- India’s domestic met coke prices remain range-bound

- Weak steel market sentiment causes bid-offer disparities

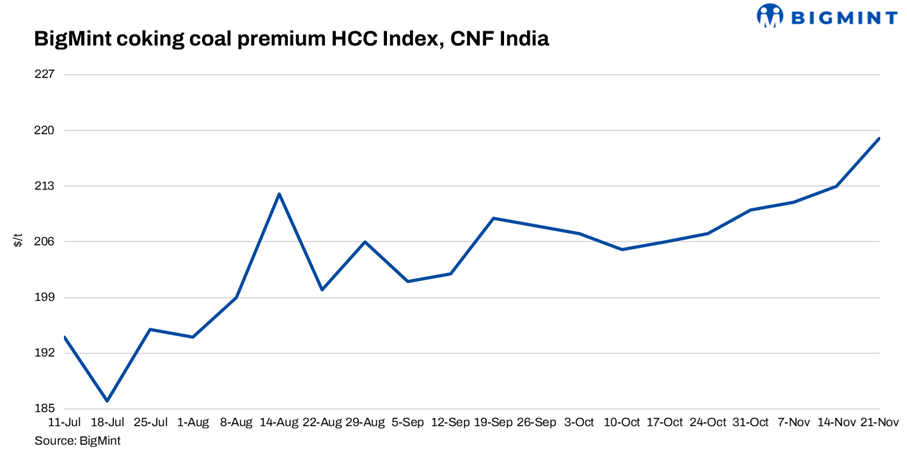

BigMint’s premium hard coking coal (PHCC) index was assessed at $219/tonne (t) CNF Paradip, India, on 21 November 2025, up by $6/t against the previous assessment on 14* November 2025.

An Indian steel mill mentioned that they were in the market for booking cargo. However, they are waiting to receive firm offers.

Meanwhile, bid-offer disparities were observed, owing to weaker steel market sentiments.

Globally, coking coal prices strengthened amid recent deals concluded for China, which has pushed up overall offers, sources said.

BigMint has consolidated its Prime Hard Coking Coal (PHCC) CFR India Index to include material of all origins, including US, Canada, Mozambique, Australia — normalised for quality and freight. With India steadily reducing its reliance on Australian PHCC and increasing imports from alternative sources, this update ensures the index accurately reflects evolving market dynamics and trade flows.

Factors impacting imported coking coal prices

1. India’s domestic met coke prices remain range-bound: The Indian metallurgical coke (met coke) market witnessed mixed trends in the week ending 20 November 2025, with stable pricing in the west and mild w-o-w gains in the east. Demand was healthy, particularly in eastern markets. In eastern India, BF-grade (25-90 mm) met coke was assessed at INR 31,800/t ex-Jajpur, marking an INR 300/t increase w-o-w. Meanwhile, prices in western India remained steady at INR 30,000/t ex-Gandhidham, indicating a balanced supply-demand scenario.

Foundry-grade met coke prices also reflected positive momentum, rising INR 300/t w-o-w to INR 36,000/t ex-Rajkot, supported by increasing demand from end-users.

2. China’s met coke market holds steady as optimism softens: China’s met coke market remained steady this week after recent price hikes, supported by firm coking coal costs and cautious steel output. Mills largely operated near breakeven, focusing on controlled procurement and stable furnace operations, while suppliers noted limited room for near-term upside due to restrained downstream steel demand.

3. India’s BF-rebar trade prices drop by INR 700/t ($8/t) w-o-w amid subdued demand: India’s trade-level blast furnace (BF) rebar prices fell w-o-w across major markets on 21 November 2025 amid subdued domestic demand. Mills offered price support or slashed list prices due to weak market activity. Trade-level BF rebar prices dropped by INR 700/t ($8/t) w-o-w to INR 46,600/t ($525/t) exy-Mumbai, as per BigMint’s benchmark assessment on 21 November 2025. Prices are exclusive of GST at 18%.

4. Indian HRC prices show mixed trends: Trade-level prices of hot-rolled coils (HRCs) in India showed mixed trends in the week. Prices declined in some markets, while other regions witnessed range-bound trends. HRC prices stood at INR 46,400-48,000/t across regions.

*Note: Date has been corrected

Leave a Reply