- Only 12% of low-emissions facilities announced till CY’23

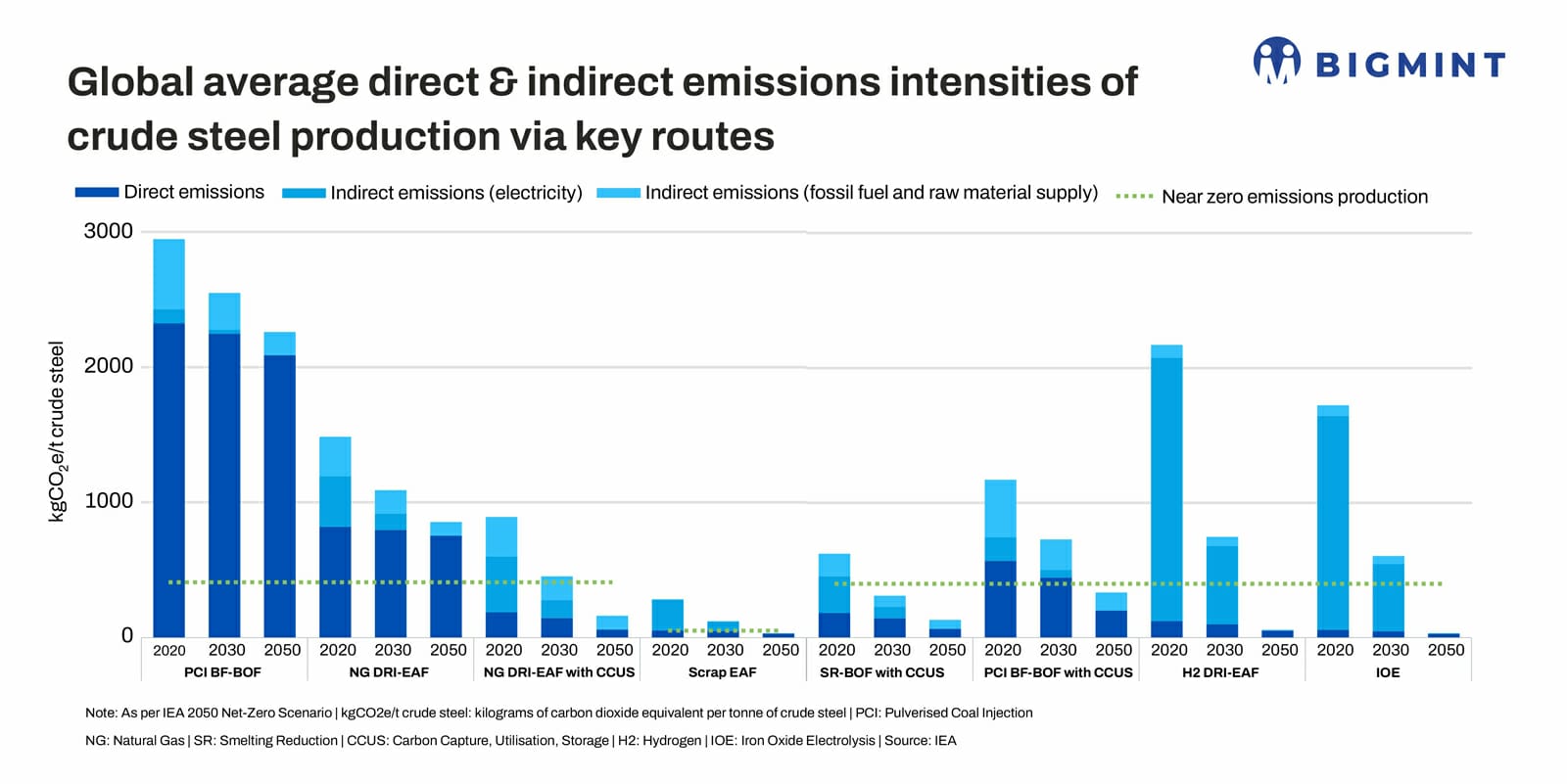

- All conventional technologies fall short of IEA’s near-zero target

- Scrap will provide just 50% of metallic inputs to steelmaking by CY’50

Morning Brief: Scientists from the University of Technology Sydney (UTS) have developed energy-related carbon budgets for industries including the aluminum, steel and chemical industries as well as automobile and aviation. The global carbon budget to limit global warming to +1.5°C with 67% certainty is 400 Gt CO2 (gigatonnes of CO2) until 2050. The steel industry would have a share of 19 Gt CO2 remaining, which is 5 of the total budget.

For perspective, the steel industry emits over 2.5 Gt annually, which means that the budget will be exhausted long before 2050 unless some immediate intervention reverses the order of things.

In this context, it is important to note that the global steel industry’s emissions intensity has remained relatively flat over the past few decades. According to the International Energy Agency (IEA), “Whilst there are nascent signs of a transformation to low and near zero emissions production, the pipeline of announced projects is still far too low compared to what is required under the IEA’s Net Zero Emissions by 2050 Scenario (NZE Scenario). As of 2023, announced projects meet just 12% of 2030 near zero emissions iron production needs.”

Defining near-zero emissions steel

The IEA has proposed some principles for defining near-zero emissions steel. These include:

- Agreeing a clear purpose for the use of the definition. Providing a common vision of a final destination for steel production in a net zero future energy system to help guide investment decisions and policy support.

- Remain technology and route agnostic, to allow for different country and company contexts.

- Thresholds should be stable, absolute and ambitious, to help build trust among users. The threshold values proposed in the IEA report for steel production are 50-400 kg of CO2 equivalent per tonne (kg CO2-eq/t), with the precise values depending on the amount of scrap used. The thresholds for near zero emissions production outlined in the IEA report4 target levels of emissions intensity that are compatible with reaching net zero emissions from the global energy system by mid-century.

- Consider globally recognised and commonly understood sets of definitions, which then can be used in different ways within different national contexts, according to national policy objectives.

Scrap dilemma

The IEA and other global bodies such as the SBTi are seeking to create a near-zero emissions steel threshold based on the full spectrum of scrap usage. It has also been emphasised that the remaining CO2 budget should be rationally distributed among the different steel production routes, with the fundamental yardstick being the percentage of scrap in total production. Thresholds are set with an eye on scrap in production.

According to the IEA, despite a strong push on material efficiency strategies resulting in increased scrap use and reducing total growth in steel demand, scrap only provides about half the metallic inputs to steel production globally in 2050 in the NZE Scenario. Scrap-based production alone is not sufficient to achieve the emissions reductions needed for the steel sector in the NZE Scenario.

A progressive near zero emission threshold based on the scrap share reflects limits on scrap availability and the difficulty of abating emissions from the iron production required.

Moreover, as per IEA, emerging market economies have a lower scrap share of metallic inputs on average, given that their stocks of steel in society are younger, and so there is comparatively less end-of-life scrap becoming available for use. The IEA’s higher near zero emissions threshold for iron-based production helps to avoid penalising countries that simply do not have as much scrap available due to their stage of development.

Additionally, if a progressive threshold were not used, there would be a higher likelihood of causing unintentional distortions in scrap market prices, as producers seek to buy up scrap as a considerably easier way to achieve near zero emissions.

Technology routes & near-zero

As the graphic on top shows, conventional production technologies – including production based on blast furnaces, coal-based direct reduced iron, and gas-based direct reduced iron – fall well short of achieving near zero emissions production. The exception being the scrap electric arc furnace route, for which the majority of indirect emissions stem from electricity generation.

Note that production via coal-based direct reduced iron – which is not shown in the figure but is a prominent route in India – has roughly comparable emissions to production via the blast furnace-basic oxygen furnace with pulverised coal injection route.

For innovative production technologies, hydrogen and direct electrification achieve the lowest emissions intensities once the electricity sector is decarbonised. Carbon capture, utilisation and storage (CCUS)-equipped routes lead to immediate reductions in direct emissions, with the smelting reduction with basic oxygen furnace route reaching near zero emissions by 2030 under the NZE Scenario.

Leave a Reply