- Rebar inventories drop 30% amid steep production cuts

- HRC suppliers face shrinking demand during off-season

- Iron ore, coke costs remain firm, providing cost support

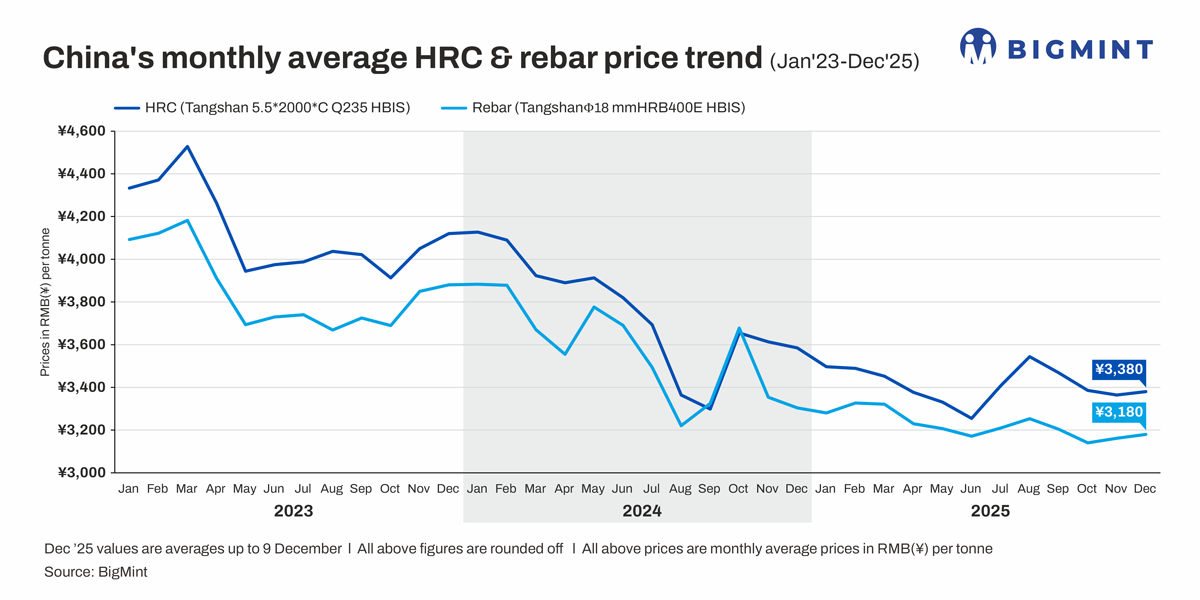

Morning Brief: Chinese hot-rolled coil (HRC) and rebar prices showed divergent movements m-o-m in November 2025. Tangshan’s benchmark HRC prices fell by RMB 22/tonne ($3/t, 0.6%) m-o-m to a monthly average of RMB 3,364/t ($476/t), while rebar was up by RMB 21/t ($3/t, 0.7%) at RMB 3,162/t ($448/t).

As seen in previous years, mills in north China had been mandated to reduce production early in the month, but the impact of these was more pronounced in the rebar segment. Producers of rebars had been struggling with narrow, even negative, margins as opposed to those of HRCs, whose sales could fetch some profits. This led mills to reduce rebar production to a higher degree.

Meanwhile, raw material costs remained steady m-o-m. In November, Quasi-Grade I met coke prices were at RMB 1,556/t ($220/t) exw-Tangshan, up by RMB 100/t ($14/t, 7%), while Australian premium hard coking coal increased by $6/t (3%) m-o-m to $197/t FOB Hay Point. Iron ore edged down by $1/t (1%) m-o-m to $105/t CNF Rizhao.

Snapshots of HRC, rebar price movements in Nov’25

HRC prices dip m-o-m on need-based demand: Price movements largely followed a V-shaped trajectory in November.

Considering weekly average prices, the first half of the month recorded a fall of INR 50/t ($7/t, 1.5%) to RMB 3,348/t ($474/t) during 10-14 November compared to RMB 3,398/t ($481/t) between 27-31 October.

At the start of the month, Tangshan-based mills had reduced production as part of air pollution control measures, while shrinking profit margins had dampened production momentum, according to Mysteel.

However, these ultimately proved insufficient to balance supply and demand, as manufacturing sentiment remained weak. The production cuts were also limited for HRCs in comparison to rebars, as mills could secure better margins from HRC sales. LangeSteel indicated that orders from downstream segments, such as the automotive and home appliances industries, slowed, as they approached the end of their traditional peak season of production.

Subsequently, prices rebounded (+0.8%) to RMB 3,374/t ($478/t) during 24-28 November, driven by optimism around upcoming policy announcements and macroeconomic sentiment. For example, China-US trade talks in Malaysia, expectations regarding the 15th Five-Year Plan, and potential US interest rate cuts boosted industrial confidence.

However, these factors were unable to reverse the decline recorded earlier, and prices closed the month lower m-o-m. Exports also failed to offset poor domestic demand due to the implementation of protectionist measures overseas.

Lange Steel data suggests that China’s total HRC social inventory stood at 2.6 million tonnes (mnt) on 26 November, down slightly by 4% from 29 October’s 2.7 million.

Rebar prices rise m-o-m on supply cuts: Chinese rebar prices dipped by RMB 2/t ($0.3/t, 0.06%) w-o-w to a weekly average of RMB 3,152/t ($446/t) during 3-7 November. Prices then rose 0.6%, settling at RMB 3,172/t ($449/t) during 17-21 November, following which they fell 0.6% to RMB 3,154/t ($447/t).

The mid-month increase followed production cuts, undertaken due to narrow profit margins, especially among electric furnace units, and production restrictions in the Beijing-Tianjin-Hebei area to control air pollution.

Subsequently, sentiment improved, as inventories began to reduce despite need-based purchases. Shortages also emerged for some grades, and dealers were able to hold offers firm. However, as the month-end approached, buyers showed resistance to the higher prices, leading to a correction.

Meanwhile, demand remained weak throughout November, with the construction industry entering its traditional off-season. Cold weather, with heavy rain and snow in the north, prevented outdoor construction activities.

According to Lange Steel data, on 26 November, Beijing’s construction material inventory stood at 288,600 t, falling by 30% from 29 October’s 410,000 t.

Daily construction steel production from major North China-based producers fell by 26% to 35,500 t during the fourth week of November from 48,000 t during the fifth week of October.

Outlook

Both HRC and rebar prices have averaged higher till 9 December, at RMB 3,380/t ($479/t) and RMB 3,180/t ($450/t), respectively.

For HRCs, this uptrend may not last during the rest of the month because of two key factors: First, demand will remain subdued with the market in its off-season. Secondly, due to the year-end, producers may intensify efforts to offload stocks and recover costs. This may push sellers to slash offers. As per LangeSteel, the slight increase in December was due to environmental inspections, though this supply tightening may be offset by weak demand.

Mysteel’s analysis suggests that China’s construction steel prices may rise further, as stocks continue to be low and sentiment remains positive. Given winter generally witnesses poor construction steel demand, this expectation suggests a divergence from traditional trends. However, the report also indicates that demand may falter in the second half, as cold weather could stall construction activity until spring.

Optimism also persists regarding policy announcements expected in December. While a potential Fed interest rate cut is a key external factor, the Central Economic Work Conference in China is also anticipated to boost industrial sentiment with announcements of measures to enhance domestic demand. However, it is unclear if they will boost prices substantially.

Leave a Reply