- Tightening concentrate supply, strong structural demand sets the tone for CY’26

- TC/RCs fall to multi-year lows on supply shortage, unlikely to return to normal range

Copper is entering 2026 on a structurally sound footing after a turbulent but ultimately supportive 2025, with mine disruptions, falling treatment charges, and aggressive restocking by traders reshaped the global balance.

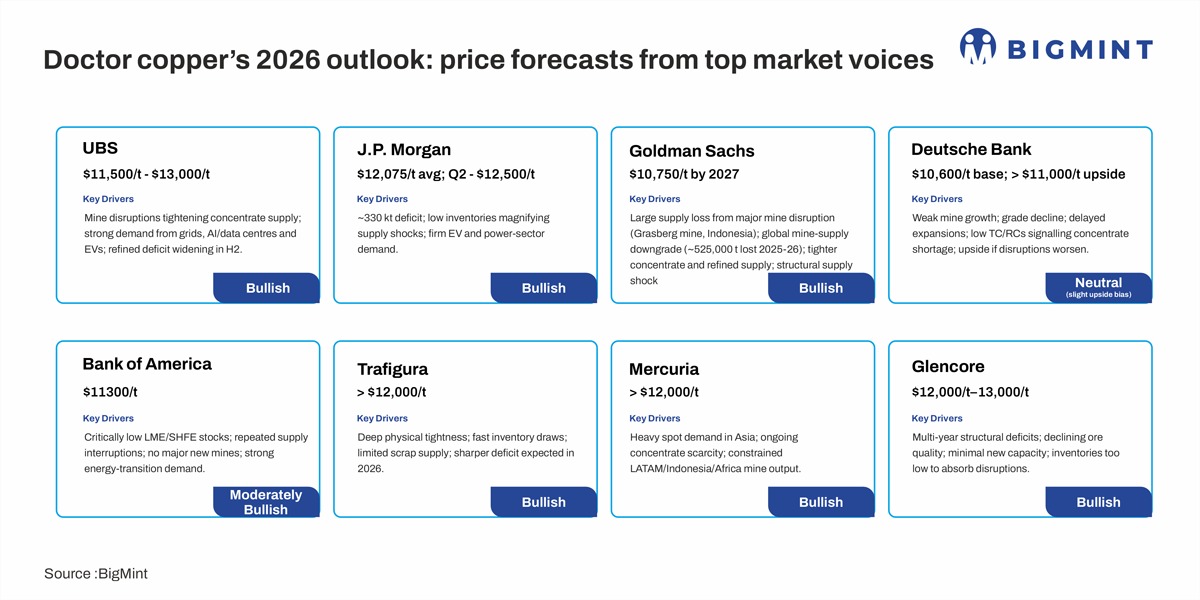

Prices moved sharply higher through mid-2025, driven by waves of supply tightness and falling inventories. As the New Year begins in a few days, several major trading houses expect copper to challenge – and potentially sustain – $12,000/t in 2026.

How did LME perform?

In 2024, average LME copper prices hovered around $9,200-9,500/t. In 2025, prices rose significantly, with averages in the range of $10,800-11,200/t, an increase of roughly 15-20% compared with 2024. Looking ahead to 2026, under current market conditions – tight supply, rising demand and strong restocking – the expected LME average is $11,500-13,000/t, which would imply a further gain of approximately 6-20% over 2025.

2025: Year of mine disruptions and tight concentrate balance

The most dominant theme of 2025 was the severe stress in the concentrate market. Spot TC/RCs collapsed to multi-year lows, with several deals settling near historic troughs as smelters competed aggressively for limited availability. A mix of unplanned outages, grade decline across key Latin American mines, and weather-related interruptions in Indonesia and Africa squeezed global concentrate flows.

Key disruptions included periodic stoppages at large Chilean operations, logistical delays in Peru, and ore grade deterioration at ageing mines, all of which reinforced the perception of a tightening supply chain. Even where expansions were announced, ramp-ups remained slower than projected, leaving smelters exposed. The result was a sharp drawdown in refined inventories across major exchanges, amplifying price volatility through the year.

TC/RC scenario

TC/RCs (treatment and refining charges) are the fees smelters charge miners to convert copper concentrate into refined metal. When TCs/RCs fall, it signals tight concentrate supply and squeezed smelter margins; when they rise, it indicates abundant feedstock.

In 2025, copper treatment and refining charges (TC/RCs) have collapsed to historically low levels, reflecting an extreme shortage of mined concentrate. Spot TCs have hovered near $10-20/t in earlier months, while several trades have even slipped into negative territory recently, meaning smelters are effectively paying miners to secure feedstock. This sharp decline highlights how aggressively concentrate supply has tightened while global smelting capacity continues to expand, putting significant pressure on smelter margins.

Looking ahead to 2026, TC/RC levels are expected to remain under heavy pressure. Mine supply growth is limited, concentrate availability is likely to stay constrained, and new smelting capacity coming online will only deepen the imbalance. As a result, TC/RCs are unlikely to return to normal ranges soon. Persistently low fees could force some smelters to reduce throughput, further tightening refined copper supply and adding upside risk to prices going into 2026.

Demand resilient amid mixed economic signals

Despite macroeconomic headwinds underlying copper demand held stronger than many expected in 2025. Renewable energy projects, grid expansion programmes, data-centre construction, and EV penetration continued to absorb refined material at an elevated rate. China’s stimulus measures in the second half of the year provided additional support, particularly in the electrical machinery and infrastructure segments.

Even with sluggish property markets in parts of the world, the broader trend of electrification proved powerful enough to stabilise demand. By late 2025, copper’s role as a strategic and green-transition metal had fully returned to the forefront of market sentiment.

2026: Deficit risks rise as demand strengthens

Most major institutions expect copper to trade in the $10,500-$13,000/t range in 2026, with strong upside potential if supply tightens. Forecasts point to a 250,000- 330,000 t refined deficit, reflecting slow mine growth, lower concentrate availability, and limited new project start-ups.

Demand, meanwhile, is broad-based and accelerating. Data centres, AI-driven power infrastructure, renewable grids, semi-conductor expansion, and EV charging networks are becoming major copper consumers—adding pressure on an already tight market. Traditional electrical sectors in emerging economies are also expanding faster than expected.

If 2025 was a year of disruption-driven tightness, 2026 is shaping up to be a year in which structural demand is likely to overtake supply growth with renewed force. With mine challenges unresolved, TC/RCs staying soft, inventories at multi-year lows, and traders positioning aggressively, copper appears to be entering a cycle where $12,000/t is no longer a peak – but a realistic benchmark for the year ahead.

Leave a Reply