- Sharp alumina output drop reported in South & North America

- Kwinana refinery closure impacts overall regional capacity

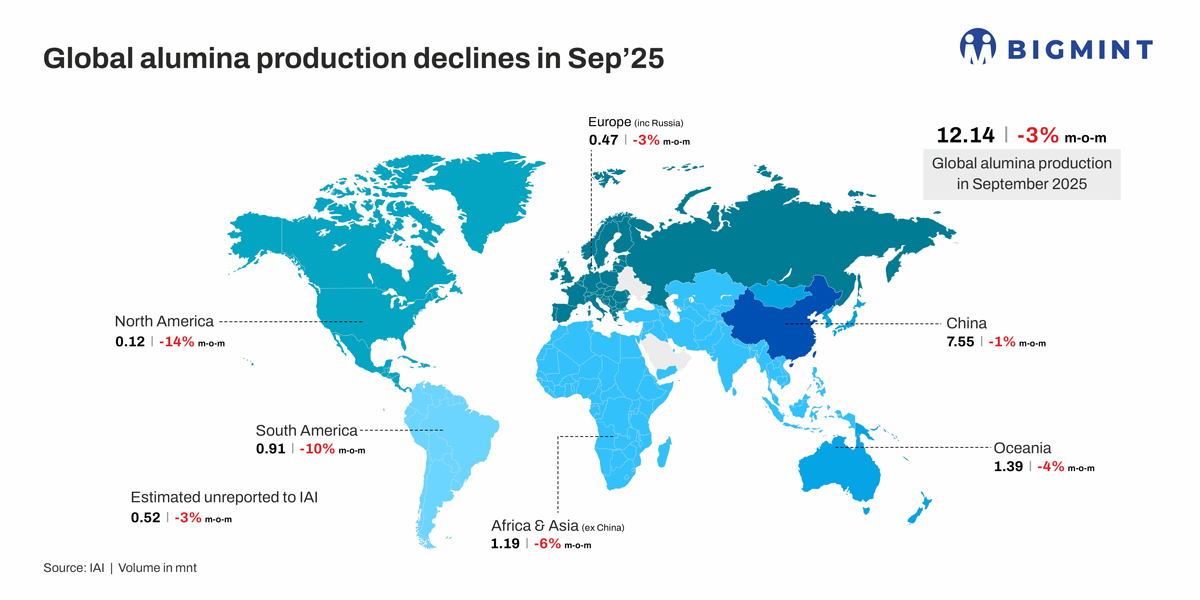

Global metallurgical alumina production declined 3% month-on-month (m-o-m) to 12.14 million tonnes (mnt) in September 2025, from 12.51 mnt in August, according to the International Aluminium Institute (IAI). The decrease was primarily attributed to maintenance-related slowdowns and energy constraints affecting major producing regions.

Despite the monthly dip, cumulative alumina output for January-September 2025 stood at 111.59 mnt, up 3% from 107.93 mnt in the same period last year, indicating sustained refinery performance through most of the year.

Country-wise breakdown

China, the world’s largest alumina producer, saw output ease by 1% to 7.55 mnt from 7.63 mnt in August, reflecting minor slowdowns in refinery operations due to power rationing and regional maintenance activities. Despite this dip, China continued to account for over 60% of global supply.

Oceania’s production fell 4% to 1.39 mnt, largely impacted by scheduled maintenance at key refineries in Australia. Africa and Asia (excluding China) witnessed a sharper 6% contraction to 1.19 mnt as several refineries in India and the Middle East faced lower throughput rates amid energy and logistics constraints.

South America recorded the steepest regional decline of 10%, producing 0.91 mnt compared with 1.01 mnt in August, as refinery disruptions in Brazil limited output.

Europe (including Russia) and North America also reported declines of 3% and 14%, respectively, with North America’s output falling to 0.12 mnt due to reduced plant utilization.

Alumina output unreported to IAI was estimated at 0.52 mnt, down 3% from the prior month.

Global alumina supply dips as refineries face disruptions

China, the world’s largest alumina producer, saw output ease as several refineries in Shanxi and Henan undertook maintenance work and operated under power rationing during the late monsoon season. Although metallurgical-grade alumina production in China increased slightly m-o-m, growth was constrained by periodic reductions in roasting furnace loads at northern refineries during the “September 3rd military parade” and routine maintenance at southern plants. Falling alumina prices narrowed profit margins, limiting producer enthusiasm for higher output, yet China continued to dominate the global alumina market, accounting for over 60% of total supply.

In Oceania, production declined amid scheduled maintenance and reduced run-rates at key Australian refineries, compounded by the permanent closure of Alcoa’s Kwinana refinery due to high operating costs and ageing infrastructure, gradually reducing overall refining capacity.

Africa and Asia (excluding China) registered lower output as refineries in India and the Middle East faced energy and logistics constraints and weaker bauxite supply, which disrupted feedstock availability for several plants.

South American alumina production fell mainly due to operational disruptions in Brazil, where integrated bauxite and alumina operations experienced maintenance-related slowdowns.

Europe (including Russia) saw a moderate decline driven by high energy prices and elevated production costs, while North America’s output dropped amid reduced plant utilization and unfavourable market economics.

The overall global decline underscores persistent structural challenges in the alumina industry, including rising power costs, refinery maintenance cycles, and bauxite supply disruptions, even as long-term demand from the aluminium sector remains firm.

Outlook

Global alumina production is expected to remain under pressure in the near term as refineries continue routine maintenance and face high energy costs. Structural challenges such as bauxite supply constraints and ageing infrastructure, particularly in Oceania and South America, may further limit output.

In China, production is likely to stay stable but sensitive to regional events and profit margins, while demand from the aluminium sector should continue supporting overall refinery activity. Overall, the market may see modest supply adjustments, with prices and operating rates gradually stabilising in the coming months.

Leave a Reply