- Black Sea mills cut offers amid weak demand, winter slowdown

- Chinese domestic billet tags up, market sentiment remains weak

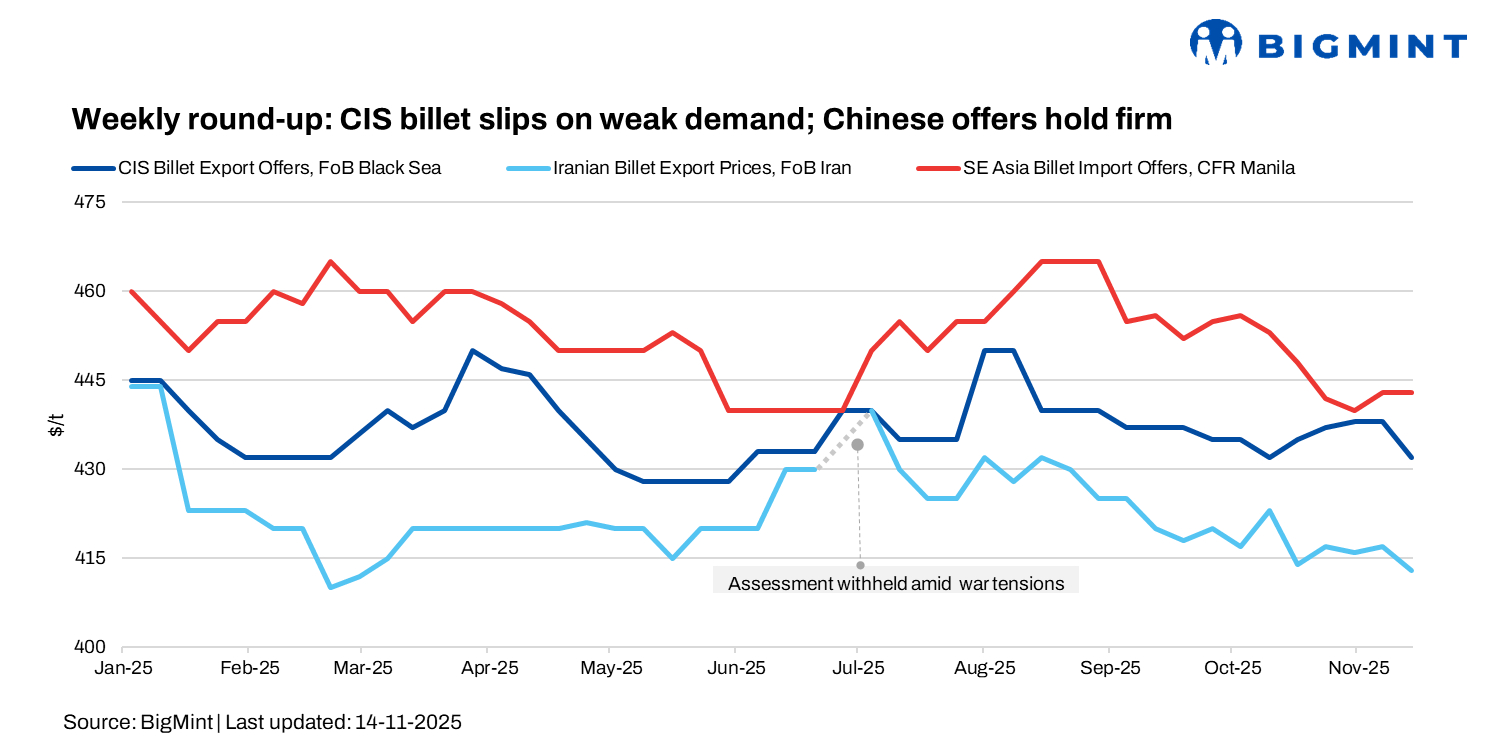

Global billet and scrap markets showed mixed momentum this week (week 46). Prices across regions slipped by up to $6/t on muted buying interest, even as Chinese exporters held firm. Chinese 3SP-grade billet offers edged up by $2-3/t to $456-460/t CFR Turkiye, while buyers remained at $442-445/t CFR, widening the negotiation gap. With weakening demand in the Black Sea and steady deep-sea scrap bookings in Turkiye, market sentiment stayed cautious.

Turkiye’s mills remained active toward the weekend, securing fresh deep-sea cargoes from the US West Coast and Venezuela. A Marmara mill booked 12,000 t of HMS 80:20 at $353.5/t CFR and 20,000 t of shredded at $373.5/t CFR — one of the few West Coast deals as suppliers diverted cargoes amid subdued Asian demand. Another mill purchased Venezuelan HMS 80:20 at $349-350/t CFR, while an unconfirmed European-origin HMS deal was heard at $349/t CFR.

Exporters continued to push higher, with European targets around $355/t CFR and US sellers eyeing $360/t CFR. Collection rates are expected to tighten during winter offering support, while rebar offers firmed up at $555-560/t FOB despite softer bids.

CIS market

Black Sea billet exporters lowered their prices this week, reversing earlier expectations of stability or slight increases. This was due to overseas buying remaining weak and domestic demand in Russia softening further. Russian mills reduced offers for December-January shipment to $435-436/t FOB, down from the previous $440-445/t held for nearly three weeks.

Some buyers reported even lower achievable levels, with an additional discount offered for firm negotiations. Donbas-origin billet was also adjusted down to $430-435/t FOB.

Although scrap prices in Turkiye remain firm, CIS billet sellers were compelled to cut levels as mills began selling December production amid slowing domestic consumption and likely logistical constraints ahead of winter. Snow is expected soon in several central and northern Russian regions, prompting producers to push exports quickly to avoid inventory buildup.

In Turkiye, no new official CIS offers emerged, but the workable range was assessed at $445-450/t CFR ($425-430/t FOB), noticeably softer than last week’s $450-455/t CFR indications. Turkish buyers remained price-sensitive, with many unwilling to pay above $450/t CFR, especially for smaller parcels and payment terms less favourable to producers.

Tunisia received CIS billet offers at around $465-470/t CFR (equivalent to roughly $430-435/t FOB), which market sources considered acceptable for that market. Given reduced offer levels, limited interest, and the absence of confirmed deals, CIS billet workable indicatives have fallen by $5-6/t to $430-434/t FOB levels.

China

Chinese billet prices rose slightly from RMB 2,940/t ($413/t) to RMB 2,950/t ($416/t) w-o-w, while SHFE January rebar futures gained RMB 23/t ($4/t). Despite this uptick, market sentiment stayed weak as demand remained sluggish, exports softened, and mills cut output amid high raw material stocks. Brief speculative restocking and late-week cost support from firmer iron ore and coke offered only limited price stability.

Middle East

Saudi Arabia remains dependent on imported billets as domestic steelmaking capacity continues to trail demand. With CIS supplies disrupted, China has emerged as Saudi Arabia’s primary source offering consistent volumes and the most competitive pricing, though buyers highlight frequent price volatility, longer lead times, and logistical limitations for handling bulk shipments.

Chinese billet remains the cheapest option at $460-465/t, compared with Omani material at $470/t, UAE-origin at $480/t, and Bahraini billets at $530/t. Monthly inflows of 50,000-60,000 t have helped Chinese suppliers effectively fill the gap left by CIS producers and support ongoing rolling operations.

Iran’s steel market saw mixed trends this week. Early in the week, billet slipped by 4,000 rial/kg ($10/t) to 355,500 rial/kg ($845/t) amid weak domestic demand, while rebar rebounded by 5,000 rial/kg ($12/t) to 410,000 rial/kg ($974/t). Higher gas tariffs and rising liquidity signalled upcoming cost pressure for mills.

Towards midweek, sentiment improved slightly. Billet edged up by 500 rial/kg ($1/t) to 356,000 rial/kg ($846/t), and rebar jumped 12,000 rial/kg ($29/t) to 422,000 rial/kg ($1,003/t), supported by stronger demand, tighter mill deliveries, and active export orders from both borders. Flat products also firmed up on improved export bookings. Near-term prices may stay supported despite soft domestic consumption.

Leave a Reply