- Weak Pacific demand limits Australian growth

- Indonesia posts strong rebound, supporting overall volumes

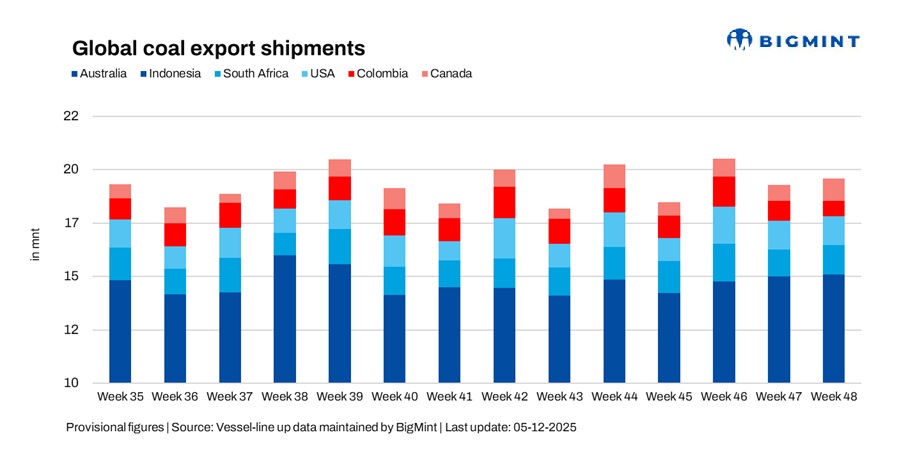

Global seaborne coal exports increased 2.1% w-o-w to 19.36 million tonnes (mnt) in the week ended 28 November from 18.96 mnt in the previous week, according to BigMint’s vessel line-up data. The rise was driven primarily by a rebound in Indonesian shipments, while gains from the US, South Africa, and Canada helped offset declines from Australia and Colombia. Overall, mixed regional demand and soft Pacific freight sentiment shaped the weekly flow.

The marginal rise in total exports reflected stronger cargo nominations from Indonesia and North American ports, while weaker Indian and Northeast Asian buying kept Australian shipments contained. Softer Pacific freight rates limited aggressive positioning of vessels on Australia-India and Indonesia-India routes, capping export growth despite smooth port operations.

Meanwhile, Atlantic rates stayed relatively firm, supporting South African and US shipments and maintaining momentum in those regions.

Country-wise trends

Australian exports ease amid subdued Pacific demand

Australia’s coal exports fell 2.8% w-o-w to 7.25 mnt in the week ended 28 November from 7.46 mnt the previous week. Loadings at key ports—Newcastle (2.69 mnt), Gladstone (1.45 mnt), and DBCT (1.31 mnt)–remained steady, supported by smooth port operations and favorable weather.

However, weaker interest from Indian steel buyers and softer spot activity in Japan restrained shipment momentum. Soft Pacific freight rates also limited aggressive vessel deployment, preventing a rebound in exports despite sound operational fundamentals.

On the demand side, China (2.09 mnt) and Japan (1.64 mnt) led import activity, with Glencore (1.01 mnt) and BHP (0.60 mnt) once again emerging as major shippers. Australia’s non-coking coal exports are expected to remain broadly stable in the near term, supported by China’s steady buying and seasonal demand in Southeast Asia.

Indonesia posts strong rebound on improved cargo flow

Indonesia’s coal exports surged 5.6% w-o-w to 7.73 mnt up from 7.33 mnt the previous week. The increase was supported by higher nominations from East and South Kalimantan and efficient vessel turnaround.

Taboneo (1.24 mnt) and Bunati (1.14 mnt) led loadings, reflecting strong operational momentum at major ports.Rising demand from China (3.04 mnt) and steady interest from India (1.15 mnt) helped maintain export growth.

However, muted Pacific freight sentiment limited a sharper rise in fixtures. Market sources also said Indonesia can’t replace China’s falling coal demand by selling to Southeast Asia, as the regional market is too small and moving toward clean energy. Without long-term planning, Indonesia risks losing export revenue and facing economic challenges in coal-producing regions.

South African exports recover modestly

South Africa shipped 1.30 mnt in the week up 4% from 1.25 mnt the previous week. Improved rail-to-port flow and sustained Atlantic freight support contributed to a modest rebound.

All loadings came from Richards Bay (1.30 mnt), reflecting smooth operational performance at the port. Softer demand from major Asian buyers, along with selective procurement in India, capped export momentum despite firm seaborne prices and tight availability in some grades.

India remained the largest importer (0.50 mnt), with gains in sponge iron prices stimulating selective purchases. Exports are likely to remain stable through December as Indian demand gradually picks up for early-2026 deliveries.

Colombia sees continued slowdown

Colombia’s coal exports declined further to 0.72 mnt in the week from 0.88 mnt in the previous week, reflecting lower cargo availability at Puerto Nuevo (0.36 mnt) and Puerto Bolivar (0.27 mnt).

Limited short-haul buying interest from Europe kept shipments constrained, despite stable terminal operations.

Brazil (0.20 mnt) and South Korea (0.15 mnt) were the main destinations, with Prodeco Group (0.41 mnt) and Cerrejon Mines (0.27 mnt) emerging as leading shippers.

US exports edge up

US coal exports rose slightly to 1.33 mnt in week 48 from 1.31 mnt in week 47, supported by steady demand from India (0.32 mnt) and the United Kingdom (0.12 mnt).

Reduced European activity continued to limit stronger gains, keeping overall growth modest.

Operational stability at Norfolk (0.40 mnt), Baltimore (0.36 mnt), and Mobile (0.35 mnt) helped support the modest rise in exports.

Canada posts significant gain

Canada exported 1.03 mnt in the week, up 40% from 0.73 mnt in the previous week. Improved rail availability and strong port throughput supported the surge.

Loadings were led by Roberts Bank (0.54 mnt), Vancouver (0.42 mnt), and Prince Rupert (0.07 mnt), reflecting smooth operational performance.

Northeast Asian demand, particularly from Japan (0.47 mnt) and China (0.34 mnt), underpinned the increase, with Elk Valley Resources (0.42 mnt) emerging as the leading shipper.

Coal freight rates remain mixed

Coal freight rates to India showed a split trend during the week. Pacific rates softened amid weak regional demand, ample vessel availability, and muted Indian procurement, limiting export growth from Australia and Indonesia.

In contrast, Atlantic rates remained firm, supported by tighter tonnage and consistent demand, enabling South African and US coal shipments to sustain momentum.

Higher bunker costs added additional pressure, particularly on longer-haul voyages, keeping freight economics under scrutiny and moderating overall shipment activity.

Outlook

Global seaborne coal exports are likely to remain steady to slightly positive in December. Firm Atlantic sentiment may support US and South African volumes, while soft Pacific rates could cap growth from Australia and Indonesia.

Buyers in India and Northeast Asia are expected to remain cautious, and any significant shift in demand or tightening in vessel supply will be critical to driving further export momentum.

Leave a Reply