- Australian exports fall on reduced port throughput

- South African shipments decline amid thin trading

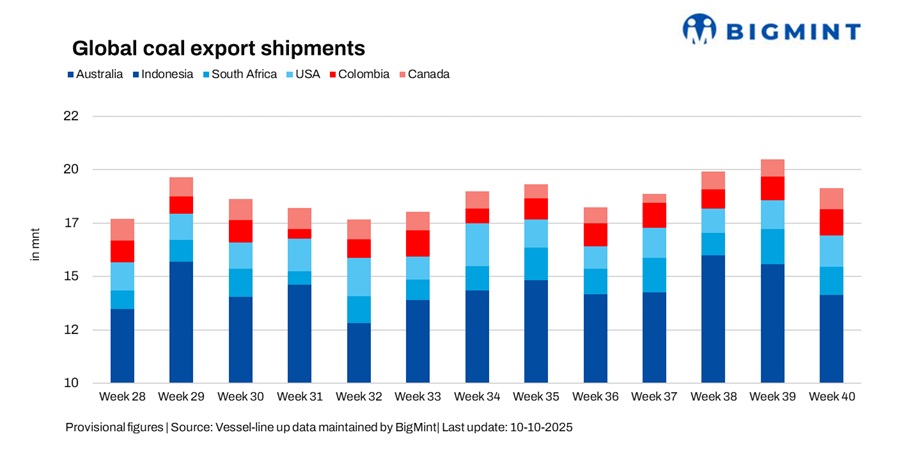

Global seaborne coal exports fell 6.2% w-o-w to 18.78 million tonnes (mnt) in Week 40 (27 September-3 October 2025) from 20.06 mnt in Week 39, according to BigMint’s vessel line-up data. The decline was primarily led by lower shipments from Australia and South Africa, which offset moderate gains from the US, Colombia, and Canada, while Indonesian exports eased slightly.

The fall reflected weaker operational performance in Australia, softer fixture activity from South Africa, and cautious demand on key Asia-Pacific routes. Indonesia’s coal shipments were supported by tighter vessel availability, although limited cargo movements and selective procurement constrained volumes. US and Colombian exports benefited from steady terminal operations and opportunistic demand, while Canadian flows saw a rebound due to stable port throughput.

Country-wise trends

Australia: Australia’s coal exports fell 14.2% w-o-w to 7.19 mnt in Week 40 from 8.37 mnt in Week 39 amid reduced vessel arrivals and weaker port throughput. Shipments from Newcastle (2.20 mnt), Gladstone (1.73 mnt), and DBCT (1.56 mnt) all eased as slower vessel nominations and limited fixture activity curbed loading momentum across major terminals. There was also a decline in coal shipments from Port Hay Point mainly due to minor port and rail maintenance disruptions, along with softer metallurgical coal demand from key Asian buyers.

On the demand front, Japan (2.03 mnt) and China (1.07 mnt) continued to anchor flows, while Indian buying stayed muted amid high landed costs and cautious procurement. Market participants noted that export volumes in the coming weeks will depend on steadier vessel scheduling and port efficiency, with sentiment remaining subdued amid softer trading activity in the Pacific basin.

Indonesia: Indonesia’s coal exports slipped 2.9% w-o-w to 6.78 mnt in Week 40 from 6.97 mnt in Week 39, weighed down by selective buying and limited spot activity. Among key terminals, Bunati (1.19 mnt), Taboneo (1.08 mnt), and Samarinda (0.93 mnt) led shipments, though overall port loadings remained subdued as charterers avoided fresh fixtures amid regional holidays and cautious restocking sentiment.

Despite Indonesia-India freight rates edging higher on tighter vessel availability, weaker industrial demand and soft power generation curtailed cargo flow. China’s intake held steady at around 2.10 mnt, while Indian offtake dipped slightly to 1.14 mnt, reflecting restrained buying interest and near-term uncertainty in the Pacific coal market.

United States: US coal exports increased 8.3% w-o-w to 1.39 mnt in Week 40 from 1.29 mnt in Week 39, aided by steady fixture activity and consistent terminal operations. Key ports such as Norfolk (0.55 mnt), Baltimore (0.48 mnt), Mobile (0.22 mnt), and New Orleans (0.15 mnt) recorded stable throughput, reflecting continued logistical efficiency and firm loadings across the Atlantic coast.

On the demand side, India emerged as the top destination with 0.51 mnt, while other Asian and European buyers maintained limited participation. Market sources indicated that higher freight economics and weaker price arbitrage capped further gains, keeping overall trading sentiment steady but cautious despite the week’s volume uptick.

South Africa: South Africa’s coal shipments dropped 19.9% w-o-w to 1.28 mnt in Week 40 from 1.60 mnt in Week 39, as weaker fixture activity and limited Indian buying dampened export volumes. All shipments were routed through Richards Bay Coal Terminal (RBCT), where lower vessel turnarounds and reduced cargo nominations reflected persistent logistical challenges.

India remained the primary destination, taking in 0.63 mnt, though overall sentiment stayed cautious amid subdued spot demand and volatile freight trends. Market participants noted that recurring rail bottlenecks and charterer hesitation continued to weigh on South Africa’s coal export momentum, offsetting any near-term support from earlier freight firmness.

Colombia: Colombia’s coal exports increased 12.6% w-o-w to 1.18 mnt in Week 40 from 1.05 mnt in Week 39, supported by stable operations and a modest recovery in fixture activity. Leading miners such as Prodeco Group (0.79 mnt) and Cerrejon Mines (0.23 mnt) drove the uptick, while Puerto Nuevo (0.78 mnt) and Puerto Bolivar (0.23 mnt) handled the bulk of shipments, complemented by minor loadings from smaller terminals totaling 0.16 mnt.

On the demand side, South Korea (0.30 mnt) emerged as a key buyer, with opportunistic restocking and steady freight levels helping sustain flows. Market participants indicated that while broader Atlantic demand remains subdued, Colombia’s flexible supply positioning and miner-driven stability are supporting short-term export resilience.

Canada: Coal exports from Canada rose 23.9% w-o-w to 0.96 mnt in Week 40 from 0.78 mnt in Week 39, supported by steady miner output, smoother rail movement, and improved vessel turnaround. Port-wise, Vancouver shipped 0.39 mnt, while Roberts Bank and Prince Rupert handled 0.26 mnt and 0.32 mnt, respectively, reflecting stable port operations and reduced congestion.

South Korea (0.23 mnt), Hong Kong (0.16 mnt), and The Netherlands (0.16 mnt) remained the key buyers, with Asian utilities restocking ahead and European traders capitalizing on softer freight rates. The rebound highlights improved logistics, though sustained momentum will depend on consistent rail performance and favourable weather at west coast terminals.

Freight trends

Dry bulk coal freight rates in Week 40 showed a mixed trend amid subdued trading. Indonesia-India rates inched higher due to tighter vessel availability, while Australia-India and South Africa-India Panamax freights softened amid inactivity and cautious charterer sentiment.

Limited fixtures and selective buying restrained cargo movement on routes with ample tonnage, though tighter lanes occasionally saw support. Freight volatility affected shipment decisions, particularly on Australia and South Africa routes, contributing to weaker flows.

Outlook

Near-term coal exports are expected to remain volatile. Australian and South African shipments may stay under pressure due to limited vessel arrivals and muted charterer activity.

Indonesian flows could benefit from tight vessel availability, while US, Colombian, and Canadian exports may continue to see selective demand support. Overall trade momentum is likely to remain cautious, influenced by freight volatility, seasonal demand fluctuations, and port reliability.

Leave a Reply