- Tier-1 mills roll over HRC and CRC list prices for Dec’25

- Rebar market recovers: BF-route trade prices up INR 700/t w-o-w

- Odisha iron ore prices in Dec rise nearly 8% from Oct average

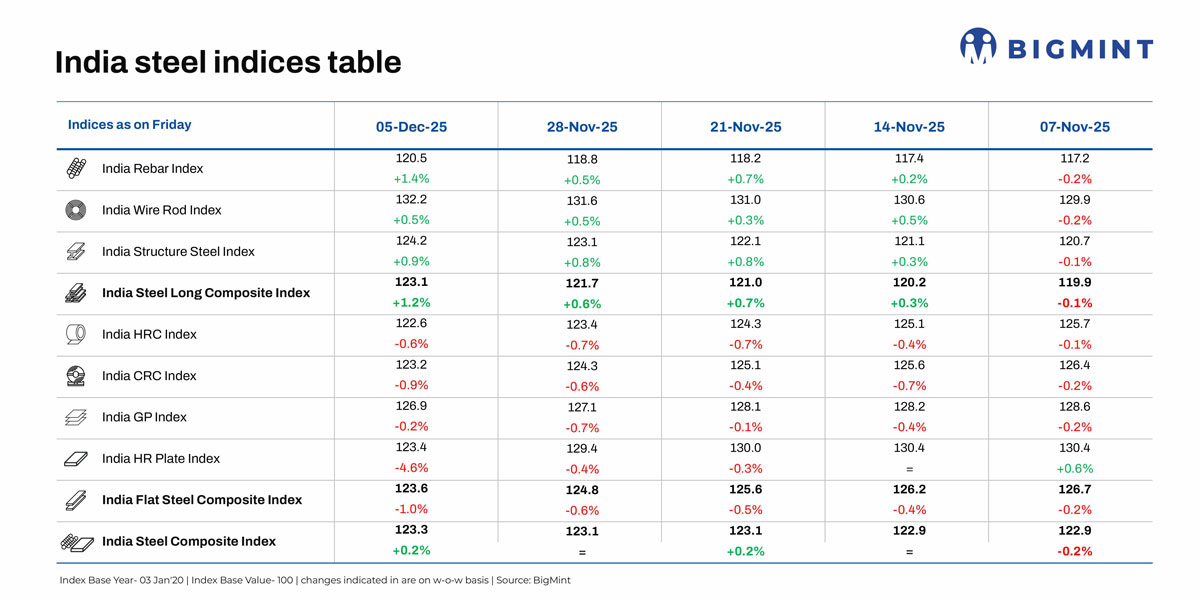

Morning Brief: Steel prices and market conditions in India remain depressed for a protracted period, with prices hovering at five-year lows; however, BigMint’s India steel composite index, in many ways a barometer of the domestic market, is showing signs of a gradual recovery that may be extremely slow but is certainly hard to miss.

The index inched up 0.2% w-o-w on 5 December 2025 while still tottering at multi-year lows in the middle of a global downturn characterised, mainly, by the steady decline in Chinese demand for, and production of, steel. Weak global demand and steel export prices are weighing on domestic prices, especially of flats products. Although domestic demand remains rock solid, it still happens to be trailing the surge in supply growth.

Highlights of price movements

Rebar market shows revival signs: Induction Furnace (IF) rebar prices recorded an increase of INR 200-1,300/t w-o-w across regions last week. Trading remained moderate, with manufacturers quoting higher. Buyers continued to procure actively supported by demand from both the project segment and retail markets. Mill inventories declined, currently estimated at around 8-12 days across markets.

As inventory pressure eased, fresh bookings picked up and semi-finished steel prices provided support to rebar prices. Despite average demand market sentiments turned optimistic toward the end of November riding on expectations of continued price stability in the days ahead.

Trade-level BF rebar prices increased by INR 700/t ($8/t) w-o-w to INR 47,000/t ($522/t) exy-Mumbai, as on 5 December. Prices are exclusive of GST at 18%. Some of the Tier-1 mills increased prices by up to INR 1,000/t ($11/t) for deliveries in December compared to prices at the end of November, sources informed BigMint. Meanwhile, others rolled over their prices against November levels.

Iron ore prices firm up: Incidentally, the firming up of domestic iron ore prices provided additional support to steel prices. BigMint’s Odisha iron ore fines (Fe62%) index increased by 7.5% in early December from average prices in October. This reflects stronger buying interest from sponge iron and pellet producers amid tight supply. Prices firmed up especially in key producing states as mills sought to secure fresh ore for winter operations and possible disruptions.

Flat steel prices remain subdued: BigMint’s benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) fell by INR 400/t ($4/t) w-o-w to INR 45,800/t ($509/t) on 2 December against INR 46,200 ($513/t) on 25 November. CRC (IS513, Gr O, 0.9 mm/CTL) prices declined by INR 300/t ($3/t) w-o-w. HRC trade prices declined in some markets while remaining rangebound in others.

The Tier-1 mills rolled over HRC and CRC prices for December sales compared with late-November levels. M-o-m, trade prices of HRC dropped INR 1,200/t in November versus INR 1,000/t for CRC.

Export allocations to the EU for Q4CY’25 are already exhausted keeping India’s HRC export index flat as mills refrain from issuing fresh offers. CBAM-related uncertainties are another thorn in the side of exporters. Muted sentiments in the Middle East due to regional holidays have reinforced dull export demand, which is affecting HRC prices. Imports, too, have edged down significantly.

On the domestic front, trade demand remained sluggish due to liquidity constraints, with buyers restricting procurement to need-based volumes. In view of capped export prospects, subdued overseas demand, and high domestic supplies, mills opted to hold list prices rather than going for an upward revision.

Outlook

Optimism hinging on key shifts in Chinese economic policies in the wake of the 15th five-year plan period and stimulus expectations are being tempered by production declines, winter cuts, and weak demand. This, coupled with a general deterioration in market conditions in Japan and the EU and the delay in finalising of a trade deal with the US, is hardly conducive to an overall recovery in steel prices especially as the Christmas and New Year slowdown is about to set in.

However, positive domestic economic policies and long-awaited changes in the tax structure and interest rates will drive steel demand in Q4FY’26, not to mention the expected acceleration in infra and construction momentum ahead of the fiscal year-end. Therefore, Indian steel prices are likely to be affected by divergent domestic and global trends in the January-March quarter, with the general expectation of a slow yet steady recovery.

Leave a Reply