- Construction, manufacturing demand expected to improve

- Market hopes for stimulus boosters from Fourth Plenum

- High steel inventories, approaching winter may dent demand

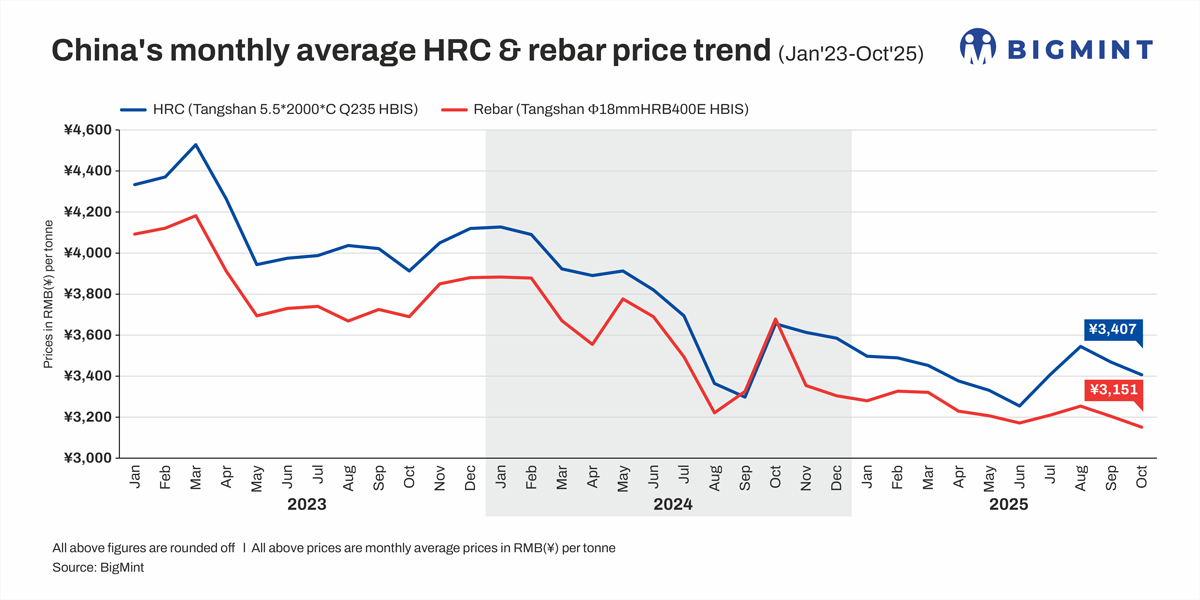

Morning Brief: Chinese steel prices weakened in early October 2025, extending the downtrend seen in September. Elevated inventories, following the trading lull during the National Day and Mid-Autumn Festival holidays, weighed on prices, while demand remained inadequate. However, strong cost support from raw material tags helped limit the price corrections.

Tangshan’s benchmark hot-rolled coil (HRC) prices averaged RMB 3,407/tonne (t) ($478/t) till 16 October, down by RMB 61/t ($9/t) from September’s monthly average of RMB 3,468/t ($487/t). Similarly, rebars stood at an average of RMB 3,151/t ($442/t) in early October, down by RMB 53 ($7/t) from September’s RMB 3,204/t ($450/t).

Despite the continued decline, market participants are hopeful of a slight price uptick in October, supported by policy measures and healthier fundamentals. However, this optimism has been tempered by the approach of winter, which is likely to dampen construction activity, and the threat of further escalations in trade frictions.

Factors influencing steel prices in Oct’25

Construction, manufacturing demand set to improve: Demand for construction steel is likely to recover in October, with the retreat of summer, which was marked by scorching heat and heavy rainfall. Major infrastructure projects have been initiated, as per reports. According to Mysteel, home appliance manufacturers have also raised their production targets for the month, which is likely to lift flat steel demand, though at a sedate pace.

Supply contraction likely as profits thin: While finished steel prices declined in September, raw material tags remained firm. Narrowing profit margins are likely to cool steelmakers’ production enthusiasm, which may tighten supply.

However, Mysteel projects that HRC supply may continue to exceed demand. Shrinking rebar profits have pushed mills to produce HRCs, which offer better margins and can help keep production momentum steady.

Additionally, an 8% increase in steel inventories following the Golden Week holiday (compared to end-September) and sluggish drawdown may weigh on prices.

Macroeconomic expectations lift market confidence: The Fourth Plenary Session of the 20th Communist Party of China (CPC) Central Committee will take place in Beijing over 20-23 October. The discussion is set to revolve around the country’s 15th five-year plan, laying down its framework, key priorities, and the policy roadmap. The market remains optimistic that the plan will include some booster shots to lift steel demand.

Input costs may remain resilient: Cost support may continue from raw material tags, preventing a sharp fall in steel prices. Iron ore, coking coal, and coke have remained relatively stable so far in early October compared to the monthly averages of September. For coking coal in particular, stringent checks on safety and production rates may constrain supply. However, iron ore may face pressure due to the build-up of steel inventories.

End of peak season may dent demand: Among the factors that may exert downward pressure on prices is the end of the peak season and the approach of winter. Construction activity is likely to subside again in winter, and if production continues to surpass demand, prices may erode. However, HRCs may remain supported on demand from the manufacturing segment, though the outlook remains soft.

Global trade tensions to hang over market: Recent weeks have seen an escalation in tensions with major economies. For example, the EU has proposed to halve its steel import quotas, while Trump imposed a 25% tariff on imported trucks and components, effective 1 November. He threatened to impose a 100% tariff on Chinese goods, though he tried to play it down later.

These escalations in trade tensions are expected to cast a shadow over trading activity, but sharp declines in prices may be limited, as the market will likely be able to weather such shocks. Negotiations are also underway between US and China, with Xi and Trump expected to meet during the Asia-Pacific Economic Cooperation summit.

Exports will continue at a resilient pace as an outlet for surplus domestic supply. The global manufacturing purchasing managers’ index (PMI) remained in expansion territory at 50.8 points in September, though it edged down from August’s 50.9, signalling moderate demand overseas.

Outlook

Overall, October is expected to end with stability or a slight weakness in terms of pricing. Macroeconomic developments are expected to induce a mild rebound, with some support from improved market fundamentals. However, it is important to note that if the stimulus packages or policy measures fall short of expectations and steel inventories remain elevated, prices are unlikely to recover.

Leave a Reply