- Auction bids, spot prices rise in early Nov’25

- Persistent supply glut may limit price gains

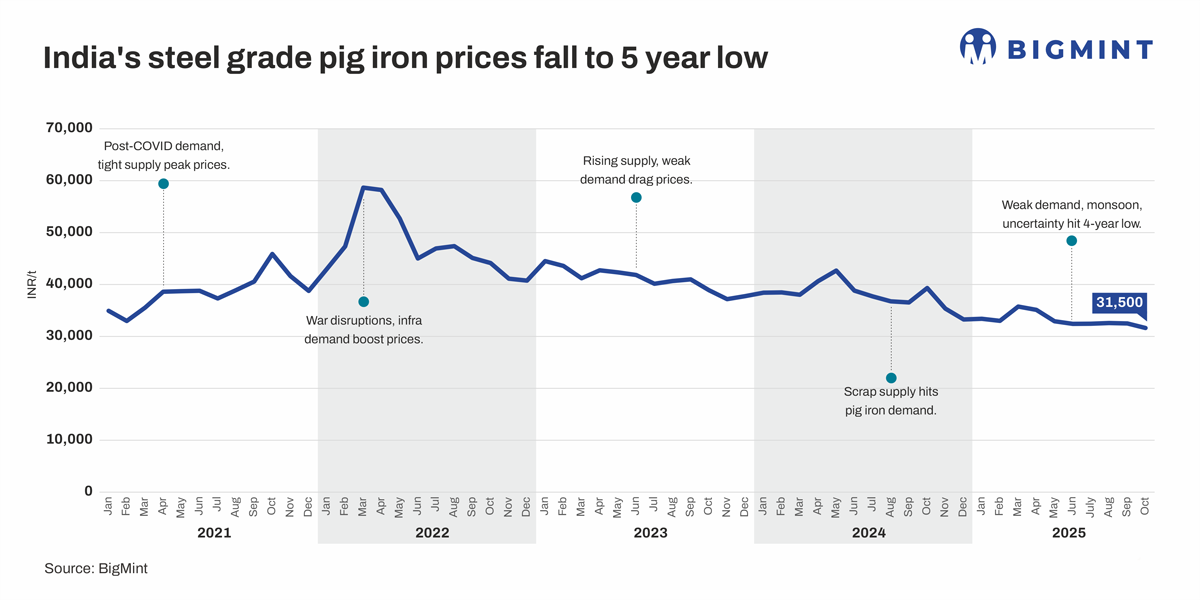

India’s pig iron market recorded a sustained depression in H1FY’26, with steel-grade prices in Durgapur approaching a five-year low of INR 31,600/tonne (t) exw in October 2025, due to a persistent gap between supply and demand.

However, with India entering its peak steel consumption season in H2FY’26, market participants expect this trend to reverse. A measured recovery may be in store, going by the market dynamics registered in the first half of November.

Price trends

Average monthly prices of pig iron (exw-Durgapur) plunged by INR 2,700/t from April to June, before entering a period of relative stability over July to September.

Subsequently, Durgapur prices recorded a drop of INR 900/t to INR 31,600/t exw in October. However, till 15 November, prices averaged INR 31,900/t, showing a slight rise of INR 300/t from October. Spot prices of pig iron were higher by INR 1,100/t at INR 32,600/t on 15 November compared to 31 October.

This rise follows an improvement in market sentiment in the first half of November, attributed to higher realizations from finished steel products. Daily spot prices of induction furnace (IF) rebars have trended up slightly since 31 October. IF rebar prices were higher by INR 300/t at INR 42,600/t on 15 October.

However, on average, IF-rebar prices, exw-Raipur, in the first half of November were lower by INR 100/t at INR 41,400/t compared to October’s monthly average of INR 41,500/t, possibly indicating that the rebound in demand for finished steel products remains modest.

Early-November auction results also signal a potential uptrend. SAIL’s Rourkela Steel Plant (RSP) auctioned 4,000 t of steel-grade pig iron on 3 November, with the entire quantity booked at an average price of INR 31,700/t exw, an increase of INR 1,150/t compared to the previous auction on 24 October.

NMDC’s Nagarnar Steel Plant auctioned 5,000 t of steel-grade pig iron on 7 November, with the entire quantity booked at an average price of INR 30,850/t (by road), higher by INR 350/t.

Will pig iron prices recover in H2FY’26?

Will pig iron prices recover in H2FY’26?

Preliminary analyses suggest that a modest price recovery or, at least, stability, may be in store for pig iron in H2FY’26, but the pace is likely to be slow, given a persistent supply glut and the overall weakness in finished steel tags.

However, it is important to note that optimism around the traditional peak season seems to be driving this expectation rather than concrete demand triggers. As such, caution persists.

Production, consumption projections for H2FY26

While pig iron production remained stable y-o-y in H1FY’26 at 4.31 million tonnes (mnt), BigMint projects a 7% y-o-y increase in H2FY’26 to 4.60 mnt. Meanwhile, consumption decreased by 3% y-o-y to 4.21 mnt in H1FY’26, but the volume is expected to increase by 10% y-o-y to 4.45 mnt in H2FY’26.

Despite consumption growth outpacing production in H2FY’26, output is expected to be higher by 0.15 mnt. This is lower than H2FY’25’s production surplus of 0.24 mnt but is higher than the 0.10 mnt recorded in H1FY’26, indicating that the market is likely to continue facing a supply glut.

- Importantly, construction and infrastructure activity is expected to pick up, driving up finished steel demand. Previously, in H1FY’26, the slump in demand for construction steel during the monsoon season prompted production cuts by some smaller steelmakers.

- Market participants have observed that small orders are gradually returning in the foundry and engineering segments, with work resuming on projects that had been halted during the monsoon. Foundries are likely to ramp up utilisation beyond 50-60% as order inflow improves.

- The automotive sector may also continue to lend steady support, with GST reforms expected to encourage sales. The ICRA expects increased tractor demand in the near term due to the imminent implementation of the TREM V emission norms from 1 April 2026. Price hike concerns may push buyers to purchase vehicles in advance.

- Met coke prices seem to be on a slow uptrend in East India, averaging INR 31,300/t exy-Jajpur till 15 November. In October, prices were at INR 29,900/t, rising INR 500/t m-o-m. Trading activity has picked up, and limited import arrivals, the anti-dumping duty, and elevated coking coal costs may keep domestic prices firm in the near term.

Leave a Reply