- Supramax, Panamax segments reflect optimistic mood

- Tight tonnage, higher bunker prices lend support

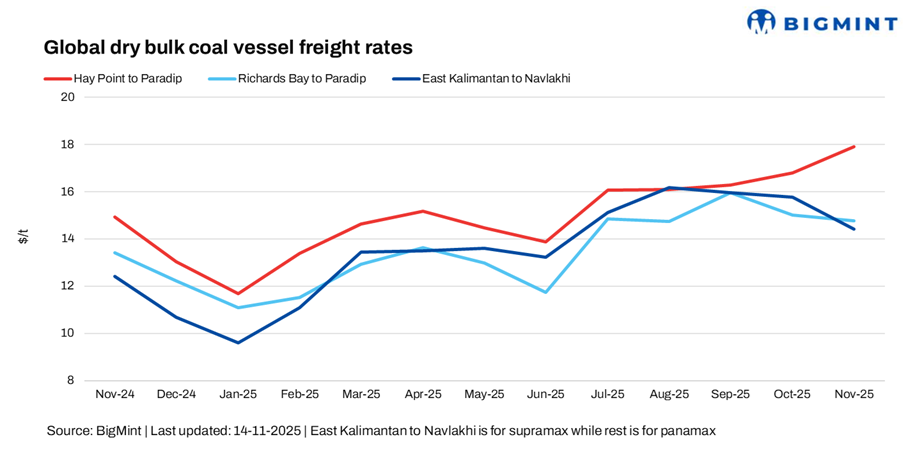

Dry bulk coal freight rates to India edged higher this week across key routes supported by firmer Pacific market sentiment, improved fixture activity, and a positive shift in FFA levels.

Despite uneven buying interest from Indian importers, tightening vessel availability in certain regions and steady demand for coal and minor bulks helped lift rates. Overall, both Panamax and Supramax segments reflected an optimistic mood, marking a reversal from the softer conditions seen earlier.

“Asia-Pacific Supramax freight rates strengthened w-o-w, supported by firm sentiment in the Pacific market even as some participants noted a mild slowdown in activity. The Indian Ocean market also showed a positive trend, lifted by the steady Pacific market,” a source said.

Coal freights on the Australia-India route strengthened this week, rebounding on the back of more active fixture activity and charterers fixing vessels at higher levels. Improved buying interest from Indian utilities and traders supported sentiment, prompting a pickup in fresh inquiries. Tonnage supply, although still adequate, tightened slightly in key loading areas as more vessels were drawn into Pacific employment, adding upward pressure on rates.

Freights on the South Africa-India route edged higher this week despite limited fixture activity, supported by firmer Pacific rates and an uptrend in FFA levels that lifted overall market sentiment. Although inquiries remained thin due to subdued sponge iron output in India, the spillover strength from the Pacific basin encouraged owners to hold for higher numbers.

Supramax freights on the Indonesia-India route also climbed w-o-w. A ship operator noted, “The Supramax Indonesian market remains firm and steady, with no signs of a slowdown appearing so far”.

However, another source mentioned, “The Supramax market feels slightly softer, with overall activity just a touch quieter”.

Rising bunker prices are adding upward pressure on dry bulk coal freight rates, as higher fuel costs directly increase operating expenses for vessel owners. “With marine fuel accounting for a significant share of voyage costs, owners are seeking to pass on these additional expenses through higher freight rates, especially on longer-haul routes such as Australia-India and South Africa-India”, a source told BigMint.

Meanwhile, India’s portside thermal coal inventories slipped 3.2% w-o-w to 12.57 million tonnes (mnt) in week 45 (ending 9 November) from 12.98 mnt in week 44. The decline was driven by limited vessel arrivals and weak restocking sentiment, especially across the west coast, while select eastern ports saw recovery post cyclone disruptions.

Route-wise updates

- Australia (Hay Point)-India (Paradip), Panamax: Freights from Australia to India rose w-o-w by around 1.07/dry metric tonne (dmt) to $18.39/dmt.

- South Africa (Richards Bay)-India (Paradip), Panamax: Panamax freights on the South Africa to India route edged up marginally w-o-w by $0.2/dmt to $15/dmt.

- Indonesia (East Kalimantan)-India (Navlakhi), Supramax: Supramax coal freights on the Indonesia to India route also followed the suite and stood at $14.72/dmt, an increase of $0.99/dmt, w-o-w.

Market highlights:

- Baltic index rises w-o-w: The Baltic Exchange’s dry bulk index for Panamax and Supramax vessels increased this week, with the Panamax index rising 80 points w-o-w to 1,897 and the Supramax index rising 75 points to 1,387. The indices rose w-o-w on stronger grain and coal demand, improved Pacific sentiment, and increased fixture activity. Firmer FFA levels and tighter tonnage in key regions also supported owners’ sentiment, lifting rates in both segments.

- Brent crude futures stable w-o-w: Brent crude oil futures inched down slightly w-o-w by about $0.2/barrel (bbl) to $63.8/bbl on 14 November 2025 against $64/bbl on 7 November. Brent crude edged down w-o-w as weak demand sentiment and lingering oversupply concerns outweighed any support from geopolitical risks, keeping prices slightly softer.

Outlook

Dry bulk coal freight rates to India are expected to stay stable to slightly firm in the near term, supported by strong Pacific sentiment and steady FFA levels. Even with uneven coal demand from Indian buyers, positive momentum from the Pacific and potential tightening of vessels in Indonesia and Australia should keep owner sentiment buoyant.

However, gains may stay limited, as Indian inquiries remain selective and cargo flow from South Africa is still subdued. Australia-India rates could firm up if Pacific demand stays high, while South Africa-India may see only modest movements. Overall, rates are likely to remain steady or mildly higher.

Leave a Reply