- ADC12 imports drop by 51% y-o-y in 10MCY’25

- Scrap-to-alloy spread supports producer margins

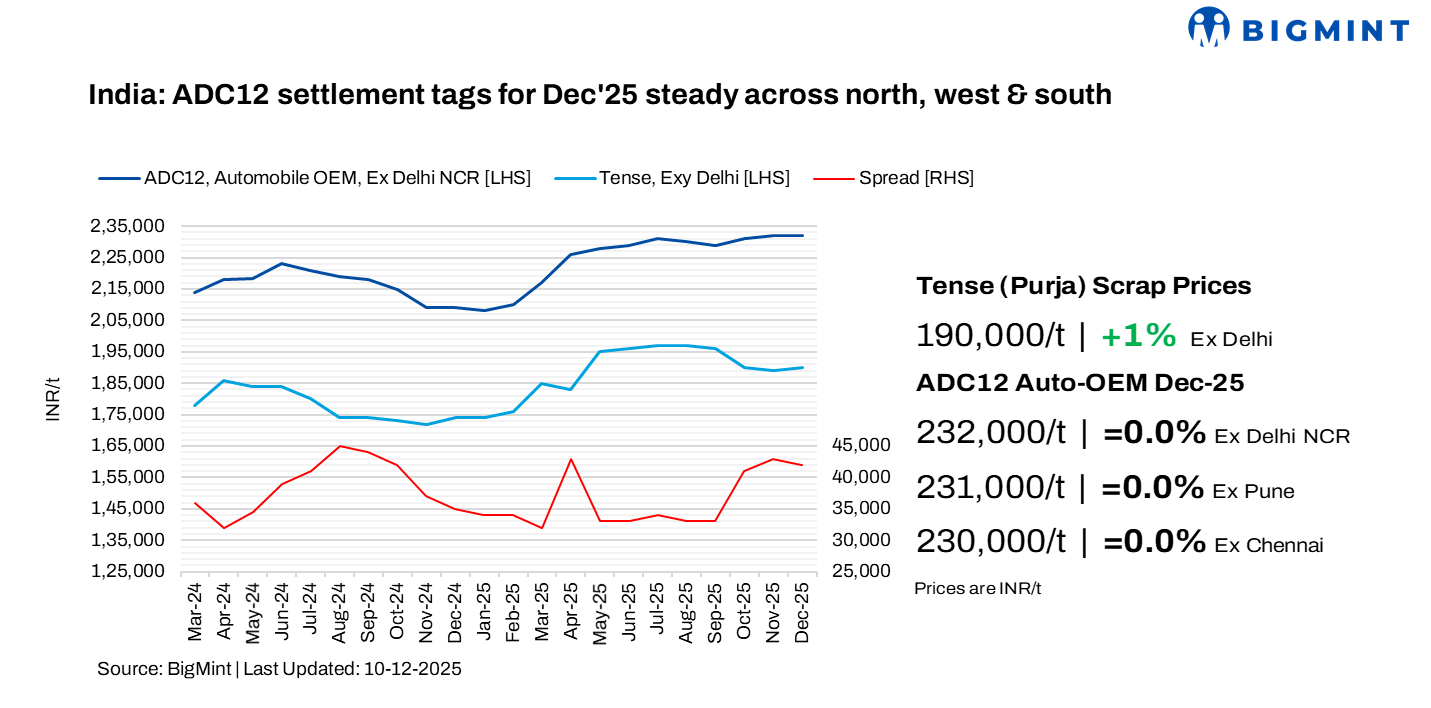

India’s aluminium ADC12 alloy ingot prices remained stable m-o-m in December 2025 supported by steady automotive demand and the typical year-end slowdown, which limited any further upward movement in prices.

BigMint’s monthly assessment for OEM-grade ADC12 showed slight price hikes across key regions:

- Delhi: INR 232,000/t, stable m-o-m

- Pune: INR 231,000/t, stable m-o-m

- Chennai: INR 230,000/t, stable m-o-m

These prices are based on 30-day payment terms.

The spread between scrap and semi-finished products saw a m-o-m increase of INR 42,000-45,000/t in both Delhi NCR and Chennai on lower domestic scrap prices and steady alloy prices due to firm auto demand.

Market insights

ADC12 offers across northern and western India were recorded in the range of INR 233,000-234,000/t, while bids hovered between INR 231,000-232,000/t levels in the north and INR 230,000-231,000/t in the west. Meanwhile, offers in the south hovered between INR 231,000-232,000/t and bids were heard between INR 229,000-230,000/t. Most OEMs are still finalising their December procurement contracts, with negotiations ongoing.

A secondary alloy producer said, “ADC12 demand stayed firm through November but is expected to ease slightly in December, largely due to the usual year-end slowdown and scheduled maintenance shutdowns at several automakers during this period.”

Another ADC12 producer from south India informed that the spread between ADC12 and Tense has widened, supporting stronger profit margins for alloy makers. Most south-based producers are preferring domestic scrap–not only from Chennai but also from other parts of south India–in an effort to secure lower-priced material.

Domestic casting scrap prices have remained steady and are still lower than both north India’s and Chennai’s average levels from two months ago. This price advantage has helped maintain healthy profit margins for alloy producers.

Alloy imports plunge y-o-y

Imports: India’s ADC12 alloy market continued to witness a sharp contraction in imports during the first 10 months of 2025 (10MCY’25), with inbound volumes falling 51% y-o-y. Total ADC12 imports stood at 10,250 t, down significantly from 20,996 t in 10MCY’24.

LME price movements

LME aluminium prices averaged at $2,885/t in early December, marking a $40/t or 1.5% gain m-o-m from the previous month.

Meanwhile, LME aluminium inventories witnessed outflows in early December, with stocks down by 3% at 530,786 t against 547,261 t in the previous month.

Aluminium prices strengthened as tightening supply aligned with improved demand signals. Chinese smelters approached government-imposed capacity limits thereby capping output potential, while SHFE inventories fell sharply, underscoring supply tightness.

Raw material price trends

In early December, prices of aluminium scrap remained rangebound m-o-m. US-origin Tense (6-7%) scrap stood at $2,000/t, down by $5/t m-o-m, while UK-origin Wheels rose by $15/t to $2,660/t. Meanwhile, Zorba 95/5 from the UK stood at $2,270/t CFR west coast, India, up by $20/t m-o-m.

The firm LME trend–driven by supply disruptions and a bullish outlook in the global aluminium market–has kept imported scrap offers elevated, even as overall scrap prices remain largely rangebound.

India’s overall aluminium scrap imports increased by 14% to 1.65 mnt in 10MCY’25 from 1.44 mnt in 10MCY’24. Major importers also scaled up procurement amid a shortage of aluminium scrap during the initial months of the year, particularly following the imposition of US tariffs.

Most grades, except for Talk, witnessed an increase in arrivals in 10MCY’25 despite price volatility.

In the domestic market, Tense scrap prices gained INR 1,000/t m-o-m to INR 190,000/t in Delhi, while in Chennai prices were assessed at INR 185,000/t exw, steady m-o-m. The stability in domestic scrap prices followed improved scrap availability in the local market and stricter GST compliance enforcement, both of which contributed to downward pressure on prices particularly in the southern region.

Silicon price trends

According to BigMint’s assessment, China’s 553-grade silicon prices remained largely steady m-o-m at $1,360/t CFR Mundra, driven by steady demand.

Outlook

The ADC12 market is expected to remain slow through the rest of December, with prices staying largely stable due to the typical year-end lull and maintenance shutdowns at several automakers. Despite firm auto demand, buying sentiments are expected to remain slow as participants await major automakers’ January 2026 price settlements. Market activity is likely to pick up after the New Year.

Leave a Reply