- Leading coil producer trims 316 prices for 2nd time in Nov

- Production costs fall as ferro molybdenum hits 4-month low

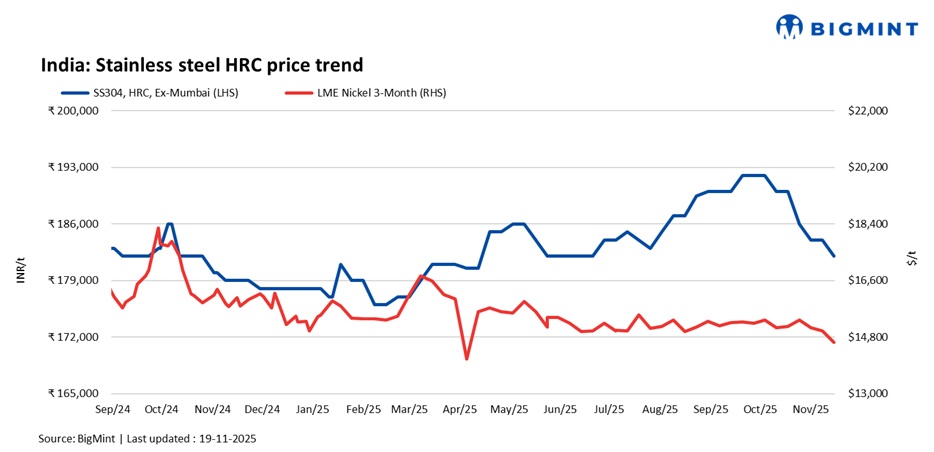

India’s stainless steel market trended down this week amid persistent weak demand and market uncertainty.

Finished flats prices dip w-o-w

Bigmint’s benchmark assessment for stainless steel 304 hot-rolled coils (HRCs) stood at INR 182,000/t, ex Mumbai, down INR 2,000/t w-o-w.

Additionally, India’s leading stainless steel coil manufacturer has reduced its 316 coil prices by INR 5,000/t, effective 17 November — the second cut this month. The revision comes amid a temporary relaxation on imports, allowing the use of non-BIS-compliant material until 31 December, and a sharp decline in ferro molybdenum prices, a key input for 316 grades, which have fallen to a four-month low.

A market participant commented, “The stainless steel market has slowed sharply after Diwali, with inquiry levels falling to less than half of expectations, triggering widespread panic selling as cheaper imported material continues to land. With a surplus already building in imports, buyers believe prices may fall further, prompting aggressive discounts and quick inventory liquidation.”

Imported 304 HRCs were indicated at INR 175,000-180,000/t ($1,900-2,000/t).

Finished longs prices dip w-o-w

BigMint’s benchmark assessments for stainless steel 304L (25 to 100 mm) black round bars were at INR 156,000/t, ex-Mumbai. Meanwhile, SS 316L black round bars were at INR 276,000/t, ex-Mumbai. Both were steady w-o-w.

Overall, the longs market remained quiet due to limited demand and poor sales. However, the wire rod segment bucked the trend, with healthy demand.

Indicative FOB prices for stainless steel longs were as follows: Indian 304 bright bars were at $2,050-2,100/t and 316 bright bars at $3,600-3,650/t, while Vietnam’s 304 bright bars were quoted at $1,880-1,950/t and 316 bright bars at $3,400-3,450/t.

China market

China’s stainless steel market remained subdued as weak stainless steel futures continued to drag down spot sentiment. Despite earlier price cuts by major mills, spot demand failed to recover, keeping transactions sluggish across key hubs such as Wuxi and Foshan. Futures hovered near yearly lows, pressured by declining nickel and soft macro cues, while spot prices for major grades such as 201, 304, 316L and 430 stayed at the lower end of recent ranges. With the year-end off-season weighing on downstream demand, limited production cuts, and easing raw material costs, overall market sentiment remained pessimistic, and prices are expected to remain under pressure in the near term.

LME nickel tags slip w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $14,630/t, down 2.6% compared to last week’s $15,005/t. Nickel stocks at LME-registered warehouses stood at 257,832 t, up by 1.8% compared to 252,750 t in the previous week.

Chinese stainless steel & NPI prices

In China, prices of domestic 304-grade stainless steel cold-rolled coils (CRCs) stood at RMB 13,350/t ($1,877/t) exw, while FOB values of 304-grade CRCs were firm at $1,860/t.

Chinese portside prices of nickel pig iron (NPI) (8-12%) were at RMB 920/t ($129/t). Meanwhile, Indonesian FOB prices of NPI (10-14%) stood at $114.69/t.

Raw materials scenario

Ferro molybdenum: Indian ferro molybdenum prices held steady w-o-w from the previous assessment on 12 November 2025. The market remained quiet, with limited trading activity and weak buying interest, driven by subdued demand from the stainless steel sector.

As per BigMint’s assessment on 19 November, ferro molybdenum prices in India stood at INR 2,775,000/t ($31,372/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices dropped by INR 1,000/t w-o-w to INR 115,500/t ($1,305/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices saw a significant increase of INR 7,500/t ($85/t) as compared to the assessment on 10 November. Prices increased, as the availability of material remained limited, which prompted sellers to raise their offers.

Ferro silicon prices in India were INR 97,000/t ($1,094/t) exw-Guwahati, as per BigMint’s assessment on 17 November. In Bhutan, prices increased by INR 8,500/t ($96/t) w-o-w to INR 97,500/t ($1,100/t) exw.

Outlook

The stainless steel market is expected to remain under pressure in the near term amid weak demand and ample supplies in the domestic market, and with import competition re-emerging, further price softening appears likely.

Leave a Reply