- Production drops despite higher Sindh output

- Punjab’s 4.49% fall drives national decline

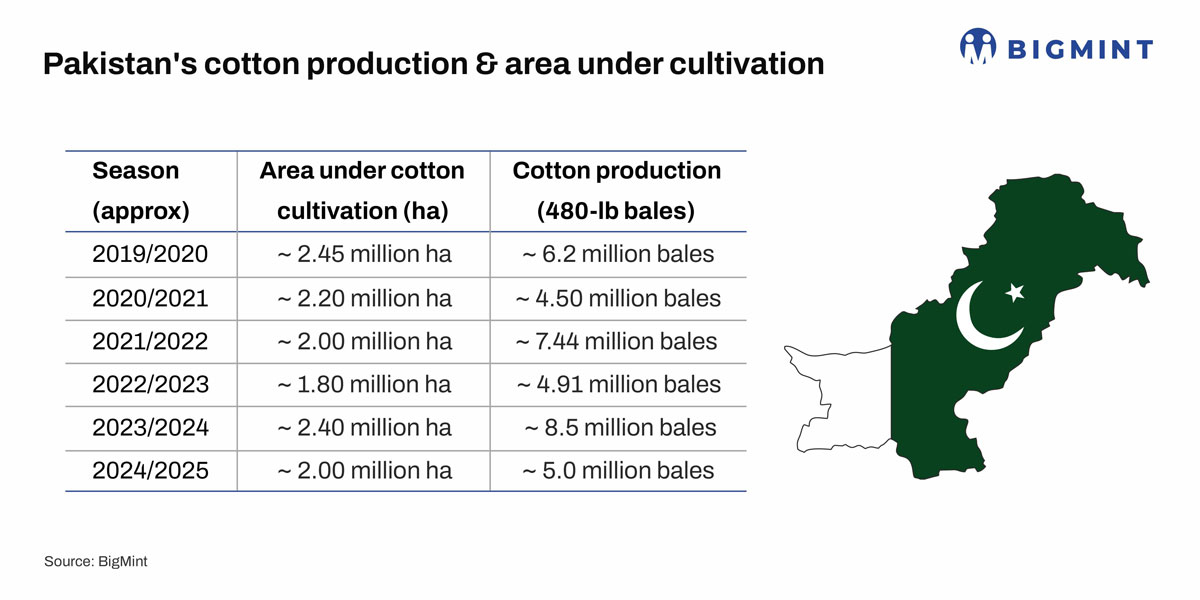

Pakistan’s cotton arrivals reached 5,133,620 bales as of 30 November 2025, falling by 57,105 bales from last year’s 5,190,725 bales — a 1.1% decline. The disparity between provinces is striking. Sindh’s arrivals increased to 2,784,373 bales, up by 53,332 bales from last year, supported by better early-season weather and consistent picking.

But Punjab, which historically accounts for nearly 60% of Pakistan’s output, posted a steep drop of 110,437 bales, or 4.49%, signalling deeper structural deterioration. The unsold stock position further highlights market weakness: 667,257 bales remain unsold this season versus around 640,000 bales at the same time last year, pointing to slower mill buying. Meanwhile, 4,466,363 bales have been sold so far compared with 4,513,478 bales last year — a clear indicator of reduced domestic offtake.

The underlying reasons are well-established and worsening. Farmers continue to move acreage away from cotton because of the absence of a support price, making the crop financially unviable against rice and sugarcane which offer higher and more stable returns.

Climate pressures — erratic rainfall, prolonged heat spells, and water shortages — have cut yields in central and southern Punjab. Pest attacks from whitefly and pink bollworm have intensified, particularly in late-August and September, damaging bolls and raising production costs.

Seed technology remains outdated, with average yields stuck around 550–600 kg lint per hectare, far below India’s 700+ kg and Brazil’s 1,800+ kg. Pakistan currently has 385 operational ginning factories compared with more than 400 just a few years ago, indicating declining raw cotton availability and shrinking industry activity.

Pakistan’s textile sector consumes more than 15 million bales annually, yet domestic production this year is expected to remain close to 7.5–8 million bales. This widening gap forces Pakistan to spend between $2–3 billion annually on cotton imports, depending on international prices. With 509,830 pressed bales and 157,427 unginned bales still lying unsold, liquidity pressures on ginners remain high. Mills have also slowed procurement due to weak textile orders globally, rising power costs, and limited export competitiveness.

Impact on India

For India, Pakistan’s continuing production decline has two clear implications. First, regional cotton supply tightness may keep global prices supported, especially if India’s own arrivals slow after January. Indian spinning millers could face cost pressure, particularly those dependent on higher-grade imported fibre.

Second, this situation creates a strong opportunity for India’s yarn and fabric exporters. As Pakistan imports more cotton and loses textile competitiveness, international buyers increasingly shift orders to India. India has already gained share in markets like China, Bangladesh, and Turkiye, and this trend may accelerate through 2026.

Going ahead, India can benefit from stronger export demand and firmer price sentiment, but only if domestic cotton availability remains steady. Any drop in Indian production or quality could quickly turn this advantage into a raw-material challenge for spinning millers. Improved logistics, better-quality arrivals, and policy clarity on cotton import duties will remain critical factors.

The regional supply imbalance caused by Pakistan’s crisis may support Indian ginners and traders, but spinning millers must prepare for volatility in both procurement and export orders.

Leave a Reply