- IF-rebar prices rise as inventories drop sharply

- HRC prices drop, post-festive demand lull continues

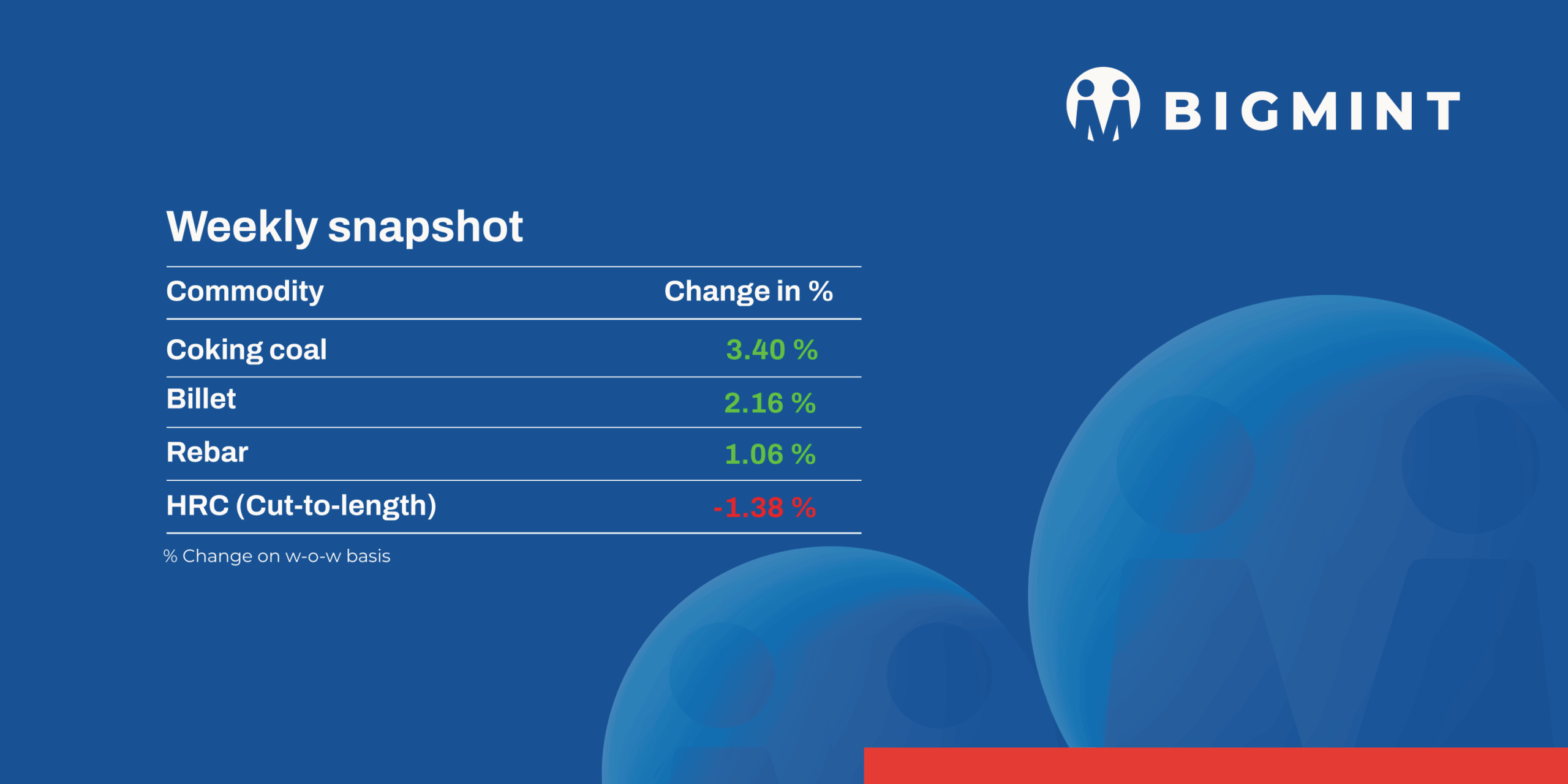

The domestic steel market saw a positive trend in prices during week 44 (27-31 October 2025). Semi-finished steel prices increased by INR 500-1,400/tonne (t) as demand improved following the Diwali festive season.

Iron ore, pellet

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index increased by $2/t w-o-w to $72/t FOB east coast on 30 October. Around 165,000 t of iron ore export deals were recorded by BigMint this week, while a few deals were heard to be under negotiation. Some bids were received at 16% discount for traders’ cargo, but deals are yet to be concluded for Fe 57% grade fines.

- NMDC Chhattisgarh conducted an auction for 75,900 t of iron ore from its Bacheli mines on 30 October. The entire quantity of 12,900 t of DR CLO (Fe 67%) fetched an 18% premium (base INR 6,250/t), while 8,000 t of sized lumps (10-20 mm, Fe 65.5%) secured 13.5% premium (base INR 5,700/t). In contrast, 21,500 t of fines (Fe 64%) were sold at base INR 4,790/t, and 2,000 t ROM were booked at base INR 5,500/t. Prices were on FOR basis, including royalty.

- Godawari Power & Ispat Ltd (GPIL) has resumed operations at its 1.8 mnt/year iron ore pellet plant in Raipur, Chhattisgarh, from 30 October. A production loss of nearly 150,000 t was reported during the downtime. However, it was stated that annual production targets are expected to be achieved without further maintenance shutdowns. Notably, GPIL’s pellet offers are expected to resume from 1 November at INR 10,200/t exw.

- Indian pellet exporters concluded around 135,000 t of pellet (Fe 62.5-64%) export deals this week amid decent pellet premiums and a hike in global iron ore prices. Deals were heard concluded at $120-130/t CFR China.

Coal

- South African coal demand in India remained subdued this week as cyclone disruptions and slow post-festive activity limited trade. RB2 and RB3 held steady at INR 8,200/t and INR 7,100/t, respectively, across Paradip, Vizag, and Gangavaram. Portside stocks rose slightly to 13.33 mnt, while sponge output fell to a 7-month low of 4.71 mnt in September.

- Domestic coal prices rose slightly this week after SECL allocated about 728,000 t of coal through auctions on 24-25 October. Prices of 5,000 GCV increased to INR 6,350/t ex-Bilaspur, while 4,500 GCV reached INR 5,200/t, up by INR 50-100/t w-o-w. Despite the price rise, trading activity stayed subdued, with limited inquiries from end-users amid sluggish demand.

- Met coke prices in India showed mixed regional trends this week. BF-grade met coke (25-90 mm) rose INR 600/t w-o-w to INR 30,500/t ex-Jajpur, while prices were stable at INR 30,000/t ex-Gandhidham. Foundry-grade coke was unchanged at INR 35,500/t ex-Rajkot. A deal for 22,500 t at INR 31,500/t signalled firm demand in eastern India, while western activity stayed subdued amid the festive lull.

- BigMint’s premium hard coking coal (PHCC) index increased $3/t w-o-w to $210/t CNF Paradip on 31 October, tracking firmer Australian offers supported by stronger Chinese market prices. While no fresh trades were heard in India, sentiment stayed bullish amid rising met coke values.

Ferrous scrap

- India’s imported ferrous scrap market remained weak, with activity subdued due to regional holidays, a wide bid-offer gap, and sluggish steel demand. Mills stayed away from new bookings as falling DRI prices and ample domestic scrap availability reduced import appetite, relying instead on existing inventories.

- Offers for shredded scrap were mostly heard between $346-352/t CFR, while HMS 80:20 hovered around $320-330/t and busheling at $360-368/t. Buyers’ bids consistently remained $10-15/t below offers, resulting in limited deals and low port arrivals, particularly at Chennai and Mundra.

Ferro alloys

- Silico manganese: Indian silico manganese (60-14) prices inched up by INR 500/t ($6/t) w-o-w to INR 71,800-72,100/t ($809-812/t) in Durgapur, Raipur, and Vizag. The uptrend was supported by tight supply, labour shortages during the festive period, and bulk order fulfillment by key producers.

- Ferro manganese: Indian ferro manganese (HC 70%) prices rose slightly by INR 500/t ($6/t) w-o-w to INR 72,000/t ($811/t) exw-Durgapur, while prices inched up by INR 600/t ($7/t) w-o-w to INR 72,100/t ($812/t) exw-Raipur, amid limited availability and steady demand.

- Ferro silicon: Indian ferro silicon (Si 70%) prices inched up by INR 500/t ($6/t) w-o-w to INR 88,000/t ($991/t) exw-Guwahati, while Bhutan prices remained steady w-o-w at INR 87,600/t ($987/t). Overall, prices remained largely stable amid limited inquiries, with market participants awaiting Bhutan’s November offers.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si 4%) prices declined by INR 1,400/t ($16/t) w-o-w to INR 119,000/t ($1,340/t) exw-Jajpur.

- Meanwhile, SAIL’s Bhilai Steel Plant (BSP) has floated a tender to procure 400 t of high-carbon ferro chrome (Cr: 60-70%, C: 6-8%, 25-70 mm), with the bid submission deadline set for 12 November. Under the reverse auction qualification rule, the highest-priced bid will be excluded.

Semi-finished

- India’s semi-finished steel market witnessed a notable uptrend this week, as per BigMint’s assessment. Domestic billet prices across major markets increased by INR 500-1,400/t ($5-15/t) w-o-w, with the sharpest gains of INR 1,000-1,400/t ($11-15/t) observed in Mumbai, Raipur, and Raigarh. The rise was primarily driven by improved buying activity in the semi-finished segment, supported by a gradual recovery in finished steel offtake that strengthened market sentiment and spot trade volumes.

Metallics

- Similarly, sponge iron prices rose by INR 200-1,350/t ($2-15/t) across key producing regions, as sellers lifted spot offers amid better material bookings compared with the previous week. The most significant increases of INR 1,200-1,350/t ($13-15/t) were observed in Raipur, Raigarh, and Rourkela, reflecting renewed market optimism and active restocking by downstream units.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, auctioned 5,000 t of steel-grade pig iron on 30 October, with the entire quantity booked at an average price of INR 30,500/t (by road). However, management approval is still pending. Bids were stable compared to the previous auction on 24 October, which saw an average price of INR 30,500/t (by road).

- SAIL-BSL in Bokaro, Jharkhand, held a steel-grade pig iron auction on 28 October, offering 9,000 t. Buyers booked 4,200 t at a base price of INR 30,700/ t. In the previous auction on 8 October, 1,200 t were booked at an average price of INR 32,000/ t, indicating a slight drop in prices.

- Indian direct reduced iron (DRI) export offers inched up by $3/t, settling at $314/t CPT Raxaul and $323/t CPT Benapole. However, import inquiries from Nepal and Bangladesh remained muted, as buyers stayed cautious amid subdued global steel market sentiment and soft finished steel demand in neighbouring markets.

Finished long steel

- IF-rebar: The induction furnace (IF) route rebar market witnessed a positive trend this week, supported by improved buying activity and better sales momentum. The market showed upward momentum post-Diwali, with increased participation from traders and major projects, strengthening overall market sentiment. Market participants highlighted better dispatches and lifting from buyers, leading to a reduction in inventory levels from around 15 days to nearly 10-12 days. The market is likely to remain positive in the near term.

- On a weekly basis, rebar prices surged by INR 100-1,700/t across regions except in southern markets such as Bangalore, Hyderabad, and Chennai, where prices fell by INR 700/t, INR 100/t, and INR 100/t, respectively, as per BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route for the 10-25 mm size were assessed at INR 38,000-38,400/t exw Raipur and INR 42,600-43,200/t exw Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 39,900-40,300/t exw Raipur.

- Trade reference prices of wire rod hovered at INR 38,600-39,200/t ex Raipur.

- BF-rebar: India’s trade-level blast furnace (BF) rebar prices edged down w-o-w across major markets. Some primary mills either increased their discounts or reduced list prices owing to subdued market sentiments post Diwali.

- However, trade-level BF rebar prices increased by 500/t ($6/t) w-o-w to INR 47,300/t ($533/t) exy-Mumbai, as per BigMint’s benchmark assessment on 31 October 2025. Prices are exclusive of GST at 18%. Hike in rebar prices by the IF-mills and market optimism led to the hike in offers in Mumbai.

- In the projects segment, prices hovered between INR 45,000-46,000/t ($507-518/t) FOR Mumbai.

Flat steel

- Trade-level prices of hot-rolled coils (HRCs) in India fell w-o-w to INR 46,700 -49,000/t ($529-556/t). Additionally, cold-rolled coil (CRC) prices fell w-o-w, with prices ranging between INR 52,500 -57,200/t ($595-648/t).

Domestic HRC prices edged lower, as overall demand was subdued. A source informed BigMint, “Market participation remains thin as post-festive sentiment is still soft, with many participants yet to return fully to active trading.” - India’s bulk imports of HRCs touched 343,891 t as of 25 October, based on vessel line-up data. Around 114,310 t of additional cargoes are expected by early-November.

- India’s bulk exports of HRCs touched 291,034 t as of 25 October and around 35,000 t of additional cargo is in transit.

- BigMint’s Indian HRC (S275) export index for Europe fell by $5/t w-o-w to $540/t FOB main port. Notably, an unconfirmed deal was heard concluded for November shipments at slightly lower levels.

- The Indian HRC (SAE 1006) export index for the Middle East and Vietnam remained steady w-o-w. This stability in prices is attributed to slow demand in both the regions.

Leave a Reply