- Chinese buyers stay active for clean grades, limiting supply

- KEI’s Gujarat plant boosts downstream copper outlook

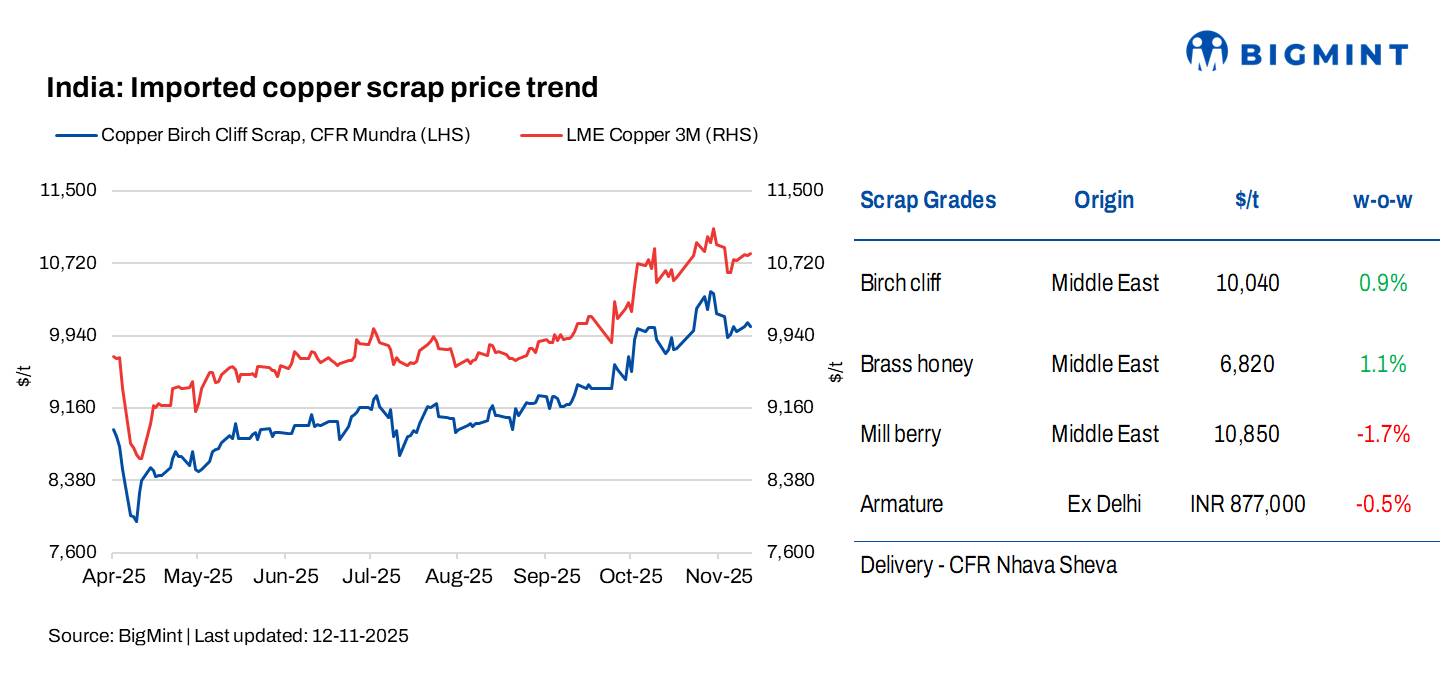

Imported copper scrap prices in India inched up w-o-w, tracking positive movements on London Metal Exchange (LME) futures. Meanwhile, domestic copper scrap prices edged down, displaying a muted-to-steady tone through the week. Market activity has gradually improved following the post-festive slowdown, but buyers remained cautious due to high inventories.

According to BigMint’s assessment, Birch Cliff scrap was assessed at $10,040/tonne (t), up by 0.9% w-o-w, while US motors mix stood at $1,200/t (both CFR Mundra), up by 0.85% w-o-w.

LME copper prices rise w-o-w

LME copper prices stood at $10,805/t on 12 November 2025, up by 1.7% from the $10,625/t recorded a week earlier.

Meanwhile, copper stocks at LME-registered warehouses stood at 136,250 t, up by 2,275 t compared to 133,975 t in the previous week.

The long-term outlook for global copper prices remains positive, backed by tight raw material supply, lower TC/RCs, and major investments such as the Adani-Caravel Minerals deal, which secures feedstock for Kutch Copper’s Gujarat smelter — reflecting confidence in structurally strong copper demand.

Market updates

The imported copper scrap market remained slightly soft this week, as offers declined in line with a drop in LME prices at the beginning of the week. Notably, LME prices fell from around $10,920/t before gradually recovering later in the week. Suppliers from the Middle East and Europe trimmed offers marginally amid subdued Indian buying following the Diwali holidays.

However, Chinese buyers stayed active, particularly for cleaner grades such as Berry, Candy, and Birch/Cliff, tightening regional availability. Indian importers remained cautious due to high inventories and steady secondary CCR demand, with limited trades reported at slightly discounted levels.

Market participants expect prices to remain range-bound in the near term, with potential support if LME prices stabilise or Chinese demand persists through mid-November.

Price levels (CIF China):

- Birch/Cliff (EU): 91.5% of LME

- Clean Brass Honey (EU): 65% of LME

- Candy Berry (EU): 97.5% of LME

Meanwhile, UAE-origin Birch/Cliff scrap was heard at around 93% of LME, CIF Mundra, while EU-origin Brass Honey was reported at 59% of LME, CIF Mundra. Additionally, Meatballs scrap (US-origin) was assessed at $2,050/t CFR Mundra, and Motor scrap (50% Cu) was quoted around $1,200/t CIF Mundra.

In the domestic market, demand for high-grade copper scrap and CCR held steady, driven by consistent offtake from the wire and cable sector. Market activity has gradually improved post-festive season as large fabricators and OEMs resumed restocking.

The announcement of KEI Industries’ new Gujarat plant further boosted confidence in the downstream copper segment, with expectations of stronger medium-term demand for both refined and secondary copper. However, near-term trade volumes remained modest, and domestic prices largely tracked LME trends, maintaining a muted-to-steady tone this week.

According to BigMint’s assessment, domestic copper prices in India showed a slight decline w-o-w. Copper armature was assessed at INR 877,000/t, down by 0.45% this week. Copper primary CC wire rods (CCR) stood at INR 1,005,000/t, down 0.5%, while copper secondary CC wire rods (CCR) were at INR 937,000/t, easing 0.32% w-o-w.

Outlook

Copper scrap prices in India are expected to remain range-bound in the near term, supported by steady domestic demand and potential stabilisation in LME prices. Any sustained Chinese buying or recovery in global industrial activity could lend upside momentum. However, high inventories and cautious buying sentiment may cap sharp gains. Market participants anticipate a gradual improvement through mid-November as liquidity and restocking activity increase.

Leave a Reply