- Raw material prices increase by INR 100-200/t

- Semis, finished steel prices rise INR 200-400/t

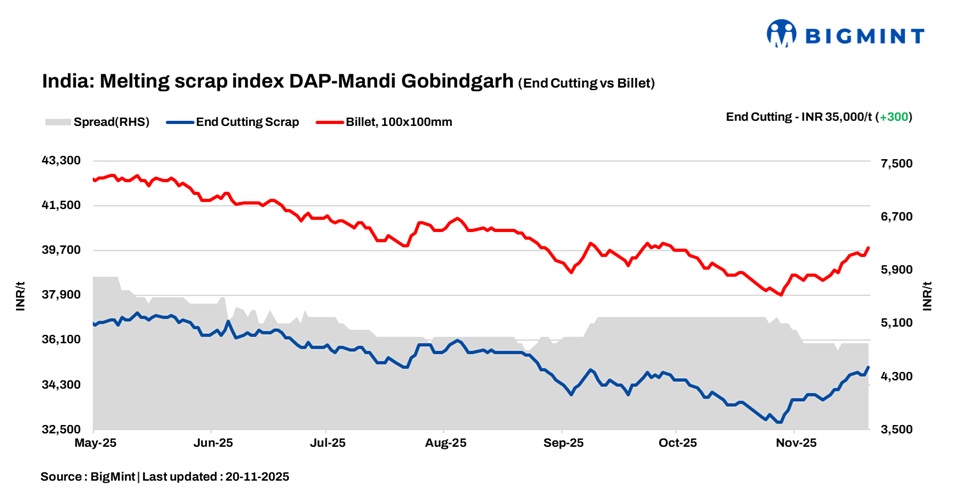

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, increased by INR 300/tonne (t) d-o-d to INR 35,000/t DAP on 20 November 2025.

The key secondary steel hub in north India has seen an improvement in scrap demand driven by the major mills procuring at a healthy pace. However, the region faces scrap shortage due to slow arrivals caused by tight GST inspections and delayed payments from mills to suppliers. Suppliers prefer dealing with large mills that pay promptly.

Demand for semi-finished and finished steel has also increased supported by seller inquiries, though overall sales remain moderate amid liquidity crunch. According to mill owners in Mandi and Ludhiana, the near-term outlook is cautiously positive or range-bound. Moderate demand persists from private infrastructure projects, the auto sector, and agricultural product manufacturers, while government infrastructure projects in Punjab remain slow.

Raw material

Prices of sponge iron (CDRI) in Mandi Gobindgarh rose by INR 200/t d-o-d to INR 29,200/t DAP. On the other hand, steel grade pig iron prices in Ludhiana moved up by INR 100/t to INR 35,200/t DAP.

Steel market

Semi-finished steel (ingot) prices in Mandi Gobindgarh surged by INR 300/t d-o-d to INR 39,800/t DAP. Across major production hubs, ingot prices saw upticks ranging from INR 100 to INR 400/t during today’s trading.

Rebar (Fe500) prices in Mandi rose by INR 400/t d-o-d to INR 44,400/t ex-works, while HR strip (patra) prices increased by INR 200/t to INR 41,200/t ex-works. Despite rising steel-making costs and heavy credit liability posing challenges for mills , near-term demand appears positive with moderate demand coming from neighbouring states.

Overview of Durgapur market

In eastern India’s Durgapur, HMS (80:20) scrap prices declined by INR 100/t to INR 30,700/t. Billet prices inched up by INR 200/t to INR 36,500/t, while rebar offers rose by INR 400/t to INR 38,900/t. According to market sources, finished steel prices strengthened in today’s trading session, although buying activity remained moderate. Prices are expected to stay range-bound in the coming days, with a possibility of slight improvement if demand sustains.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 4,600-4,900/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $318/t, approximately INR 30,410/t (inclusive of freight). HMS (80:20) in Mumbai remained stable d-o-d at INR 29,600/t DAP. Indicative prices of shredded from Europe stood at $348/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 12,050/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply