- High steel inventories cap near-term recovery potential

- Election uncertainty keeps buyers cautious and inactive

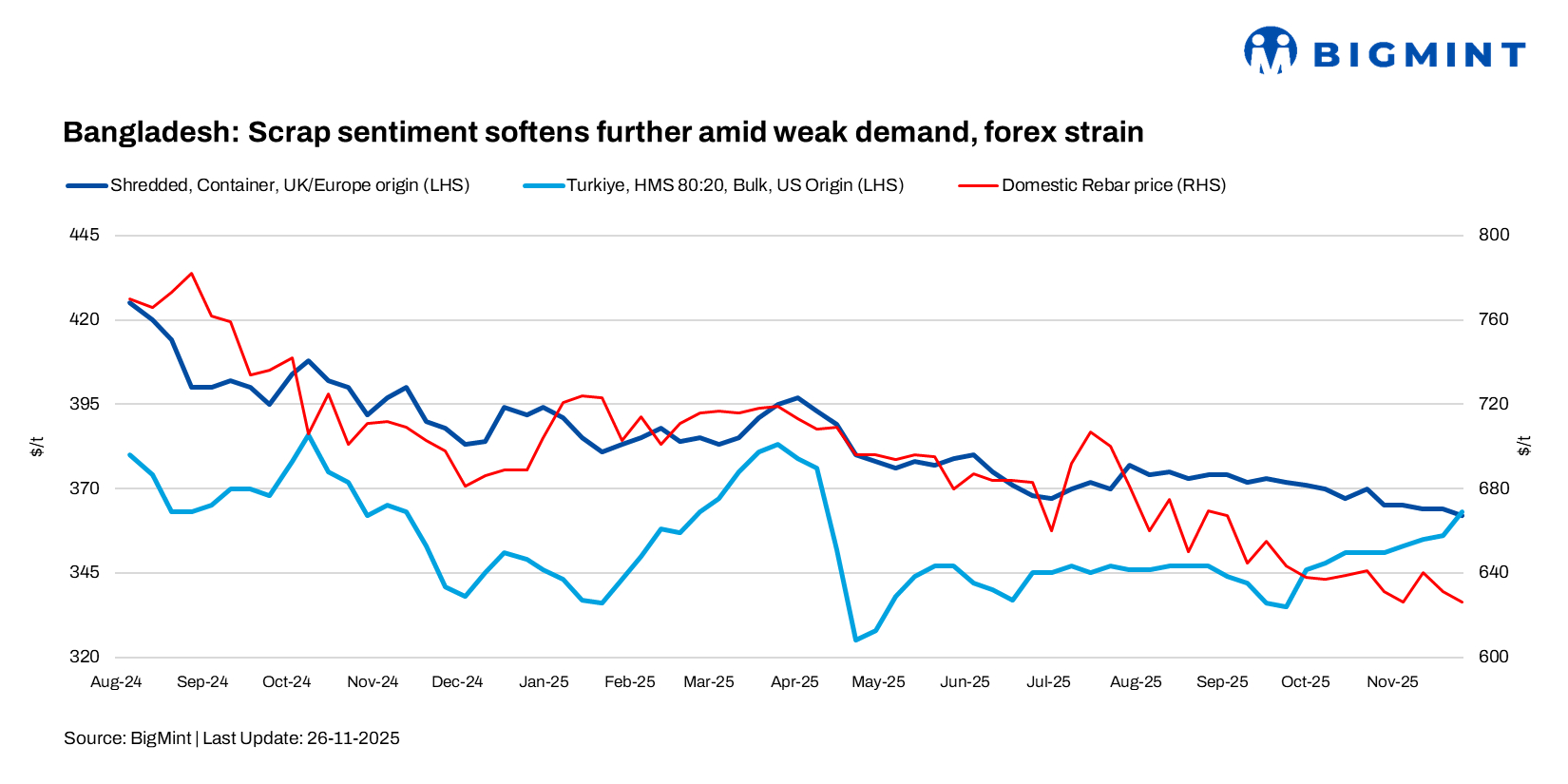

Bangladesh’s imported scrap prices and sentiment remained soft during the week ending on 26 Nov, with mills weighed down by weak downstream demand and tight liquidity. Buying remained cautious, and election-related uncertainty further slowed activity, keeping most buyers on the sidelines unless absolutely necessary.

BigMint’s weekly assessments

- European-origin HMS (80:20) held steady w-o-w at $341/t.

- European-origin containerised shredded inched down by $2/t w-o-w to $364/t.

- Japanese-origin H2 bulk stayed stable at $341/t.

- US-origin HMS (80:20) bulk inched up $2/t w-o-w to $353/t.

Bulk HMS 80:20 from the US was last heard between $355-360/t CFR, but Bangladesh’s bids stayed between $340-345/t CFR, keeping bulk trades sidelined. Sentiment remains weak as mills hold back amid election uncertainty and liquidity strain.

Indications for bulk cargoes into Chattogram have now risen above $365/t CFR, though these remain notional given the lack of buying interest. Japanese H2 was priced between $340-345/t CFR, but demand is still negligible.

Deal activity was limited but steady through the week. A 9,000-t PNS cargo from Singapore and Malaysia was concluded at $367/t CFR Chattogram, while another supplier sold the same grade at $363/t.

Other recent deals:

- 5,000 t PNS from Malaysia/Singapore booked at $365/t CFR Chattogram

- 1,000 t PNS form Australia booked at $371/t CFR

- 500 t shredded from Australia sold at $360/t CFR

Ship-breaking market

Chattogram received six vessels totalling 63,479 LDT this week, though overall yard activity stayed softer than expected. Bangladesh continued to lead on pricing, but workable candidates were limited, with only a few tankers and LNG units entering the market and overall vessel supply falling short.

Steel plate prices hovered around $526/t as the BDT (Taka) weakened. Rising pre-election uncertainty, cheaper imported steel, and high unsold inventories kept demand subdued, weighing on sentiment despite the gradual increase in HKC-approved yards.

Outlook

The near-term outlook stays weak, with scrap demand likely stuck in a narrow range until domestic steel consumption picks up and Forex pressures ease. Winter may tighten global supply slightly, offering some support, but high steel inventories and ongoing election uncertainty will keep any upside limited.

Leave a Reply