- IF rebar prices rise w-o-w amid firm sponge iron, billet prices

- BF rebar prices hit 5-year low on weak demand, surplus supply

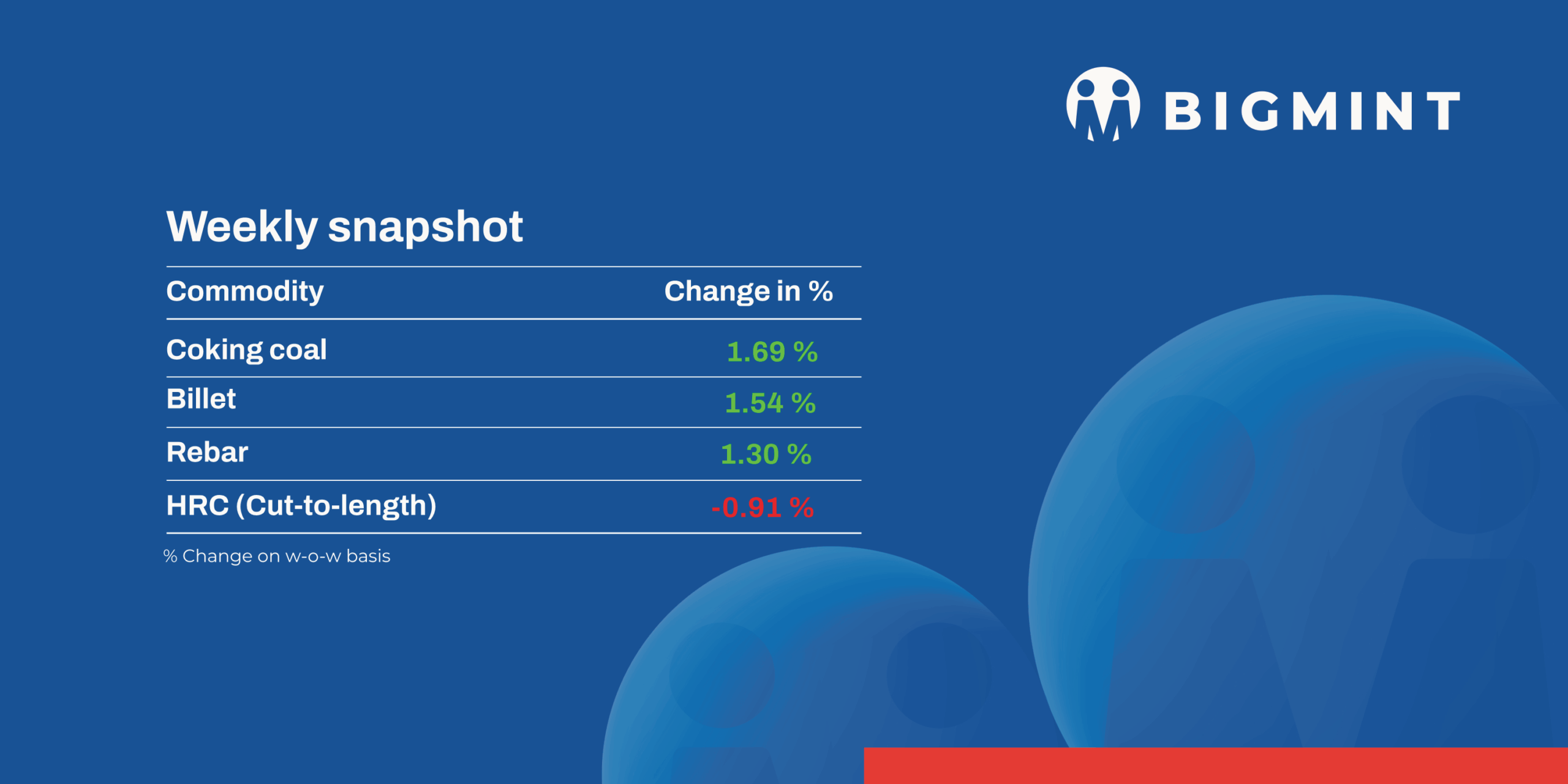

The domestic steel market recorded positive price movements in the week ended 28 November. Semi-finished steel prices edged up by INR 300-700/tonne (t), boosted by steady demand for finished steel products.

Iron ore and pellet

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, fell by INR 50/t ($0.5/t) w-o-w to INR 9,650/t ($108/t) DAP on 28 November 2025. Demand was limited in the last couple of days, with local pellet suppliers concluding deals for around 20,000 t in Raipur at INR 9,400-9,600/t exw. Raipur-based pellet producers kept their offers for 63% (+/-0.5%) material stable at INR 9,500-9,600/t ($107-108/t) exw recently.

- In NMDC’s 85,100 t iron ore auction from Chhattisgarh on 27 Nov’25, 35,800 t was booked. 12,900 t DRCLO (10-40 mm, Fe 67%, base INR 6,300/t) and 4,000 t lumps (10-20 mm, Fe 65.5%, base INR 5,750/t) were sold at 16% premiums. Out of 25,200 t, 10,300 t ROM (10-150 mm, Fe 65.5%) was booked at INR 5,500/t and 8,600 t fines (Fe 64%) at INR 4,790/t. Prices were on FOR basis, including royalty, DMF, & NMEDT.

- In NMDC Kumaraswamy 26 Nov’25 auctions, entire 40,000 t (10-40 mm, Fe 60.69%) of lumps booked at INR 4,285/t. 80,000 t (Fe 58.93-62.97%) of fines sold at INR 3,099-5,133/t.

- BigMints bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices fell by $2.5/tonne (t) w-o-w to $66.5/t FOB east coast on 27 November. Meanwhile, the index stood at $78/t CFR China. BigMint heard approximately 350,000 t of export deals during this publishing period, primarily for December laycan with a couple of iron ore lump cargoes recorded from the west coast.

Coal

- South African thermal coal offers firmed w-o-w on 28 Nov across major Indian ports, although buying remained selective as industries resisted higher offers amid mixed inventories and rising freight. Prices tracked stronger global benchmarks and INR depreciation. Ex-Paradip RB2 increased by INR 150 to 8,550/t, while RB3 stayed at 7,200/t. At Gangavaram, RB2 rose by INR 50 to 8,400/t and RB3 moved to 7,250/t. Ex-Vizag RB2 also gained INR 50 to 8,400/t, with RB3 steady at 7,200/t.

- Domestic coal prices held firm w-o-w on 28 Nov at INR 6,350/t for 5,000 GCV and INR 5,250/t for 4,500 GCV ex-Bilaspur. Demand had begun improving as SECL and ECL scheduled frequent auctions ahead of winter requirements.

- India’s met coke market remained steady w-o-w with marginal regional changes. Eastern BF-grade met coke stayed at INR 31,800/t ex-Jajpur, while western prices edged up to INR 30,200/t ex-Gandhidham. Foundry-grade met coke at Rajkot held firm at INR 36,000/t, supported by stable end-user interest. Market mood stayed cautious as buyers awaited clarity on anti-dumping duties.

- BigMint’s premium hard coking coal (PHCC) index stayed unchanged at $219/t CNF Paradip on 28 November 2025, with persistent bid–offer gaps. Australian offers hovered at $217–220/t CFR India, while bids remained near $210/t amid weak steel sentiment. Recent Chinese purchases continued to support global coking coal offers.

Ferrous scrap

- India’s imported ferrous scrap market remained subdued throughout the week as mills shifted toward cheaper domestic sponge iron, local scrap, and HBI amid weak finished steel sales and uncertainty from the softer US dollar, which rendered earlier import price levels unworkable. Offers remained steady, with HMS 80:20 near $330/t CFR, HMS 90:10 at $340-345/t, shredded around $355/t, and PNS at $360/t, while workable bids stayed noticeably lower.

- Competition from higher Turkish bookings diverted containerised scrap away from India, widening the India-Turkiye price gap and discouraging buying, as exporters increasingly favoured markets such as Turkiye, Pakistan, and Bangladesh.

- In the last seven days, around 14,500 t of imported scrap was booked into India, including about 5,750 t of HMS 80:20 at $315-340/t CFR from the UK and Brazil into Mundra and Nhava Sheva, alongside 2,000 t of shredded at $347-352/t and rest includes busheling bundles, turnings & borings and NTP bundles.

Ferro alloys

- Silico Manganese:Indian silico manganese (60-14) prices dip slightly by INR 500/t ($6/t) w-o-w to INR 69,700-70,600/t ($780-790/t) across Durgapur, Raipur, and Vizag. Slower buying from steel mills, driven by volatility in finished steel prices, kept procurement cautious and lowered trade activity across key markets.

- Ferro Manganese:Indian ferro manganese (HC 70%) prices inched down by INR 100/t ($1/t) w-o-w to INR 72,000/t ($806/t) exw-Durgapur, while prices in Raipur also slip slightly by INR 400/t ($4/t) w-o-w to INR 72,000/t ($806/t)Prices softened as buying interest weakened, with sluggish market activity and cautious procurement weighing on overall sentiment.

- Ferro Silicon:Indian ferro silicon (Si 70%) prices fell slightly by INR 500/t ($6/t) w-o-w to INR 98,000/t ($1,097/t) exw-Guwahati, while Bhutan’s prices increased by INR 700/t ($8/t) to INR 98,500/t ($1,102/t). Limited availability kept offers firm, but buyer caution slowed trading activity. Market participants are now awaiting Bhutan’s December price announcement.

- Ferro Chrome:Indian high-carbon ferro chrome (HC 60%, Si 4%) prices declined by INR 3,500/t ($39/t) w-o-w to INR 111,200/t ($1,245/t) exw-Jajpur amid buyer resistance to higher offers, which slowed market activity.

- Meanwhile, Vedanta-Ferro Alloys Corporation (FACOR) has scheduled an auction for high-carbon ferro chrome (Cr 56% min, 10-150 mm) on 1 Dec’25, with minimum allowed bid quantities set at 25-300 t for both lots.

Semi finished

- India’s semi-finished steel market recorded a moderate increase this week, according to BigMint’s assessment. Domestic billet prices across major regions rose by INR 300-700/t ($3-7/t) w-o-w, with Jalna, Raipur, and Mumbai leading the uptrend, posting gains of INR 500-700/t ($5/t). A significant portion of bookings was directed toward outstation markets, as buyers leveraged favourable interstate price gaps and competitive transportation costs rather than procuring locally.

- In contrast, the sponge iron market remained volatile with only minor adjustments in offers. Key markets from central and eastern regions registered modest increases of INR 100-300/t ($1-3/t) w-o-w, while other regions held firm. Although a slight sentimental improvement influenced these variations, while buying interest remained weak keeping overall spot activity limited throughout the week.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, auctioned 5,000 t of steel-grade pig iron on 28 Nov’25, with the entire quantity booked at an average price of INR 31,100/t (by road). However, management approval is still pending. Bids improved by INR 250/t compared to the previous auction on 07 Nov, which saw an average price of INR 30,850/t (by road).

- Indian DRI (Direct Reduced Iron) offers softened slightly by $1-2/t, settling at $308/t CPT Raxaul and $320/t CPT Benapole. The marginal decline was due to subdued demand from key importing countries, with buyers showing limited appetite for spot procurement.

Finished Long Steel

- IF-rebar:India’s Induction Furnace (IF) route rebar prices moved upward week-on-week, supported by firm sponge iron and billet prices. Early in the week, sellers saw active bookings as buyers procured significant quantities. In the past couple of days, with the increase in prices, buying activity has slowed down, but with adequate volumes already sold, suppliers are not interested in rebating the prices. Supporting with the above factors Inventory levels have also come down to 10–12 days from the earlier 15 days, and prices are expected to remain range-bound with a positive bias in the near term.

- On a weekly basis, prices in rebar steel witnessed increased in the range of INR 100-700/t across the regions except in Chennai where price drop of INR 200/t noticed as per BigMint assessment shows.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 38,700-39,100/t exw Raipur, INR 42,500-43,100/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 41,100-41,500/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 40,000-40,500/t ex Raipur.

- BF-rebar:Indian trade-level BF-rebar prices have hit a five-year low in end-November 2025, as per BigMint data. Prices fell w-o-w due to muted trading activity across key markets, with sellers offering discounts to clear inventories. Surplus material in the trade channel has intensified the pressure on prices, market sources indicated.

- Trade-level BF rebar prices dropped by INR 300/t ($3/t) w-o-w to INR 46,300/t ($517/t) exy-Mumbai, as per BigMint’s benchmark assessment on 28 November. Prices are exclusive of GST at 18%.

- In the projects segment, prices hovered between INR 45,000-46,000/t ($503-514/t) FOR Mumbai. Buyers were cautious in placing orders amid market uncertainty.

Flat Steel

- Trade-level prices of hot-rolled coils (HRCs) in India showed down-trend in the week beginning 24 Nov. HRC prices stood at between INR 46,000-48,100/tonne (t) ($516-539/t) across regions. Cold-rolled coil (CRC) prices ranged between INR 51,300-56,000/t ($575-628/t).

- The domestic HRC market sentiments remained soft as market demand remains moderate, but oversupply and high inventory levels are weighing on sentiment, a participant informed Bigmint.

- India’s bulk imports of HRCs touched 197,069 t as of 22 November 2025, based on vessel line-up data. Around 115,427 t of additional cargoes are expected by early December.

- India’s bulk exports of HRCs touched 162,088 t as of 22 November 2025, and around 159,015 t of additional cargo are in transit.

- BigMint’s Indian hot-rolled coil (HRC, S275) export index for the European Union (EU) remained stable w-o-w at $520/t FOB main port. No fresh offers were heard, as India’s export quota to the EU for the October-December quarter has been exhausted.

- Furthermore, the Indian HRC (SAE 1006) export index monitoring the Middle East market remained unchanged due to stable domestic demand in the region ahead of approaching National Day holidays.

Leave a Reply