- Met coke prices rise by INR 200/t w-o-w in eastern India

- Indian BF mills’ rebar prices show mixed trends in early-Dec

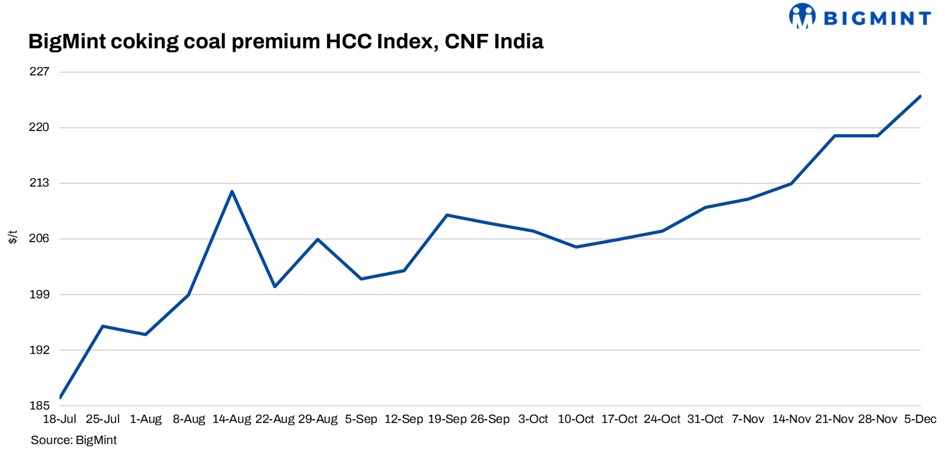

BigMint’s premium hard coking coal (PHCC) index was assessed at $224/tonne (t) CNF Paradip, India, on 6 December, up by $5/t against the previous assessment on 28 November 2025.

Meanwhile, bid-offer gaps persisted amid subdued steel market sentiment. Offers for Australian-origin material rose to around $220/t CFR India, driven by global cues, but buying interest was limited at these levels, with bids relatively lower, according to a source from a steel mill.

Globally, coking coal prices strengthened amid recent deals concluded for China, which has pushed up overall offers, sources said.

BigMint has consolidated its Prime Hard Coking Coal (PHCC) CFR India Index to include material of all origins, including US, Canada, Mozambique, Australia — normalised for quality and freight. With India steadily reducing its reliance on Australian PHCC and increasing imports from alternative sources, this update ensures the index accurately reflects evolving market dynamics and trade flows.

Factors impacting imported coking coal prices

Met coke prices firm up in eastern India on higher coking coal costs: The Indian metallurgical coke market displayed a mixed picture during the week ending 4 December 2025, with prices firming up in eastern India, while they were stable in the west. In the east, BF-grade (25-90 mm) met coke rose by INR 200/t w-o-w to INR 32,000/t ex-Jajpur, supported by higher offers. Meanwhile, in western India, prices were unchanged w-o-w at INR 30,200/t ex-Gandhidham, reflecting steady buyer interest. Foundry-grade met coke remained at INR 36,000/t ex-Rajkot, indicating shifts in niche demand.

Earlier, on 4 December, Australian premium hard coking coal (PHCC) prices had moved up by $3/t w-o-w to $202/t FOB, offering cost-side support to domestic coke values.

Chinese coke market remains weak: China’s coke market continued to feel the pressure of weak sentiment, as raw coal supply increased and procurement remained cautious. Trading activity stayed sluggish, with online bids slipping further, underscoring expectations of prolonged softness. Even though coking coal prices improved, coke offtake weakened as steel mills battled poor profitability, subdued steel demand, and more frequent maintenance shutdowns. Rising inventories and lower molten iron output deepened pessimism, signalling that near-term improvement in fundamentals remains unlikely.

Mixed pricing signals seen for Indian BF-rebar prices in early-Dec’25: India’s blast furnace (BF) rebar market witnessed mixed pricing signals in the week ended 5 December. Some leading primary mills increased rebar prices by up to INR 1,000/tonne (t) ($11/t) for deliveries in the first two weeks of December compared to prices at the end of November, sources informed BigMint. Meanwhile, others rolled over their prices against the previous month’s levels. Post revision, list prices stood at INR 47,000-48,500/t ($522-539/t) on landed basis. It should be noted that mills had offered discounts/rebates to augment sales last month.

Leave a Reply