- Tight refined tin supply supports market stability

- Myanmar mine supply recovery remains slow

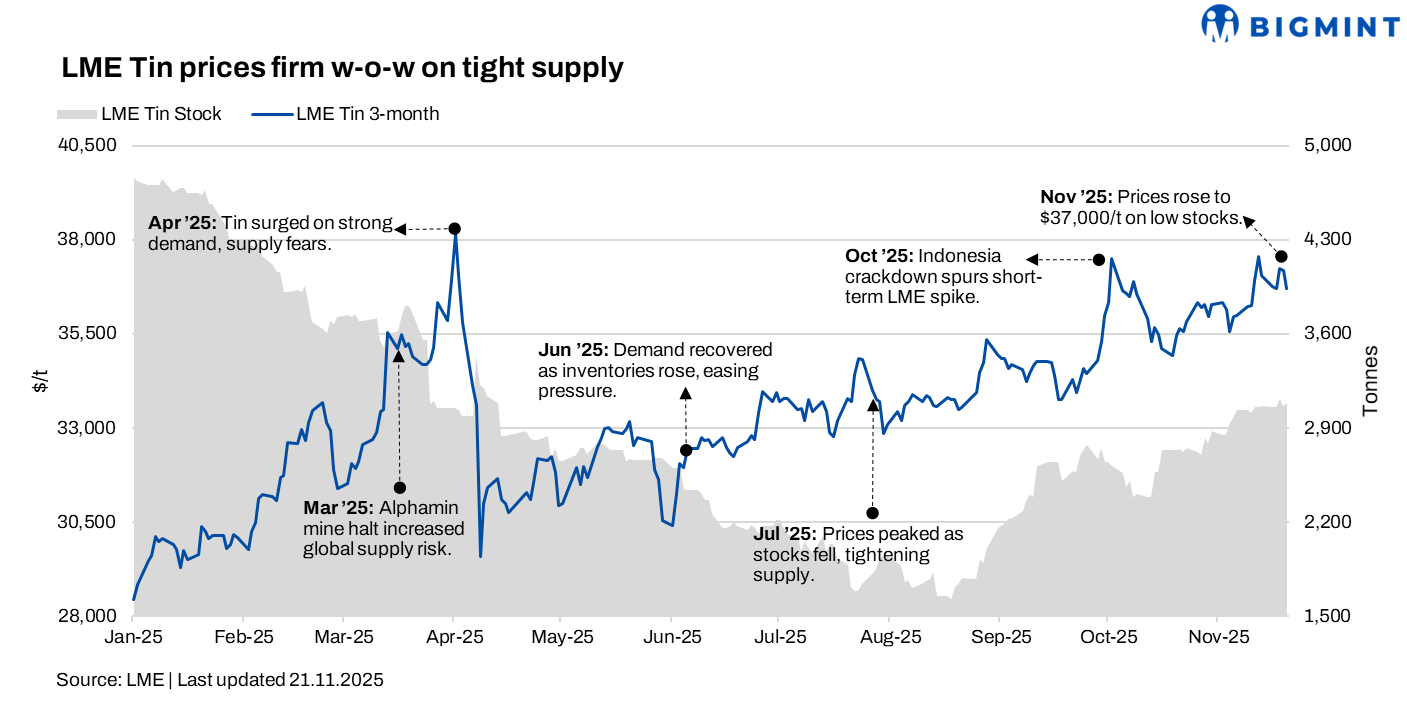

LME tin prices stood firm during week 47 of CY’25 (17-22 November). Tin prices remained firm this week despite broad pressure across global base metals, supported by resilient supply fundamentals and tightness in refined tin availability. While macro uncertainty driven by mixed US labour data and soft risk sentiment limited upside, sustained mine-side challenges and uneven import flows helped keep tin prices relatively stable.

Pricing, inventory trends

LME tin prices averaged $36,923/tonne (t) in week 47, marking an $117/t or 0.3% rise w-o-w from week 46 (10-14 November). The week began with prices at $36,775/t, which inched up to around $37,230/t mid-week and closed at $36,710/t.

Meanwhile, tin inventories at LME-registered warehouses rose to 3,075 t from 3,045 t in week 46.

What impacted prices?

Tin prices held firm this week even as global macro sentiment turned cautious. The latest US non-farm payrolls data showed an increase of 119,000–well above expectations–yet the unemployment rate unexpectedly rose to 4.4%, the highest since October 2021. This conflicting data deepened market divides over the Federal Reserve’s policy path, briefly lifting the US dollar index and exerting broad pressure on base metals. US equities closed lower, further cooling risk appetite and prompting profit-taking among tin bulls.

In China, signs of resilience in the broader economic recovery emerged, but the transmission of macro support into the industrial sector remained weak, keeping investors conservative. Spot trading was sluggish, with downstream buyers limiting activity to small, just-in-time procurement.

Fresh data from the World Bureau of Metal Statistics (WBMS) offered mixed cues. Global refined tin output reached 32,500 t in September 2025, while consumption stood at 27,600 t, resulting in a monthly surplus of 4,900 t. However, January-September data showed a cumulative production deficit of 9,200 t, reinforcing concerns around structural tightness in the refined market.

Mine-side dynamics also supported tin’s relative firmness. Global tin ore production hit 27,200 t in September and reached 223,100 t between January and September. China’s tin ore and concentrate imports in October rose 33.5% m-o-m to 11,632 t but remained 22.4% lower y-o-y, highlighting ongoing supply sensitivity. Imports from the DRC surged 124% m-o-m, while shipments from Myanmar continued to recover only slowly, falling 24.6% m-o-m and 61.6% y-o-y.

Refined tin imports into China were notably weaker. October volumes fell 58.6% m-o-m and 82.8% y-o-y to just 526 t. Bolivia and Peru remained the top suppliers, though both recorded steep m-o-m declines, indicating restricted refined tin availability in the international market.

Outlook

Tin prices are expected to remain rangebound in the near term as cautious macro sentiment and soft risk appetite cap further upside. While refined tin supply remains structurally tight, uneven mine recovery–particularly from Myanmar–continues to inject uncertainty into the market. Traders will watch U.S. economic signals and China’s downstream demand trends closely, as these factors will shape tin’s next price direction.

Leave a Reply