- Nickel prices hold firm in Q3CY’25 despite oversupply

- Global smelting activity drops in Sep’25, led by China

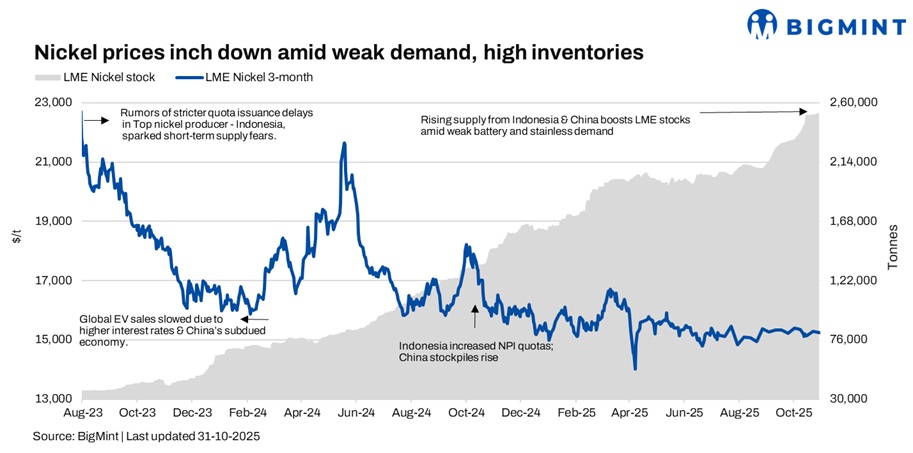

Nickel prices on London Metal Exchange (LME) showed volatility during the week with with three-month contracts settling at $15,245/t on 31 October, down slightly by $40/t w-o-w from $15,285/t in the previous week. During the same period, nickel stocks on the LME remained elevated, closing at around 252,102 t, largely range-bound against last week’s 250,854 t.

Nickel futures experienced downward pressure amid several macroeconomic headwinds such as persistent global oversupply, weakening demand from stainless steel and EV sectors, and a strong US dollar.

Market highlights

Nickel market stabilises in Q3CY’25, but structural oversupply persists

Nickel prices stabilised in Q3CY’25 despite ongoing oversupply concerns. Market headwinds included the US EV tax credit expiration and tariff disputes with China, impacting demand uncertainty. Indonesia’s quota cuts have not fully alleviated supply imbalances amid rising nickel stockpiles. While US EV demand softened temporarily, Chinese demand showed signs of recovery. Shifts in EV battery chemistries also affected nickel consumption patterns. Overall, supply discipline remains critical for price recovery.

Global nickel smelting activity declines in Sep’25

Global nickel smelting activity weakened notably in September. China drove much of the slowdown, with inactive capacity rising for a third consecutive month to 42.9%, pressured by reduced nickel pig iron (NPI) output and idling of major smelters. Indonesia saw a slight pick-up in activity, while Europe and Africa remained largely unchanged. Meanwhile, Class 1 nickel operations showed relative stability, supported by steady smelter performance in South Africa.

Nornickel Nickel output rises q-o-q, annual guidance intact

Nornickel reported Q3CY’25 nickel production at 53,600 t, up 18.4% q-o-q due to increased processing of semi-finished materials, though 4% lower y-o-y. Total nickel output for January-September stood at 140,000 t, down 4% y-o-y. The company maintained its full-year guidance at 196,000-204,000 t. Copper production in Q3 reached 100,105 t, down 4% q-o-q and 7% y-o-y, with nine-month output at 313,300 t, approaching a 343,000-355,000 t annual target.

Outlook

Nickel prices are forecast to remain under pressure due to ongoing concerns about weakened stainless steel demand and high inventory levels. Global economic uncertainties continue to curb industrial buying, while markets await supply adjustments from key producers.

Leave a Reply