- JPY weakness supports Japan’s rising scrap export tags

- Weather disruptions tighten US scrap collection flows

Japan’s scrap export prices climbed up on stronger tender results and Tokyo Steel hikes, though Vietnamese demand stayed muted. US export and domestic prices held steady, supported by tight supply despite weak finished steel demand.

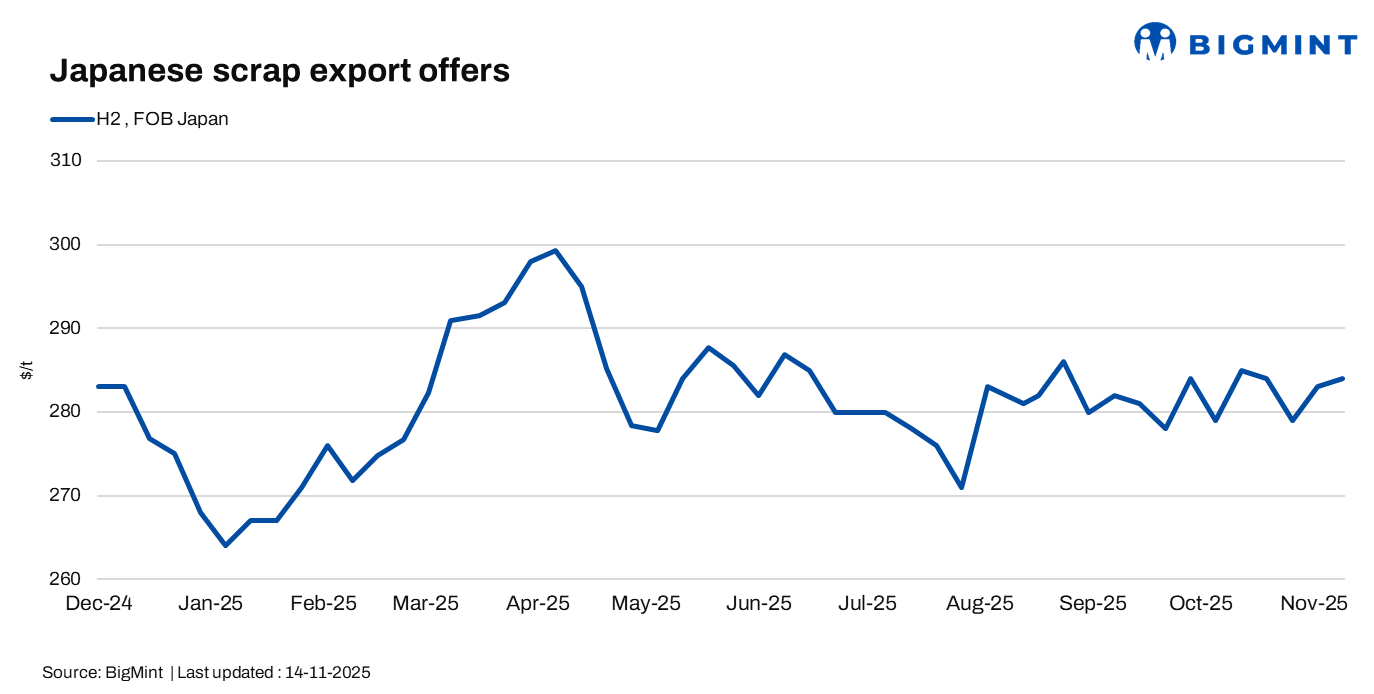

Japan’s scrap export prices rise w-o-w

BigMint assessed Japan’s H2 scrap at JPY 43,900/t ($284/t) FOB Tokyo Bay, up JPY 500/t ($3/t) from the previous week.

In the November 2025 Kanto tender, H2 prices rose JPY 644/t to JPY 44,960/t ($291/t) — the fourth consecutive monthly increase. Additionally, a weaker JPY continued to support export offers. The total volume for which bids were made slipped to 121,100 t, while the per-ship cap was raised again to 20,000 t.

Tokyo Steel implemented its second price hike for November, lifting scrap prices by JPY 500/t ($3/t). Post-revision, H2 prices now range from JPY 39,000/t ($252/t) at Takamatsu to JPY 44,000/t ($284/t) at major plants.

H2 offers to Vietnam stood at $328-333/t CFR, up slightly, while bids remained at $320-325/t. Deals settled around $325-328/t. Seasonal rains and storms continued to dampen Vietnamese scrap demand.

US scrap export tags fall w-o-w

US ferrous scrap export prices eased slightly this week, even as another cargo was booked by a Turkish mill at steady levels. Tight supply and weather-related disruptions continued to offer support, though the market remained under pressure from high freight costs and weak finished steel demand in key destinations.

In the domestic market, November trade settled sideways, with prices of all grades rolling over from October. A combination of balanced supply-demand conditions, limited mill procurement, ongoing outages, shorter melting schedules, and a compressed shipping window kept pricing stable despite broader export softness.

FOB assessments (US East Coast, bulk)

HMS 80:20 – $325/t, down by $2/t w-o-w.

Shredded – $345/t, down by $2/t w-o-w.

US-origin HMS 80:20, bulk – CFR assessments

Turkiye – stable w-o-w at $356/t.

Vietnam – down by $3/t w-o-w at $345/t.

Bangladesh – down by $1/t w-o-w at $351/t.

Outlook

Japan’s scrap market is expected to remain firm on stronger tenders, with support from a weaker JPY, though export activity may remain slow due to muted Vietnam demand and seasonal weather. In the US, dock prices are likely to face upward pressure as supply tightens, with participants expecting more noticeable increases from January to February despite high freight rates limiting near-term movement.

Leave a Reply