- Liquidity constraints dampen market sentiment

- Sellers clearly under pressure amid soft demand

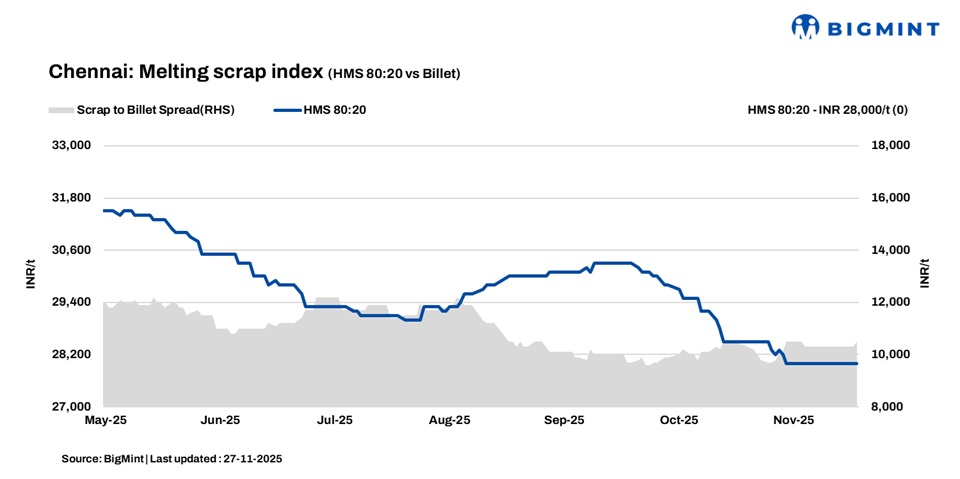

HMS (80:20) scrap prices in Chennai remained unchanged at INR 28,000/t, with stability observed on both d-o-d and w-o-w comparisons, according to BigMint’s latest assessment. Similarly billet and rebar prices held firm w-o-w and d-o-d, assessed at INR 38,500/t and INR 43,000/t respectively. The market continues to face pressure from liquidity constraints, with billet and rebar demand hovering at average levels, reflecting a cautious buying trend across regions.

Imported, domestic market trends

Imported shredded scrap offers stood at $345-350/t CFR Chennai, while buyers kept bids lower at $340-342/t. HMS (80:20) was quoted at $320-325/t, with bids around $315-320/t.

UK-origin HMS was heard at $320-325/t (2-3% impurities) CFR Chennai and $320-325/t (1-2% impurities) CFR Chennai. Hong Kong PNS at $354-355/t CFR Chennai, and Malaysian busheling at $360-362/t CFR Chennai.

The key concern in the trade right now is whether Indian buyers can realistically secure UK HMS at these levels when Turkiye is already paying $360-365/t for bulk. Suppliers are clearly feeling margin pressure, and overall sentiment remains weak with dull finished steel demand and cautious buying.

In the Chennai market, domestic HMS (80:20) scrap is trading at INR 28,000-28,500/t for spot transactions with immediate payment. Deals involving extended credit terms are fetching slightly higher prices in the range of INR 28,500-29,000/t. Market participants noted that most offers and concluded trades are concentrated within the INR 28,000-29,000/t band, reflecting the prevailing liquidity conditions and the growing influence of credit-based pricing in scrap trade.

Buyer-supplier sentiments

According to market sources, major sponge iron manufacturers are prioritising captive consumption over selling material in the merchant market. Supplies from neighbouring states have also remained weak amid reported logistical challenges, particularly from regions such as Bellary.

Billet demand continues to be subdued, with some market participants undertaking maintenance shutdowns. Finished steel demand is also muted, as no major project activity is expected in the state ahead of the upcoming assembly elections next year. Current rebar offers stand at INR 41,500-42,000/t for project buyers and INR 43,000-43,500/t in the retail market.

According to a leading scrap supplier, HMS (80:20) scrap traded in the range of INR 28,000-29,000/t, with realisations varying primarily based on payment terms. Ongoing liquidity constraints continue to dampen market sentiment, resulting in moderate trade volumes. With the monsoon season underway, buyers remain cautious in placing fresh bookings, particularly for finished steel. Market sentiment remains weak as major mills are carrying elevated finished steel inventories of approximately 20-25 days, further contributing to the subdued market sentiment.

Regional comparison

In the western India-based Jalna market, billet prices rose by INR 700/t day-on-day to INR 38,500/t DAP, while rebar prices gained INR 100/t at INR 42,800/t, and HMS (80:20) scrap prices climbed INR 100/t to INR 29,200/t DAP. Market participants noted improved finished steel trading activity in recent sessions, with mills securing adequate scrap inflows to support operations. Despite the recent uptick in semis and finished steel prices, scrap rates are likely to stabilize in coming days, as mills prioritize preserving conversion margins that had narrowed previously.

Outlook

Market participants expect domestic scrap prices to remain stable in the coming days, supported by firm supplier offers and relatively higher imported scrap and sponge iron prices. Any near-term price movement is likely to be limited to within INR 200-500/t, keeping overall market sentiment steady but range-bound.

Leave a Reply