- Steel exports reach 88 mnt in 9MCY’25

- Exports to MENA region increase by 20% y-o-y

- Total shipments may inch close to 120 mnt in CY’25

Morning Brief: Steel exports by China in the January-September 2025 period (9MCY’25) increased by 9% y-o-y to around 88 million tonnes (mnt) from 80.9 mnt in the corresponding period last year, as per BigMint data. China’s exports in September 2025 stood at 10.46 mnt, up by 3.1% y-o-y as compared to 10.15 mnt in September 2024, as per General Administration of Customs.

Steel exports remained elevated even against a high base and despite Chinese crude steel production dropping by 2.9% y-o-y in 9MCY’25.

The surge in exports can be attributed to weakness in domestic demand which can be explained by the sustained downtrend in the real estate and property markets in China for the fifth straight year in 2025. The building construction sector still accounts for over 40% of Chinese steel demand.

New home sales are projected to drop by 8% from last year to between RMB 8.8 trillion and RMB 9 trillion. With sales projected to be RMB 9 trillion or less this year, China’s property market will have halved in just four years, from RMB 18.2 trillion in 2021, according to a recent study.

That apart, investment growth in the infrastructure sector plummeted to 1.1% in January-September, while investment growth in the manufacturing segment dropped to 4%. Real estate development growth remained negative, at -14%.

So, domestic demand weakness is driving exports by China at a time when planned reduction in crude steel output is being carried out only gradually. Interestingly, the channeling of increased export volumes to diverse, economically emerging geographies such as the Middle East, Africa, Central and South America and even the CIS countries has been for China a key counterweight to US tariffs, and growing trade protectionist measures adopted by different countries including the EU.

China’s steel exports rise 10% y-o-y in Jan-Sep’25 despite trade and tariff barriers

Why did exports edge up in Sep’25?

M-o-m, steel exports increased by 10% in September compared to 9.51 mnt in August. According to Mysteel, China’s domestic demand for steel remained sluggish, which was exacerbated by logistics and construction disruptions caused by Typhoon Ragasa in Southern and Eastern China, combined with a pessimistic market outlook ahead of the Golden Week holidays. This created significant oversupply. With production outpacing consumption, producers sought to offload their excess inventory.

This substantial domestic overstock and bearish sentiment led to an increase in export activity, as mills aggressively diverted volumes to international markets to maintain production rates and clear inventory ahead of the National Day holidays from 1-8 October.

In September, Chinese hot-rolled coil (HRC) offers to the Middle East dropped by $8/t m-o-m to around $506/t CFR UAE, intensifying competition for other exporting countries, while Indian offers to the region were priced higher at approximately $526/t CFR UAE in the same month.

China’s FOB HRC offers for the month stood at $478/t, remaining the most competitive in the market. By comparison, Indian offers were significantly higher at $502/t FOB.

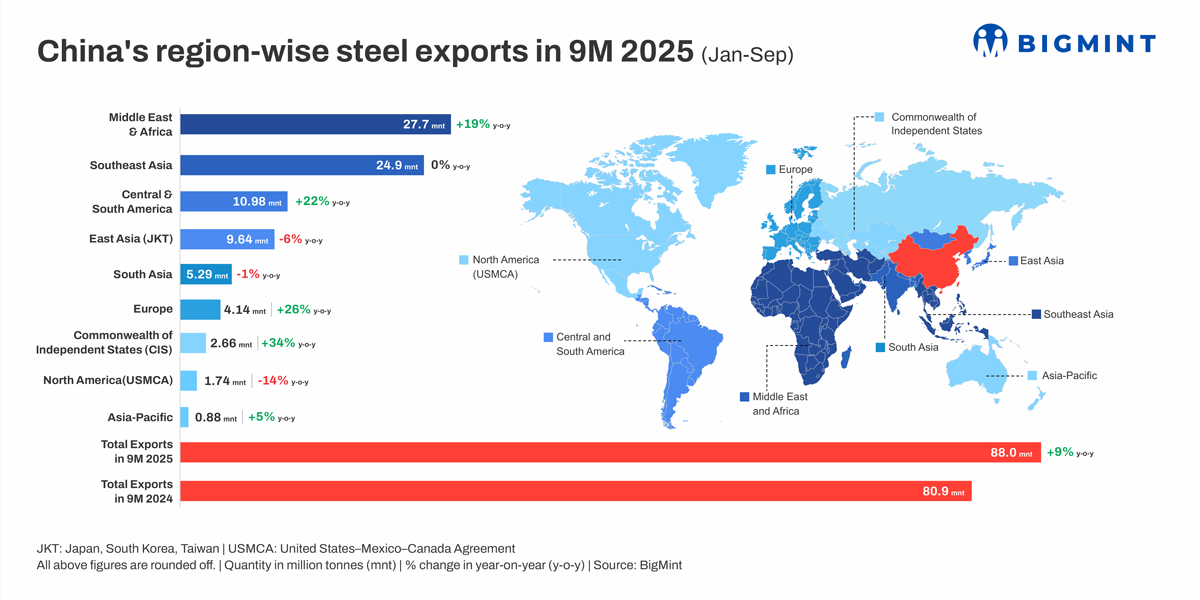

Region-wise steel exports

The MENA region remained the topmost destination for Chinese steel in 9MCY’25, with total shipments of around 27.6 mnt, an increase of 20% y-o-y. The UAE and Saudi Arabia witnessed steady growth in imports from China, while shipments to Turkiye dropped 7% y-o-y in 9MCY’25.

China’s exports to the Southeast Asian nations remained flat on the year at around 25 mnt. The highlight was, of course, the 25% decline in shipments to Vietnam following an anti-dumping duty imposed on flat-rolled imports. Exports to Philippines and Indonesia increased by 12% and 3%, respectively, despite both countries imposing import tariffs on Chinese steel.

At around 11 mnt, steel exports to Central and South America witnessed a sharp growth of 22% y-o-y in 9MCY’25. Peru, Chile and Ecuador saw the steepest rise in imports from China, while Brazil, the largest importer in the continent, reduced imports from China by 8% on the year.

Exports to East Asia (9.64 mnt) dropped 6% y-o-y in 9MCY’25. Imports by South Korea (5.7 mnt) slid by 9%, while Taiwan saw a massive decline of 40% y-o-y. Both countries have anti-dumping duties on certain Chinese products.

Exports to South Asia (5.29 mnt) edged down by 1% y-o-y. Pakistan (2.33 mnt, +26%) was the highest importer, while India (1.62 mnt, -31% and Bangladesh (0.81 mnt, +16%) trailed.

Even as Chinese shipments to India declined sharply due to the safeguard duty, exports to Europe increased by 26% y-o-y during the review period as buyers rushed to restock ahead of CBAM coming into force from January 2026.

Shipments to the CIS nations (2.66 mnt) rose 34% in 9MCY’25, with data suggesting that this region has emerged as a new landing place for Chinese exports. Kazakhstan, Uzbekistan, Kyrgyzstan, and Tajikistan have registered steep growth in imports from China.

On the other hand, exports to North America (1.75 mnt) dropped by 14% y-o-y in 9MCY’25.

Outlook

Analysts suggest that exports will hit a new peak in 2025, with protectionist backlash forcing commodity and geographical diversification rather than restraint. Also, semi-finished, rebar, and wire rod exports have surged manifold.

At a 10% annual growth rate, China’s exports are supposed to exceed the 120-mnt mark in 2025. The backlash is also evident as over 80 countries have imposed tariff and duty walls in response to China’s aggressive exports. With the WSA predicting continued demand weakness in China, and softer-than-expected stimulus measures by the Chinese government, it may be expected that exports will remain elevated going forward.

Leave a Reply