- Tight availability of high-grade ore persists

- Payment delays restricting smooth trade flow

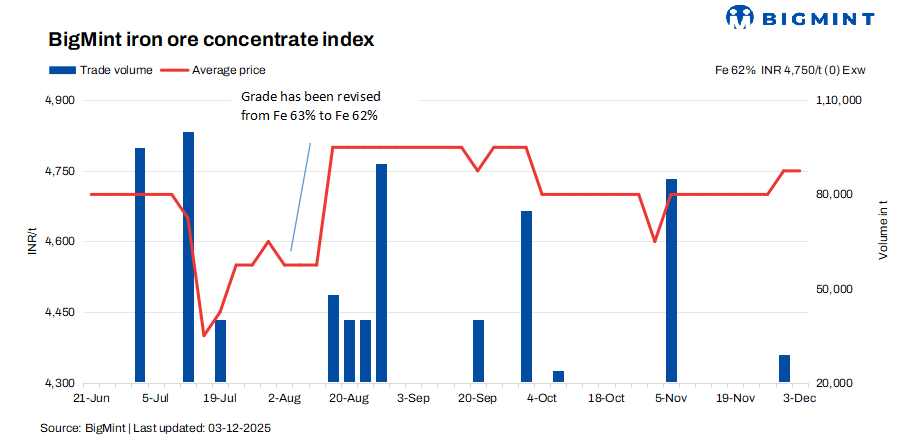

BigMint’s latest bi-weekly assessment for India’s iron ore concentrate (Fe 62%) remained unchanged at INR 4,750/tonne ($53/t) ex-works Jabalpur on 3 December as against 29 November. According to market sources, trading was moderate as sellers busy clearing pending bookings kept fresh offers virtually off the table, thereby tightening overall availability in the market.

Meanwhile, Fe 63% concentrate prices were stable at INR 5,000/t ($58/t) exw. Market sources reported active deals for high-grade concentrate as an acute shortage of premium grades has worsened into an overall regional shortfall. With supplies tightening rapidly, buyers continued to chase high-grade material.

A Jabalpur-based seller observed that “market competition has increased noticeably in recent days. Recent railway restrictions over the past four-five days disrupted wagon availability and slowed unloading operations, although these logistical issues have now been resolved.”

Despite this improvement, payment-related challenges continue to weigh on trade. The seller mentioned that although material is ready for upcoming deals, buyers are delaying payments due to the earlier disruptions in movement.

“With nearly 30% of older commitments still pending, the market is facing a clear demand-supply imbalance. This backlog, combined with heightened competition, is creating uncertainty among both buyers and sellers,” a source mentioned.

A Jabalpur-based buyer informed BigMint that prices remain stable in the region with no significant changes observed over the last few days.

Rationale

- One (1) trade was recorded in this publishing window and was taken into consideration, receiving a 50% weightage.

- Eight (8) offers and indicative prices were heard, and six (6) were taken into consideration as T2 trades, receiving 50% weightage.

Factors influencing prices

- Pellet prices remain firm in Raipur: PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, held firm at INR 9,650/t ($108/t) DAP on 2 December, unchanged from the 28 November assessment. Market activity remained subdued over the past few days, with demand trailing and buying sentiment staying noticeably weak among local steelmakers. Despite suppliers maintaining steady offer levels, no significant deals were finalized, underscoring buyers’ cautious approach amid persisting uncertainty in market fundamentals.

- Odisha iron ore prices edge up w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index stayed unchanged w-o-w at INR 5,600/t ($63/t) ex-mines on 29 November 2025. Prices in the Odisha market remained firm as miners continued to close deals at prevailing offer levels. According to market participants, several leading miners successfully sold substantial bulk volumes through auctions, highlighting resilient demand even as caution persisted in downstream sectors.

Outlook

Iron ore concentrate prices are expected to remain stable in the near term supported by firm pellet prices, healthy auction activity in key producing regions, and persistent tightness in high-grade supplies. While payment delays, logistical constraints, and weak downstream buying sentiment may limit spot trade volumes, restricted fresh offers and pending order backlogs are likely to prevent any major price correction.

Leave a Reply