- Crude steel production plunges to 21-month low

- Domestic supply glut continues to propel steel exports

- Incentives, trade-in policy subsidies spur auto sector

Morning Brief: China’s macroeconomic indicators continued to signal lacklustre momentum in the country’s steel industry in September 2025.

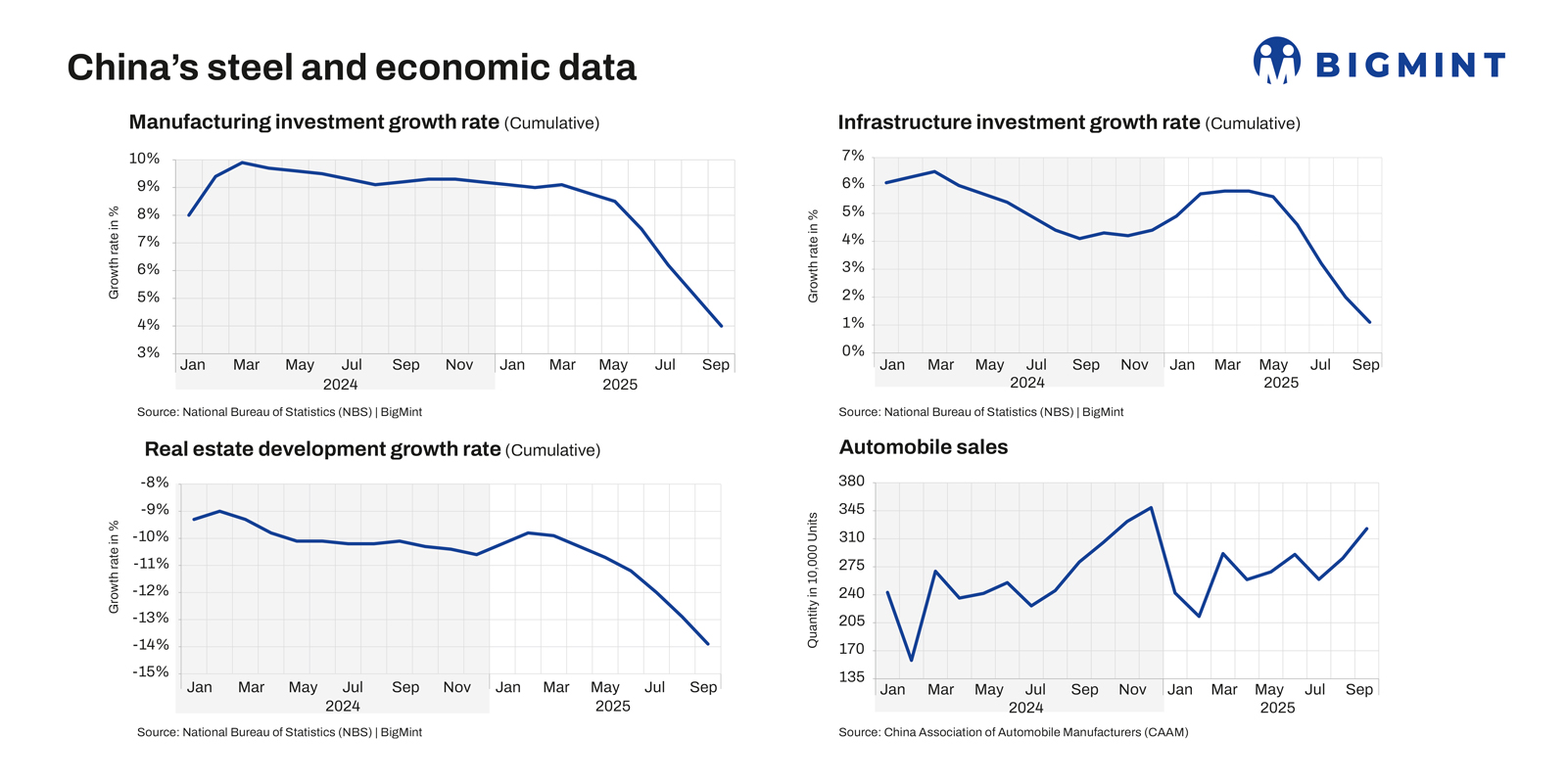

Latest data from the National Bureau of Statistics reveals that investment growth in the infrastructure sector plummeted to 1.1% in January-September 2025, while the same for the manufacturing segment slipped to 4.0%. Real estate development growth remained negative, at -13.9%. All three are at their lowest in over two years, suggesting that demand weakness may persist in the medium term.

Fixed asset investment growth, tracking the real estate, infrastructure, and manufacturing segments and accounting for over 40% of its GDP, was at -0.5%, the weakest in over five years.

These line up with worldsteel’s recent projection of a 2.0% drop in Chinese steel consumption in CY’25. Moreover, consumption is set to further moderate in CY’26, though by a lower by 1.0%.

Highlights of China’s steel industry in Sep’25

Crude steel production plunges to 21-month low

Crude steel production remained below 80 million tonnes (mnt) for the third consecutive month, with volumes edging down by 5.0% y-o-y to 73.49 mnt.

This marks a 21-month low, attributed to the following factors: (1) operation suspensions at certain mills ahead of the military parade on 3 September, (2) shrinking profitability of steelmakers amid declining product prices and firm raw material costs, and (3) weaker demand than expected during the peak season.

Meanwhile, pig iron output declined by 5.4% y-o-y to 66.05 mnt in September.

Steel exports continue uptrend

September steel exports were up 10% m-o-m to 10.47 mnt, the highest in four months. A domestic supply glut compelled steelmakers to direct material overseas, with volumes rapidly accelerating due to aggressive price undercutting.

Adverse weather, including Typhoon Ragasa, disrupted logistics and construction activity, while restocking momentum remained soft ahead of the Golden Week holidays (1-8 October).

Iron ore imports rise as peak steel season arrives

Iron ore imports increased 10.6% m-o-m to 116.22 mnt as demand strengthened in alignment with a modest increase in infrastructure orders. Expectations of improved market activity during the peak steel season also drove up steelmakers production enthusiasm and, consequently, iron ore demand. Additionally, global miners boosted shipments to take advantage of iron ore prices remaining above $100/tonne (t).

Coal production, imports climb up m-o-m

Coal production stood at 411.51 mnt, rising 5.4% m-o-m but dipping by 1.8% y-o-y. The resumption of mining activities following the military parade could have led to higher production m-o-m.

Meanwhile, stricter safety checks in key production hubs, operational disruptions due to flooding, a drop in thermal power generation amid rainy weather, and an increase in hydroelectric generation impacted coal production and consumption, leading to a slight drop y-oy.

However, imports diverged from this trend, reflecting a 7.64% increase m-o-m. Pre-holiday restocking and expectations of higher industrial activity are likely to have boosted imports.

Cement production continues to slide

The y-o-y fall in China’s cement production sharpened to 5.2% over January-September (1,259.36 mnt) compared to 4.8% in January-August (1,104.57 mnt). The long-persisting downturn in China’s property sector contributed to the deeper fall. Additionally, the cement industry has been aiming for production discipline due to overcapacity concerns.

Auto production, sales in high gear

Auto production totalled 3.276 million units in September, up 16.4% m-o-m. Meanwhile, sales stood at 3.226 million units, up 12.9% m-o-m.

Auto sales accelerated in September, aided by incentives such as trade-in subsidies. Fears regarding the potential discontinuation of some of these programmes — due to limited funding with local administrations — also likely prompted a rush among buyers.

However, rising sales and production may not necessarily be a sign for cheer, as price competition has severely narrowed profit margins of automakers. This has likely been a drag on steel market activity.

Construction woes continue as investment growth slides

Bearish trends emerged in construction-related macro indicators. Infrastructure investment growth decelerated to 1.1% in January-September compared to the 4.6-5.8% rate seen in various months in the first half of the year.

Real estate development growth declined by one percentage point to -13.9%. New home prices fell 0.41% m-o-m, the sharpest drop this year, returning to 2019 values.

The steady decline in prices has undermined households confidence regarding new home purchases.

Manufacturing activity weakens amid US-China trade war

Manufacturing investment growth slowed to 4.0% in January-September, with the rate peaking at 9.0-9.1% in January-March. While manufacturing showed the strongest growth among end-user sectors, buoyed by a thriving automotive industry, it continued to be highly vulnerable to US-China trade frictions.

China’s official manufacturing purchasing managers index (PMI) remained below the expansion mark for the sixth month, at 49.8 points in September. Domestic demand was tepid, while trade tensions affected exports.

Outlook

All eyes are on China’s fourth plenum, which is expected to lay down the roadmap for the next 2026-2030 Five-Year Plan. Market participants are hoping for concrete consumption-boosting programmes to restore growth momentum. A potential Xi-Trump meeting next week is also expected to shed light on how US-China relations will evolve and whether a cessation in the tariff war can be brought about.

Additionally, several infrastructure development plans are expected to be actioned in this quarter, prompted by waning export demand and the tariff war.

China has also announced policy-based financial instrument with a corpus of RMB 500 billion to channel funds into national projects and, thereby, advance investment growth.

Only time will tell if these initiatives succeed in reviving China’s steel industry. For now, with the approach of winter, traditionally a sluggish period, prospects of industry growth appear to be limited.

Leave a Reply