- Energy costs, maintenance schedules cap output globally

- Tight inventories support higher aluminium market prices

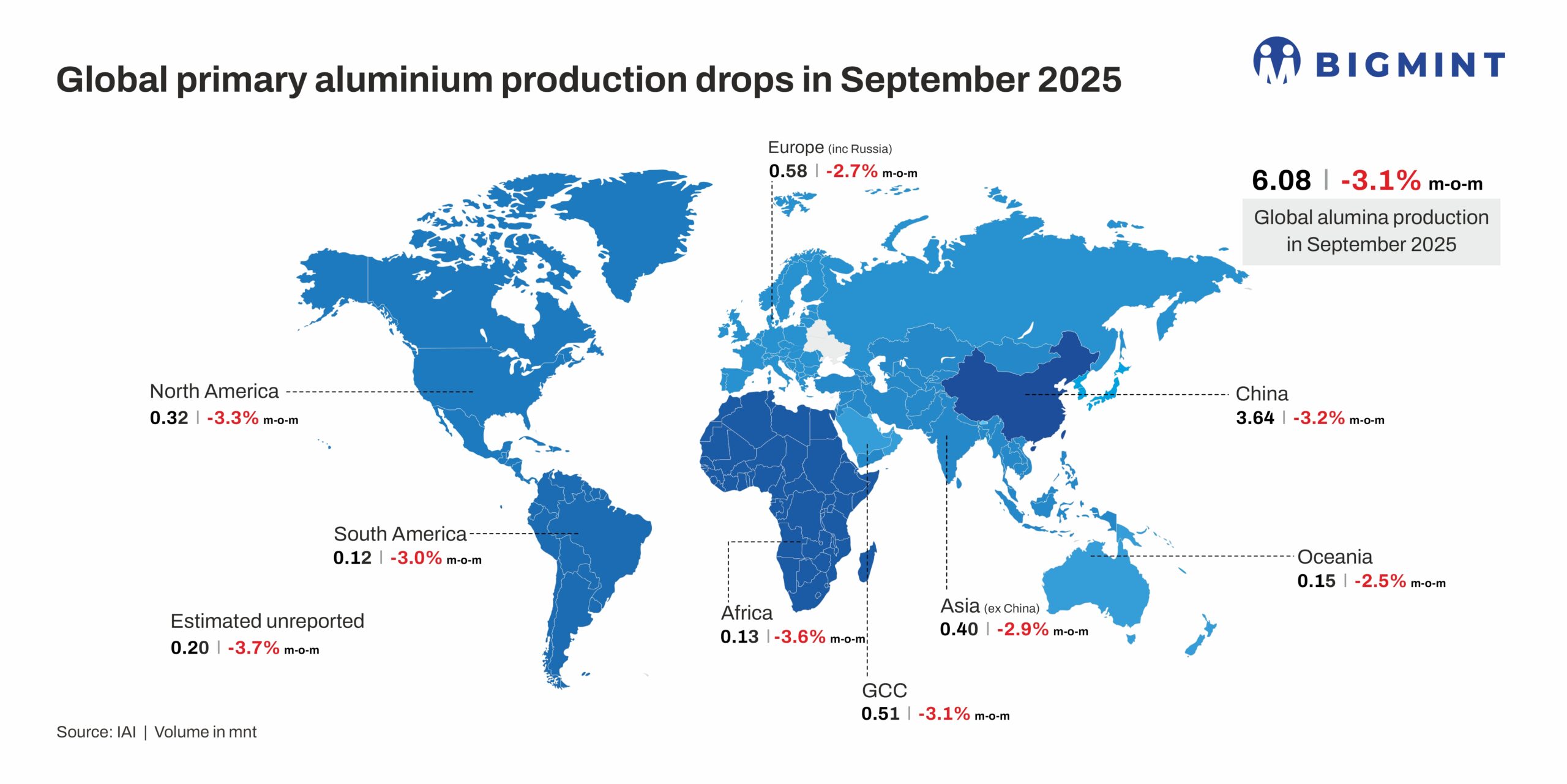

Global primary aluminium production in September 2025 stood at 6.08 million tonnes (mnt), down 3.1% m-o-m from 6.28 mnt in August. The fall reflects weaker output across major producing regions amid operational slowdowns and market adjustments.

Meanwhile, global aluminium production in 9MCY’25 reached 55.136 mnt, compared with 54.277 mnt in 9MCY’24, representing a 1.6% y-o-y increase, indicating steady growth on a cumulative basis despite the monthly dip.

Country-wise breakdown

China, the largest producer, recorded a 3.2% m-o-m fall to 3.64 mnt, maintaining its lead in global supply. Africa registered a 3.6% m-o-m drop to 0.13 mnt, while South America slipped 3.0% m-o-m to 0.128 mnt.

North American output decreased 3.3% m-o-m to 0.32 mnt, and Asia (excluding China) dipped 2.9% m-o-m to 0.40 mnt. Europe (including Russia) production contracted 2.7% m-o-m to 0.58 mnt, while Oceania edged down 2.5% m-o-m to 0.156 mnt. The GCC region also saw a 3.1% m-o-m reduction to 0.51 mnt, and estimated unreported output slipped 3.7% m-o-m to 0.206 mnt.

Overall, global aluminium production witnessed a uniform m-o-m decline across regions, reflecting operational moderation and seasonal adjustments in September 2025.

China, the world’s largest aluminium producer, witnessed a drop in September production to 3.644 mnt from 3.764 mnt in August. This reduction aligns with the government’s implementation of production caps to manage energy consumption and environmental impact, leading to tighter supply in the global market.

Why did global aluminium output drop in Sep’25?

Global primary aluminium production declined in September 2025 due to a combination of policy, operational, market, and seasonal factors.

In China, government-enforced production caps aimed at controlling energy consumption and reducing carbon emissions, along with seasonal maintenance in regions such as Inner Mongolia and Yunnan, limited output. Weaker export demand also contributed to the reduction, with China’s production falling from 3.764 mnt in August to 3.64 mnt in September. Given that China accounts for over half of global aluminium production, these adjustments had a significant impact on worldwide supply.

Rising energy costs further constrained production, particularly in North America and Europe, where electricity prices for industrial use in the US increased to 9.29 cents per kilowatt-hour in July 2025 from 8.75 cents the previous year. Energy variability, environmental regulations, and regional hydropower constraints forced smelters in higher-cost regions to operate at reduced capacity or schedule downtime. Weak demand from downstream sectors such as automotive, construction, packaging, and manufacturing, coupled with high inventory levels in several regions, reduced operational incentives, prompting producers to scale back output. Seasonal maintenance and end-of-season curtailments during September also reinforced the slowdown.

Market and trade dynamics further influenced production trends. Tight visible inventories on the London Metal Exchange (LME) and dominant positions by large traders limited near-term supply, creating backwardation and encouraging producers to throttle output strategically rather than risk overproduction. Benchmark aluminium prices rose sharply due to these tight stocks and strong market sentiment, but higher input costs and rising energy expenses meant many producers prioritised profitability over volume expansion. Shifts in global trade flows, including decreasing exports of semi-finished aluminium and rerouted volumes from regions such as Russia, disrupted regional availability and added further pressure on production.

Feedstock trends also played a role, with declining alumina prices in some regions reflecting weaker smelter demand and prompting temporary slowdowns. Maintenance and efficiency upgrades in Africa, the GCC, and other regions contributed to reduced output, reinforcing the overall decline. Collectively, these factors — policy restrictions, rising energy and input costs, weak downstream demand, tight inventories, trade disruptions, and seasonal adjustments — drove the 3.1% m-o-m fall in global primary aluminium production from 6.28 mnt in August to 6.08 mnt in September 2025.

Outlook

Global aluminium output is expected to remain subdued in October 2025, as seasonal maintenance, high energy costs, and policy-driven production caps in China continue to constrain supply. Weak downstream demand and tight inventories may limit operational increases, while market prices and trade adjustments could encourage producers to prioritise profitability over volume, keeping output near September levels.

Leave a Reply