- India ranks 3rd globally in stainless steel output

- China’s crude stainless steel output up 3% y-o-y

The 10th APAC Ni-Cr-Mn Stainless Steel and New Energy Conference 2025, hosted by SMM Information and Technology Co., Ltd. and held on 20-21 October in Xiamen, Fujian, brought together global experts and industry leaders to discuss market trends, innovation, and supply chain challenges. Centred around the theme “Exploring Development Directions and Solving Industry Challenges Together,” the conference provided a practical platform for in-depth discussions on market dynamics, technological breakthroughs, and emerging industry trends.

The current industry dynamics in China, reflecting a sharp fall in imports; India’s strong growth story, with consumption growth at around 8%; and evolving raw material market trends were among the various aspects discussed during the conference.

Current status of China’s stainless steel industry

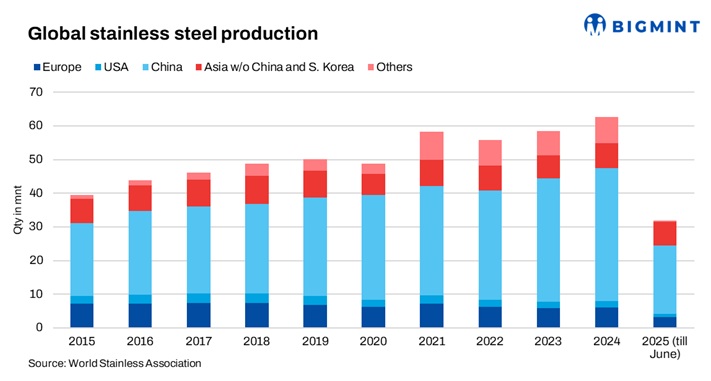

China’s crude stainless steel production in January-October 2025 reached approximately 32.49 million tonnes (mnt), up 3.01% y-o-y, with a projected total of 41-41.5 mnt for 2025.

In January-August 2025, China’s stainless steel imports stood at approximately 1.02 mnt, reflecting a sharp decrease of 23.32% y-o-y, with lower exports from Indonesia being the primary contributor to this decline.

Meanwhile, stainless steel exports during the same period rose modestly by 3.09% y-o-y to around 3.36 mnt, with major markets being Vietnam, Russia, Turkiye, and South Korea. Net exports increased significantly by 21.19% y-o-y to 1.67 mnt, indicating a strengthening export position despite lowered import volumes.

India’s growth story, future outlook

India’s stainless steel sector recorded strong momentum in 2024, with melt shop production rising over 7%. This solidified its position as the world’s third-largest producer after China and Indonesia. Stainless steel consumption also grew nearly 8% to around 4.8 mnt in FY’25, supported by rising demand from infrastructure, construction, railways, and process industries.

The 300-series segment saw significant expansion, while the 200-series continued to dominate applications in utensils, pipes, and tubes. Meanwhile, the 400-series gained traction in railways and structural applications. The ABC (architecture, building, and construction) sector surged by over 12%, reflecting India’s accelerating industrial growth and vast potential for further stainless steel market development.

Indonesian production trends

Indonesia’s stainless steel production during January-October 2025 was about 4.16 mnt, down 0.49% y-o-y, with output forecast to rise to around 5.1 mnt by year-end, driven by increased output from major players such as Tsingshan and Jindalai.

Raw material market insights

Raw materials remain critical to the stainless steel sector. Nickel continues to serve as the largest alloying metal, with consumption rising rapidly, especially in battery manufacturing and new energy applications.

China’s production of high-carbon ferro chrome reached 6.54 mnt in January-September 2025, marking a y-o-y decrease of 192,700 t. Total capacity for 2025 stood at 15.61 mnt, with an additional 600,000 t expected in Q4. Inner Mongolia led production with 5 mnt, up 431,800 t y-o-y, accounting for 76.5% of national output.

China remains the world’s largest molybdenum producer, accounting for 47.7% of global output in 2024 with 138,000 t of concentrate. However, environmental checks, low ore grades, and rising costs have slowed growth. In 2025, production is expected to reach 143,000 t (metal content), up 3.4% y-o-y, while global supply rises only 1.9%.

Outlook

The Asian stainless steel market is entering a phase of strategic rebalancing — with China maintaining dominance through strong exports, India accelerating domestic consumption growth, and Indonesia expanding production capacity. Rising demand from the green energy and EV sectors will continue to shape raw material markets, while supply chain realignments and decarbonization efforts redefine trade patterns into 2026.

Leave a Reply