- Portside Indonesian coal prices remain steady amid ample stocks

- US pet coke rally fades quickly as Indian buyers resist higher offers

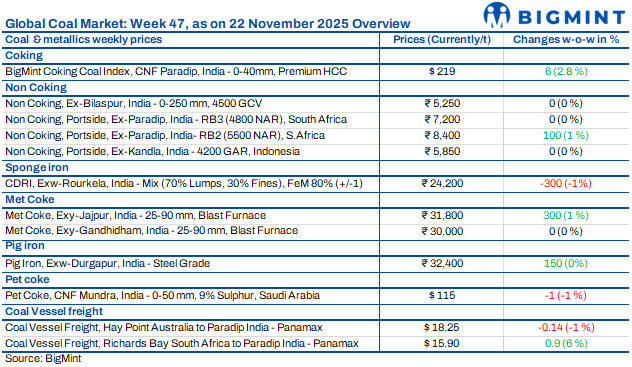

The Indian coal market reflected steady yet cautious sentiment over 17-22 November, shaped by softer buying interest and tighter supply signals across key global export hubs. Traders remained selective, keeping procurement muted despite firmer global indications. Freight movements showed mixed direction, while sentiment across thermal and metallurgical segments remained balanced. Overall, the market maintained a stable tone with limited upside, awaiting clearer demand traction from power, steel, and sponge iron sectors.

Portside Indonesian thermal coal prices hold steady amid soft Indian buying

Portside Indonesian coal prices in India were mostly unchanged w-o-w, supported by firm seaborne benchmarks but restricted by weak local procurement. BigMint kept 5000 GAR at INR 7,200/t in Kandla and INR 7,100/t in Vizag, while 4200 GAR remained at INR 5,850/t and INR 5,750/t. The 3400 GAR grade inched up to INR 4,600/t at Navlakhi. Stocks at power plants rose to 52.89 mnt, ensuring comfortable coverage. Seaborne prices lifted slightly due to rainfall in Kalimantan, but domestic portside values stayed range-bound due to adequate inventories and cautious demand.

Portside South African thermal coal prices firm up on tight supply, stronger Asia demand

South African thermal coal prices at Indian ports remained firm w-o-w, with RB2 rising by INR 100/t to INR 8,400/t ex-Paradip while remaining stable at INR 8,350/t in Vizag and INR 8,400/t in Gangavaram. RB3 stayed flat across the east coast. FOB offers for 5500 NAR held at $76-77/t as tight supply and bulk buying from South Korea and Japan lifted the market. Freights increased to $15.5-16/t. Sponge iron sentiment supported demand, with BigMint’s C-DRI index at INR 24,200/t. South African 4800 and 5500 NAR cargoes were sold out for December, with even $60-61/t FOB bids failing to secure tonnage. Limited availability and firm Asian demand were expected to keep offers elevated through early 2026.

Domestic coal prices hold steady; 98% of offered volumes booked at SECL auction

Domestic coal prices remained stable w-o-w, with 5,000 GCV at INR 6,350/t and 4,500 GCV at INR 5,250/t ex-Bilaspur. In the latest SECL auction, 98% of the 1.078 mnt offered was booked, reflecting strong participation as traders continued operating on low inventories. Auction-based offer changes are expected once deliveries begin. SECL has started releasing larger quantities ahead of winter demand, supporting steady market sentiment despite muted industrial offtake.

Portside US thermal coal traders struggle as demand collapses

US thermal coal traders at Kandla and Tuna remained under acute financial pressure as demand collapsed and inventories remained excessively high. Pre-GST stockpiling created a sharp vacuum in offtake, while winter halted brick-kiln operations and pushed restocking expectations to late February. The cement sector’s shift toward cheaper Indonesian coal removed a crucial demand outlet. Nearly 600,000 t of US NAPP coal is sitting at ports, with daily dispatches barely 4,000 t. Older stocks were offered near INR 10,100/t, with fresh cargoes at INR 10,300-10,400/t, forcing distressed sales as traders struggled to meet letter of credit (LC) obligations.

India’s met coke prices stay range-bound as coking coal sentiment turns bullish

India’s met coke market showed mixed movement, with eastern prices edging up while western levels stayed steady. BF-grade met coke stood at INR 31,800/t ex-Jajpur, up INR 300/t w-o-w, whereas Gandhidham remained stable at INR 30,000/t. Foundry-grade met coke firmed up to INR 36,000/t ex-Rajkot. Market sentiment in the east stayed optimistic, supported by DGTR’s preliminary findings confirming dumping of LAM coke from six countries. Coking coal sentiment turned bullish as domestic met coke makers expected future duties to lift demand for imported coal.

Imported pet coke prices ease as US rally fails to hold

Imported pet coke prices in India slipped w-o-w, with BigMint assessing US-origin material at $117-118/t CFR and Saudi-origin at $115-116/t CFR. A brief $10-18/t surge in US prices — driven by a short burst of Chinese buying at $125-132/t CFR — proved unsustainable as Indian cement buyers refused higher levels. Most large consumers have fuel secured until January-March 2026, giving them little incentive to chase costly cargoes. With Indian bids capped near $109-113/t CFR, the bid-offer gap widened, cooling the rally. Market sentiment leaned softer, as strategic stocking and coal-pet coke flexibility continued to limit upside for US high-sulphur material.

India’s coal freight market show mixed trends across key routes

India’s dry bulk coal freight market showed a split pattern last week, with Pacific rates easing while Atlantic levels held firm. Panamax freights on the Australia-India route softened to $18.25/dmt as Indian buyers showed minimal interest. South Africa-India freights rose slightly to $15.9/dmt due to tight tonnage and stronger export offers. Supramax rates from Indonesia dipped to $14.04/dmt amid thin inquiries. Lower bunker costs offered slight relief, while vessel supply stayed comfortable across basins. With Indian demand still inconsistent, freight sentiment remained steady to slightly soft despite firmer global cues.

Leave a Reply