- High-CV prices weaken slightly; mid-CV, low-CV tags rise

- Demand shifts, utility buying influence price movements

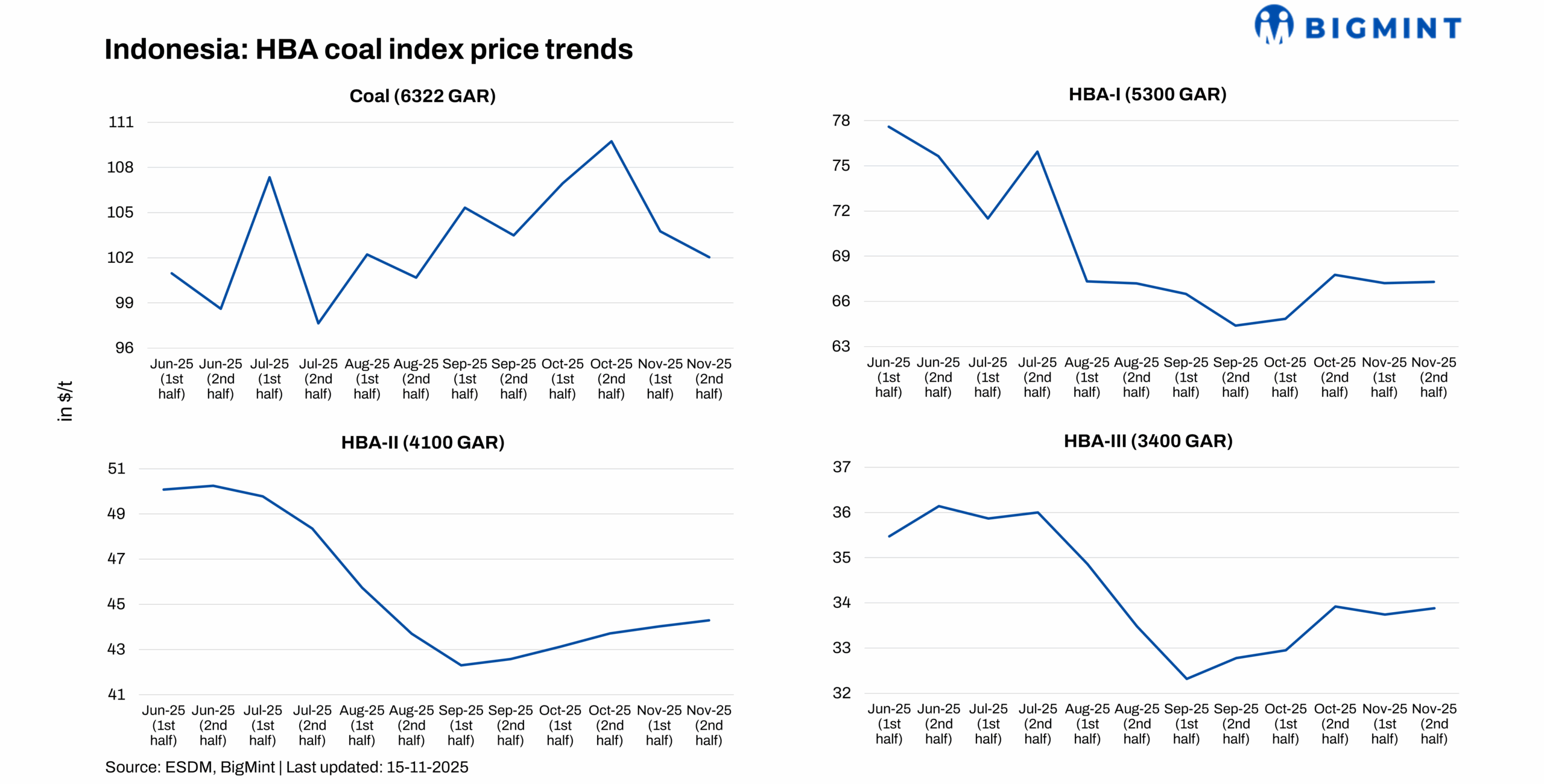

Indonesia’s Ministry of Energy and Mineral Resources (ESDM) has released the updated Harga Batubara Acuan (HBA) for the second half of November 2025, revealing a mixed pricing pattern across coal grades. The new data reflects shifting global demand trends, regional supply adjustments, and the changing economics of fuel substitution in Asia’s energy markets.

High-CV coal records mild downtrend

High-calorific value (high-CV) coal prices (6,322 kcal/kg GAR) slipped by 1.7% to $102.03/t, continuing the cautious tone seen earlier in the month.

The decline is largely tied to moderating seaborne demand from China and India, alongside ongoing supply recalibrations in major exporting hubs. The reduction remains moderate, reflecting a market that is directionally weak but not under significant pressure.

Mid-CV coal holds stable with marginal uptick

Mid-calorific value (mid-CV) (5,300 kcal/kg GAR) coal edged up 0.1% to $67.29/t, indicating a broadly stable demand scenario. Slight improvement in procurement from the Asian steel and manufacturing sectors supported the grade.

Its competitive pricing and efficiency continue to attract buyers seeking predictable fuel costs amid uncertain macroeconomic conditions. Despite the small movement, the grade remains in a narrow price band, reinforcing a steady market environment.

Low-CV coal extends its upward momentum

Low-calorific (Low-CV) value grades maintained positive momentum into mid-November. The 4,100 kcal/kg GAR variety rose 0.6% to $44.29/t, while the 3,400 kcal/kg GAR grade increased 0.4% to $33.88/t.

These gains were primarily driven by strong domestic demand from utilities prioritising affordability and fuel value. Low-CV coal continues to serve as an economic stabiliser for power producers, especially under rising cost pressures in alternative fuels.

Outlook

Indonesia’s coal index movement remains shaped by ongoing shifts in global energy preferences, fluctuating industrial activity in Asia, and the balancing of supply pipelines. Coal prices are expected to stay range-bound in the near term, with global demand cues remaining mixed. High-CV coal may see limited upside, while mid- and low-CV grades could retain stability, supported by firm domestic consumption and cost-driven buying interest.

Leave a Reply