- Grid stability masks deeper industrial demand slump

- Economic reliance on govt spending signals structural fragility

On the surface, India’s power grid is a picture of robust health. Over the past month, it has navigated the seasonal transition from monsoon to winter with remarkable stability. Demand has softened predictably, the grid frequency has held steady, and a comfortable buffer of 52 million tonnes of coal enough for 17 days sits at power plants recorded as of 15th November 2025. Yet, this placid surface is hiding a turbulent undercurrent: what looks like efficient management is also a symptom of a deepening demand depression that raises urgent questions about the nation’s industrial vitality.

The comforting veneer of seasonal stability

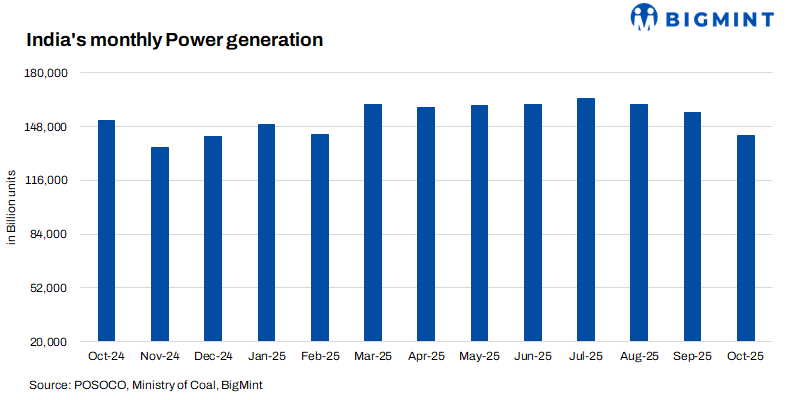

The data from the National Load Despatch Centre (NLDC) tells a story of seamless seasonal adjustment. From a late-October peak of 189,660 MW, demand has eased by mid-November, a typical pre-winter softening. The grid has remained impeccably balanced, with coal’s share in the generation mix actually rising from 73% to 76% as hydroelectric output plummeted by 36%.

“Operationally, the grid has never been more resilient,” says a senior grid official. “We have managed the hydro decline and seasonal demand shift without a hint of shortage. The system is performing as designed.”

But this operational success masks a more disquieting economic reality. The very comfort of the situation – the ample coal stocks, the easing demand – is built on a foundation of weaker-than-expected industrial electricity consumption.

The “Single-engine” economy: A house built on Government spending

The core of the issue lies in the structure of demand. A source from a major cement company revealed a startling statistic: 70-75% of all cement sales are currently delivered to government-funded infrastructure projects. This is not an isolated data point but a proxy for the entire core sector.

This reliance on public spending is reflected starkly in the power data. Despite government projections of 277 GW peak demand, actual usage has plateaued at 240-245 GW. More tellingly, total power output in October fell 11% year-on-year, with coal-fired generation down a dramatic 14%.

“This isn’t just a seasonal adjustment; it’s a demand collapse,” argues Dr. Rajeev Sharma, an independent economist. “The prolonged monsoon provided a convenient excuse, but it primarily exposed the sluggish industrial burn. Private investment and household consumption are simply not firing. State governments are financially strapped, and the private real estate market is fundamentally weak.”

This creates a vulnerable economic model. The health of the coal, cement, and steel industries is tethered directly to the continuity and scale of the central government’s capital expenditure. Any pullback or delay in this spending would immediately expose the fragility of the underlying industrial demand.

A tale of two hemispheres: India’s slump vs. Global rebound

India’s power slump stands in stark contrast to the energy narratives unfolding in other major economies, highlighting its outlier status.

- China: While India’s power generation contracted, China is forecasting a 10% year-on-year rise in Q4 power generation, with coal-fired output expected to be 8% higher.

- Europe: Defying its own green transition narrative, Europe is witnessing a quiet coal resurgence. In Poland, coal-fired generation surged to 6 TWh in October, up 8% year-on-year, its highest level since March. Germany is also seeing increased coal burn.

“The contrast is telling,” says a Singapore-based commodities analyst. “In Europe, coal is being used to ensure energy security amid volatile gas prices. In China, it’s fueling a rebounding industrial engine. In India, it’s piling up at power plants because the industrial demand just isn’t there. This isn’t a global coal story; it’s a story of specific Indian economic headwinds.”

Outlook: A precarious balance

The outlook is one of precarious balance. The Indian power grid is stable, but it is a stability born of underutilization, not vibrant growth. The comfortable coal stockpiles are a symptom of weak demand, not robust planning.

Corporate strategy is already adapting to this “single-engine” reality. Major cement and steel players are publicly focusing on “EBITDA margins rather than volume growth,” and the industry anticipates a wave of acquisitions over costly greenfield projects. They are betting on consolidation in a low-growth, government-driven market.

For now, the lights will stay on. The grid is stable, and coal remains the dependable bedrock. But the silence on the grid is growing louder, and it speaks not of efficiency, but of an economy waiting for a second engine to ignite.

Leave a Reply