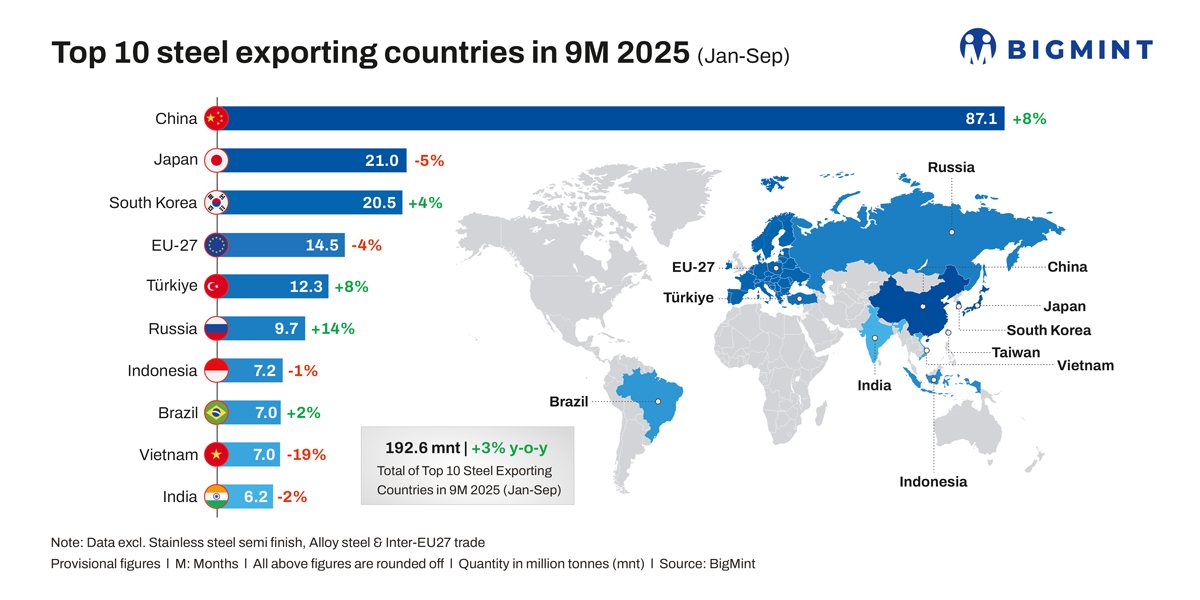

- Total shipments by top 10 exporting countries rise by 3%

- Chinese steel exports may rise by 8-10% y-o-y in CY’25

- Russia ramps up exports by subverting Western sanctions

Morning Brief: The top ten global steel exporting countries were able to lift steel shipments by 3% in the first nine months of 2025 (9MCY’25) despite trade wars and tariff-related turmoil which upended global markets. Total steel exports by the top 10 countries were around 184 million tonnes (mnt) in January-September — over 10% of global steel demand of around 1,800 mnt in 2024. This marks a slight increase from the 178.37 mnt recorded in the year-ago period.

China continued to show robust growth as the world’s leading steel exporter, although that growth was not replicated in steel production in 2025 in which China, again, holds the world’s top spot. The combined share of the top three exporters – China, Japan and South Korea – was roughly 70% of global steel exports in 9MCY’25, with China accounting for around 47% of global exports. Notably, despite the negative impact of US tariffs and trade wars, decline in demand in the advanced economies and global manufacturing contraction, some of the other leading steel-exporting countries such as Brazil, Russia, and Türkiye were able to ramp up exports.

Top steel-exporting countries

China: China’s total exports of steel in 9MCY’25 was recorded at over 87 mnt, an increase of 8% y-o-y. Chinese steelmakers have been forced to offload goods overseas to alleviate the supply pressure in the domestic market. US-China tariff tensions have also driven aggressive front-loading, and expectations are that China will close the year with robust export growth y-o-y, reaching a new peak.

There have been some significant shifts in export flows, with several traditional markets adopting protectionist measures to safeguard their domestic industries. As such, Chinese exporters were compelled to redirect shipments to other geographies, particularly to the Middle East and Africa, Southeast Asia and South America.

Japan, South Korea, Taiwan (JKT): In sync with a drop in crude steel production, Japanese steel exports dropped 5% y-o-y in 9MCY’25. As per METI forecasts, exports may fall by over 6% in Q4CY’25. The construction sector continues to suffer labour shortages and rising material raw material costs, the auto sector lacks demand momentum. Exports may decrease as steelmakers lose market share in China where EV adoption is growing fast, as well as US tariffs, EU quota system, and anti-dumping probes by many countries.

South Korea, on the other hand, recorded a 4% y-o-y growth in steel exports in 9MCY’25 mainly due to front-loading of shipments ahead of the implementation of US tariffs pegged at a uniform 50% for steel and aluminium for all countries. However, the EU’s slashing of import quotas and raising tariffs to 50% for imports beyond quota volumes pose a direct threat to Korean exports.

Taiwanese exports fell a sharp 10% y-o-y on weak demand in key geographies such as the EU, growing exports by China, which affected JKT in general, and US tariffs. However, India’s exemption of BIS curbs for some mills has opened a window for Taiwanese exporters.

Turkiye, Russia: Turkish exports, especially of long steel products, increased y-o-y in 2025, with total steel exports recording a gain of 8%. Turkish exporters to traditional markets such as Syria increased due to post-war reconstruction efforts in that country, as well as other markets such as Yemen, although shipments to Israel dropped over diplomatic and political stand-off. US tariffs, economic and currency instability and weak EU demand, however, pressured exports.

Russia, on the other hand, ramped up steel exports by 14% y-o-y in 9MCY’25. Sanctions by Western countries significantly limited exports of Russian steel products. This led to a reorientation towards the domestic market and the markets of “friendly” countries. At the same time, the practice of offering price discounts of 15-30% was used to expand presence. Despite the sanctions, Russian steel exports remain significant, mainly due to demand in countries that did not impose them and the absence of a complete ban on imports of Russian semi-finished products in the EU.

Brazil, Vietnam, India: Although Brazil recorded a marginal increase in steel exports during the review period, US tariffs and continuing import assault from China remain major threats. The US was Brazil’s top steel buyer in 2024. However, Brazil’s steelmakers are more concerned about rising Chinese imports. Despite Brazil imposing a 25% tariff on 11 steel products in 2024, the imports still hit record highs; almost 70% of imports were from China.

India’s exports fell marginally y-o-y due to trade wars and uncertainties, strong competition from China and growing trade protectionist measures adopted by countries. Volumes to key markets such as Southeast Asia and the Middle East impacted overall volumes.

US tariffs, trade protectionism and declining demand in key geographies saw Vietnamese steel exports dropping nearly 20% y-o-y in 9MCY’25. Steel production and domestic sales increased by 9-10% y-o-y in H1CY’25. While domestic demand was strong, export volumes were under pressure, reflecting global steel market volatility and lower demand from key international buyers.

Outlook

Global steel demand is expected to bottom out in 2025 and rise moderately in 2026, as per WSA short-range outlook published in October. Among the key positives, are projections of an over 3% rise in steel demand in the EU and nearly 2% in the US in 2026. While, on the face of it, this appears to be positive for global trade and steel exports, growing protectionism, oversupply and continued rise in Chinese volumes threaten to derail the expected momentum.

In 2025, Chinese exports may rise by 8-10% y-o-y, while the advanced economies witness a decline in global demand export shipments. India’s export prospects, too, remain tied to the possibility of diversification in Asia, Middle East and Africa. But shrinking EU quotas, global trade protectionism and high Chinese exports all paint a dismal picture.

Leave a Reply