- Market caution continues amid global macro uncertainties

- Expectations of Fed rate cut offer limited short-term support

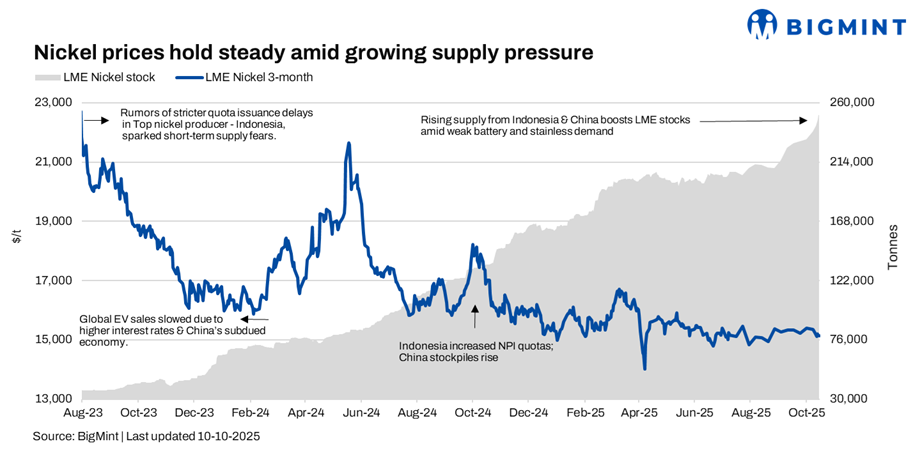

Nickel futures on the London Metal Exchange (LME) experienced a modest downturn this week, with three-month contracts settling at $15,130/t on 17 October, down $225/t w-o-w from $15,355/t the previous week. The decline reflects a combination of rising inventories, softening downstream demand, and continued market caution amid global macro uncertainties.

During the same period, LME warehouse stocks increased steadily to 250,530 t from 231,654 t, indicating that the market continued to grapple with a comfortable near-term supply situation. The inventory build suggests that offtake from key end-use sectors, particularly stainless steel and nickel pig iron (NPI) producers, remains moderate, limiting the potential for a sustained price recovery.

The price weakness aligns with broader fundamental pressures in the nickel market. While Indonesia’s nickel ore output continues to rise and seasonal production adjustments in China provide limited cost support, the oversupply in global markets keeps the market in check. The International Nickel Study Group (INSG) forecasts a persistent surplus for 2025, which is consistent with rising warehouse inventories and pressure on LME prices to hover near the $15,000/t mark.

On the demand side, although electric vehicle (EV) battery production continues to grow, its immediate impact on nickel demand is constrained. Stainless steel, which accounts for roughly 65-70% of global nickel consumption, remains the primary driver of demand. Weak downstream orders, combined with ongoing trade uncertainties between China and major economies, contributed to muted buying activity in both the futures and spot markets.

Global macro factors also weighed on sentiment. Escalating Sino-US trade tensions, potential tariffs on Chinese goods, and volatile energy and currency markets have reinforced risk-off positioning in base metals. Meanwhile, expectations of a US Federal Reserve interest rate cut provided limited short-term support, as slowing industrial growth and weak manufacturing data in Europe and the US continued to weigh on metal demand.

Outlook

Nickel prices are likely to remain range-bound in the short term, with support coming from high-cost production limits in Indonesia and China, but upside is likely to be constrained by inventory overhang and sluggish end-user demand. Any significant shift in global supply policy, export controls, or a pick-up in stainless steel production could temporarily tighten the market, but the near-term tone remains bearish-to-neutral.

Leave a Reply