- Market sentiment weak amid slow demand and cautious buying

- China’s stainless steel market inactive during holiday period

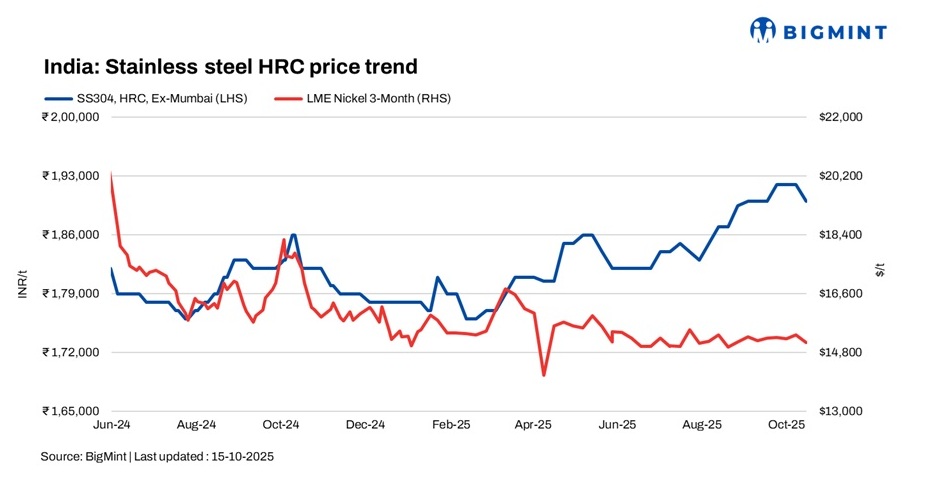

India’s stainless steel (SS) finished market saw mixed trends this week, with finished longs prices rising by up to INR 2,000/t and finished flats prices dropping by up to INR 2,000/t w-o-w amid delayed imports.

BigMint assessed 304-series hot rolled coils (HRCs) at INR 190,000/t ex-Mumbai, down INR 2,000/t w-o-w, while 304L black round bars (25-100 mm) also remained stable at INR 160,000/t, unchanged w-o-w. In contrast, 316-series hot-rolled coils (HRCs) stood steady at INR 345,000/t and cold-rolled coils (CRCs) were at INR 350,000/t w-o-w.

Market sentiments

Market participants reported a noticeable shortage in the domestic market as delayed shipments from China and other countries continue to limit supply, providing mild support to flat product prices. However, overall market conditions remain weak, with demand subdued despite recent relaxation in BIS norms. “A meaningful recovery is unlikely in the next six months”, one source noted.

Finished longs demand continues to rely mainly on immediate, need-based purchases, with little sign of speculative or bulk buying activity.

Global insights

China’s stainless steel market remained largely inactive during the National Day and Mid-Autumn Festival holidays, with limited trading and shipments. While broader market sentiment improved on expectations of U.S. Federal Reserve rate cuts and stronger commodity futures, stainless steel fundamentals stayed weak. Despite the traditional September–October peak season, downstream demand recovery was limited, and transactions remained sluggish.

Market inventories also began to show signs of rebounding after previous declines, adding to supply pressure. Meanwhile, falling prices of key raw materials such as high-grade nickel pig iron (NPI) and high-carbon ferro chrome weakened cost support for stainless steel producers.

Raw materials scenario

Ferro molybdenum: Indian ferro molybdenum prices witnessed an increase of INR 53,000/t ($600/t) as compared to the assessment on 8 October. Prices edged up following the rise in global markets, particularly China, as well as the rise in oxide prices.

Ferro molybdenum prices in India were INR 3,085,000/t ($34,928/t) exw-India, as per BigMints assessment on 15 October.

Ferro chrome: Indian high-carbon ferro chrome (HC-60%) prices dropped by INR 950/t w-o-w to INR 120,400/t ($/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices edged up by INR 1,000/t ($11/t) as compared to the previous assessment on 6 October. Prices increased, as sellers raised their offers following decent export demand, extended rains in Bhutan, and a slight supply crunch, as some sellers were focused on fulfilling SAIL’s tender requirements.

Ferro silicon prices in India were at INR 88,000/t ($991/t) exw-Guwahati, as per BigMint’s assessment on 13 October. In Bhutan, prices rose by INR 600/t ($7/t) w-o-w to INR 88,000/t ($991/t) exw. Deals for around 5,600 t were recorded by BigMint in both regions in this assessment window, within the price range of INR 84,000-89,500/t ($946-1,008/t) exw.

Ferrous scrap: India’s imported scrap market stayed under pressure, with prices falling to nearly a five-year low amid sluggish deep-sea activity and weak buying interest. Most mills remained on the sidelines, reflecting cautious sentiment and limited restocking.

Shredded scrap was offered at $352-355/t CFR Mundra/Nhava Sheva, while busheling stood at $366-370/t and HMS 80:20 around $320-324/t. A firm dollar, high freight rates, and muted domestic steel demand continued to weigh on market confidence.

LME nickel tags remain largely stable w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,110/t, down by $245/t compared to last week’s $15,355/t. Nickel stocks at LME-registered warehouses stood at 243,258 t, up 5% compared to 231,630 t in the previous week.

Outlook

The stainless steel finished market is expected to remain subdued as Diwali approaches. Overall, while current market conditions remain calm, there is an expectation that post-festival demand will drive renewed activity, potentially boosting prices and trading volumes in the coming weeks.

Leave a Reply