- Stable construction activity limits any upward rebar movement

- Export bids are weak, keeping UAE scrap under mild pressure

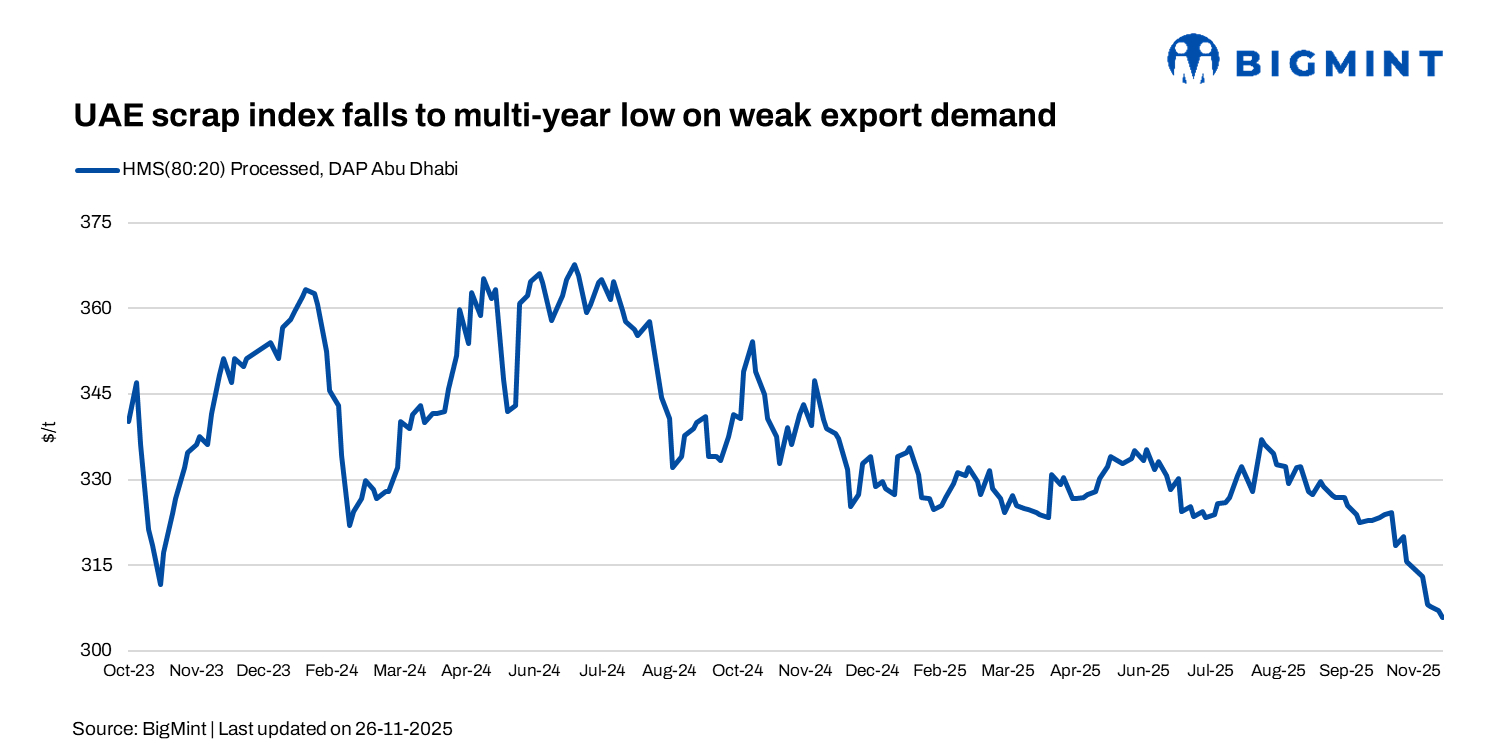

UAE domestic processed HMS prices fell sharply by AED 67/t ($18/t) m-o-m to AED 1,124/t ($306/t) on 26 Nov’25, mirroring a w-o-w drop of AED 7/t ($2/t) from last Wednesday (19 Nov’25) amid weak export activity and softer buying interest.

Notably, the current HMS 80:20 processed price is now hovering at its lowest level since assessments began in October 2023.

Shredded scrap traded at AED 1,150-1,170/t ($313-319/t), while PNS hovered at AED 1,140-1,160/t ($310-316/t). Traders remain cautious, limiting purchases as they await clearer signals from mills, keeping overall sentiment subdued.

Local scrap prices remain mixed from different yards:

- HMS (unprocessed): AED 1,025-1,075/t ($279-293/t)

- HMS (processed): AED 1,075-1,125/t ($293-306/t)

- Shredded: AED 1,160-1,175/t ($316-320/t)

- Fabrication scrap: AED 1,075-1,100/t ($293-299/t)

- End-cut: AED 1,175-1,190/t ($320-324/t)

Market feedback shows in the export market, UAE shredded is bid at $350-355/t CFR, with offers hovering around $360-362/t CFR Qasim.

Lastly, a Pakistan-based mill booked 2000 t of shredded from the UAE at $360/t CFR Qasim.

Emirates Steel maintains rebar pricing for December sales

Emirates Steel Industries kept 10-32 mm rebar prices unchanged at AED 2,648/t ($721/t) on 90-day LC terms, with the UAE market staying steady and unlikely to absorb higher levels amid moderate construction activity.

EMSTEEL secures natural gas supply with ADNOC gas

EMSTEEL secures natural gas supply with ADNOC gas

EMSTEEL strengthened its strategic position by signing a major 20-year natural gas supply agreement with ADNOC Gas worth $3.5–4.2 billion, effective January 1, 2027. The deal secures a long-term energy supply to support operations and future expansion.

EMSTEEL operates three gas-based DRI plants (4.2 million tpy), 3.6 million tpy of EAF capacity, and rolling mills including 2 million tpy of rebar, a 1 million tpy section mill, and a 500,000 tpy wire rod mill.

UAE billet buying rises amid lower-than-expected prices

Meanwhile, billet trade showed activity–UAE buyers booked around 50,000 t at $455–460/t CFR, still below supplier expectations and pressured by cheaper Asian offers. Strong domestic rebar demand continues to cap semis’ profitability, limiting mills’ appetite for billet exports.

Adding another layer of competition, Saudi mills have formally entered the UAE market after Al Ittefaq Steel, Hadeed, and National Steel secured ECAS approval. Early signs show 20,000-25,000 t of Saudi rebar already sold, with more shipments expected. Saudi rebar is estimated at AED 2,280-2,330/t delivered, significantly below Emirates Steel’s official prices, raising concerns about price pressure even if cut-and-bend preferences may cushion the impact.

Short-term outlook

The UAE market is set to remain steady yet cautious. Scrap prices may face mild downward pressure as weak export activity and selective buying keep sentiment subdued. Rebar demand stays stable, but insufficient for mills to push for higher prices.

Leave a Reply