in 10MCY’25 due to safeguard duty. Scrap imports remain stable, rising just 3% in 9MCY’25 due to a construction slowdown and greater use of domestic scrap. This is reflected in scrap consumption rising by 13% y-o-y during the review period.

United States

The US ferrous scrap market continues to battle weak demand, falling steel prices, and limited export support. In the June-September quarter, ferrous scrap prices were remarkably static even as tariffs kept domestic HRC demand firm near the 80% utilisation mark.

By September, however, the market began to soften. HRC, which had traded near $900/short tonne (st) earlier, slipped below $800/st as seasonal demand failed to materialise. Mills responded by reducing busheling prices by roughly $20/gross tonne, while dealers held firm on shred and cut grades, given concerns over inflows.

Weak sales, a cooling labour market, softening consumer confidence and planned mill outages continue to weigh on sentiment. Export markets remain flat, providing little relief.

UK & European scrap supply

Reduced buying interest from Turkiye pulled HMS and OA dockside prices down in the third quarter of 2025. European containerised prices softened as demand from Pakistan and India weakened, while domestic shredder operations faced increasing pressure from lower intake volumes.

Container business is expected to decline further on weak finished steel demand. Deep-sea activity is comparatively stable, with a slight recent uptick that is unlikely to last. Short-sea sentiment is the weakest, with some sources describing conditions as the most depressed since the COVID period.

Leading scrap importers

Turkiye: The country remained the largest scrap importer despite shipments falling by 7% in 9MCY’25 as billet imports edged up by 27% y-o-y in H1CY’25. Even as deep-sea bulk scrap imports rose by 6% y-o-y in 9MCY’25 the overall import volume was lower y-o-y.

India: India’s ferrous scrap imports rose modestly by 3% y-o-y in 9MCY’25. This was not only due to the increase in crude steel production, as mentioned, but also the decline in prices of US shredded scrap and European HMS (80:20). Domestic scrap consumption remained high as scrap prices have sunk to nearly five-year lows.

Moreover, the expansion in sponge iron consumption (over 40% between 2021 and 2024) is steadily altering India’s ferrous feedstock composition. Predictable supply, stable pricing, and consistent metallic yield have made sponge a preferred substitute for scrap, particularly in regions where it is more cost-effective. Many mills are optimising charge mixes toward sponge iron to mitigate exposure to volatile scrap.

Bangladesh: Bangladesh’s scrap imports increased by 10% y-o-y in 9MCY25 supported by lower prices. Imported bulk scrap prices have approached five-year lows, while containerised scrap followed a similar trend. A sluggish ship-breaking market has likely contributed to stronger demand for imported scrap.

East Asia: East Asian ferrous scrap imports showed mixed trends across regions in 9MCY’25, with Vietnam seeing a sharp surge, while Taiwan recorded a decline due to weak steel demand, high inventories, and cheaper alternatives. South Korea’s imports declined y-o-y despite a brief restocking-led uptick in September. Thailand experienced strong growth on higher scrap usage and improved supply, while Indonesia recorded moderate gains supported by policies encouraging greater scrap utilisation.

Scrap import outlook

A key thematic is, of course, the rise in global DRI and HBI production and its impact on scrap consumption.

Global ferrous scrap imports are expected to remain rangebound in the last quarter of CY2025, with some steady growth likely in Q4. Market sentiment will remain firm on tightening export regulations in key supplying regions. Prices may stay stable to slightly firm, with premium grades holding better value as mills prioritise yield. However, a sharp upside remains unlikely without a major supply disruption in key exporting hubs.

Risks ahead include weaker steel demand if the Chinese economy slows further, fresh trade barriers restrict supply, rising energy and collection costs lift scrap margins, and currency fluctuations across Asia alter import competitiveness. Turkish mills are expected to maintain moderate imports while relying more on billet/semis to manage costs due to firm scrap prices.

The EU’s scrap outflows are expected to remain limited under the Waste Shipment Regulation and new surveillance regimes. Rising EAF-based steelmaking capacity will keep more material within the region.

Scrap consumption is expected to extend its downtrend in Q4CY’25. BigMint data indicate usage of over 490 mnt in 10MCY’25, a 4% decline from 513 mnt in the same period of CY24. China is likely to see weaker usage if output-cut policies persist. The EU and the US are poised to lift consumption on strong EAF operations. Japan and South Korea remain constrained by subdued steel production.

Scrap consumption is expected to extend its downtrend in Q4CY’25. BigMint data indicate usage of over 490 mnt in 10MCY’25, a 4% decline from 513 mnt in the same period of CY24. China is likely to see weaker usage if output-cut policies persist. The EU and the US are poised to lift consumption on strong EAF operations. Japan and South Korea remain constrained by subdued steel production.

India’s rising crude steel output and a strategic shift toward higher scrap utilisation, driven by decarbonisation goals, are expected to support stronger demand.

Leave a Reply