- Mills hold prices on muted sentiment

- Export market weakness weighs on domestic prices

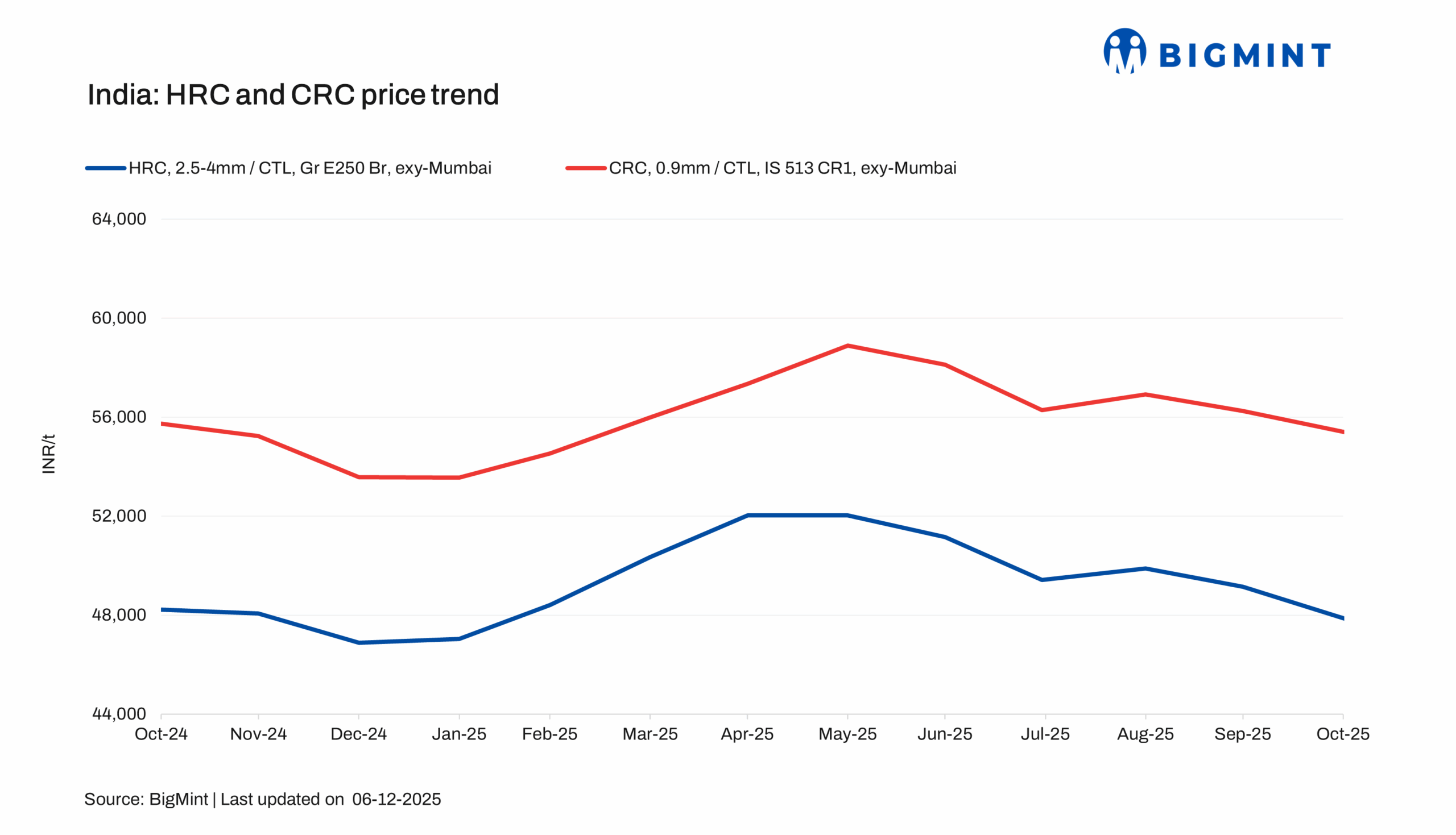

Leading Indian steelmakers have rolled over hot-rolled coil (HRC) and cold-rolled coil (CRC) prices for December 2025 sales compared with late-November list levels.

List prices of HRC (2.5-8 mm, IS2062, Gr E250 Br) ranged within INR 46,950-48,500/t ($522-539/t) ex-Mumbai. CRCs (0.9 mm, IS513 CR1) were at INR 53,200-55,750/t ($591-620/t).

BigMint’s benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) fell by INR 400/t ($4/t) w-o-w to INR 45,800/t ($509/t) on 2 December against INR 46,200 ($513/t) on 25 November.

CRC (IS513, Gr O, 0.9 mm/CTL) prices declined marginally by INR 300/t ($3/t) w-o-w to INR 54,000/t ($600/t) on 2 December against INR 54,300/t ($603/t) the week before. These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

M-o-m, trade-level HRC prices declined by INR 1,200/t ($13/t) to INR 46,750/t ($520/t) in November compared with INR 47,900/t ($532/t) in October. CRC prices also eased, dropping by INR 1000/t ($11/t) to INR 54,800/t ($609/t) in November, down from INR 55,800/t ($620/t) in October.

HRC-CRC spread

The gap between CRC and HRC stood at around INR 8,087/t ($90/t) exy-Mumbai in November as compared to INR 7,528/t ($84/t) exy-Mumbai in October 2025.

Why did mills roll over prices for Dec’25?

1. Export channels offer limited support: Mills rolled over list prices for December as export and domestic market conditions offer little scope for an upward adjustment. Export allocations to the EU for Q4CY’25 have been fully exhausted keeping Indian HRC export indices flat as mills refrained from issuing fresh offers. The steady trend was reinforced by muted buying in the Middle East due to regional holidays and persistently weak demand. Additional pressure stemmed from CBAM-related uncertainties and a dip in import arrivals, which limited competitive signals.

2. Domestic trade market conditions remain subdued: On the domestic front, trade demand remained sluggish due to liquidity constraints, with buyers restricting procurement to need-based volumes. Given the combination of capped export opportunities, subdued overseas activity, and weak domestic sentiment, mills opted to maintain list prices rather than implement any upward revision for November.

Outlook

HRC prices are expected to remain stable, with limited upside as export channels stay constrained and domestic trade buying continues on a need-based pattern. Unless export activity improves or downstream demand gains traction mills are likely to hold prices at current levels through December.

Leave a Reply